Buybacks: Washington’s Warning

Stock buybacks are a conflict of interest which has been exposed primarily through extravagant levels of executive pay and income inequality. As an extension of previous articles on this topic, 720 Global digs even deeper to expose the truth behind the logic and rationale of corporate stock buybacks.

In his 1995 speech at Harvard University, Charlie Munger (Vice Chairman Berkshire Hathaway) walks through a multitude of causes for human misjudgment. Embedded throughout his speech is the core role incentives play in influencing human behavior.One does not require a PhD in psychology to understand why corporate executives continue to expand stock buybacks at, counter-intuitively, record high stock valuations. The latest reminder of such incentives comes from The Center for Effective Government and Institute for Policy Studies. In a recent study they found that the retirement funds of the chief executives of the 100 largest corporations are worth on average just under $50 million, or a combined $4.9 billion.This amount is equal to the aggregate retirement accounts of 41% of U.S. families.

Stunning facts like that compel 720 Global to continue to raise awareness regarding the dangers buybacks impose not only on American public companies and their investors but also on the economic and social fabric of the nation. In part 1 of this series, “Buybacks: Connecting Dots to the F-Word”, 720 Global highlighted how executive leadership has elected to engage in uses of their corporate resources that benefit executive compensation at the expense of long-term shareholders, the company’s future success and ultimately the U.S. economy. Part 2, “Shorting the Buyback Contradiction”, examined the ways in which buybacks distort equity valuations and exposed the unknown risks being shouldered by investors.

This third article in the series extends the analysis of the prior two articles.It provides a more specific review of the ways in which corporations are manipulating their stock price and abusing the trust of investors to the direct benefit of corporate executives.

Corporate America and American Values – The Backdrop

Well before the Revolutionary War, commerce and trade in the American colonies was vibrant.By the early 1700’s, the colonies under British rule had rapidly become one of the most productive and wealthiest economies in the world, providing Great Britain with an invaluable source of trade goods as well as an increasingly powerful tax base for revenue.Naturally, those businesses - farming, manufacturing, printing and journalism, education, import/export – have evolved into what we know today as the domestic corporate sector.As corporate America grows stronger, more profitable and more powerful and influential, logic follows that this is a reflection of the durability and steadfastness of America.That is as it has always been.

These businesses, and their now global success are a manifestation of something immensely larger than that of the profits and material benefits they generate.The foundation of this country was conceived, established, dedicated and founded by good, brave men whom we today endearingly and reverently refer to as our Founding Fathers.By them, the United States of America was founded for a multitude of express purposes which cumulatively represent a set of moral ideals.From these established ideals, more than any other country in the history of mankind, much happiness and success has been derived.The fact that the United States of America was established as a republic, a nation based on the rule of law, amplifies the obligation of the population, especially leaders of all forms, in adhering to those moral ideals.

Reinforcing this concept in his first inaugural address to the population of the new republic, George Washington warned “…the propitious smiles of heaven can never be expected on a nation that disregards the eternal rules of order and right which heaven itself has ordained.”And yet, for all of that foundation and obligation and reverence to which we owe our remarkable success, the traditional mechanisms by which we measure that success are failing.

Executive Greed

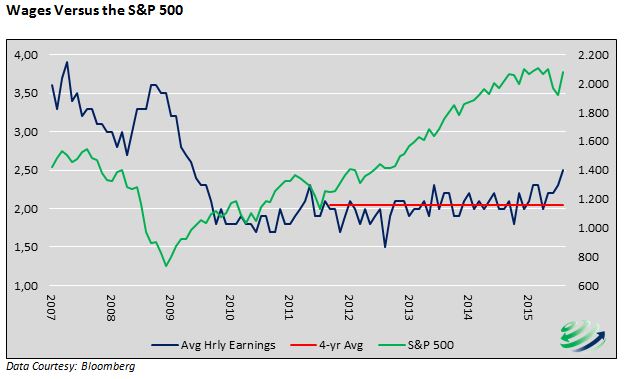

Today, corporate profits and U.S. stock markets, two of our broadest yardsticks for measuring economic success, are near record highs.On those metrics, one might be tempted to suppose that the strength of America is reflected in the strength and success of its businesses.And yet, corporate profitability and rising stock markets are not translating into widespread economic prosperity as shown in the graph below comparing stagnating hourly earnings versus the S&P 500.

Vast swaths of the population in the United States are not enjoying the benefits of the so-called post-crisis recovery.Meanwhile, the top executives of major corporations are prospering in a way never before seen.This contrast between the rich becoming ultra-rich and the rest of the population stagnating at best, was a characteristic of the pre-depression “Roaring 20’s” as well.

A report issued by the Economic Policy Institute on CEO pay highlights that in 2014 the CEO-to-worker compensation ratio was 303X compared with 58x in 1989 and 20X in 1965.The exponential rise in executive compensation has occurred in both relative and absolute terms.From 1978 to 2014, inflation-adjusted CEO compensation increased 997 percent, almost double the rise in stock market value. When compared with other highly paid workers (defined as those earning more than 99.9% of other wage earners), CEO compensation was 5.84 times greater.The rate at which CEO compensation outpaced the top 0.1% of wage earners reflects the power of CEO’s to extract “concessions” rather than an outsized contribution to productivity.

The composition of executive pay has gone from one predominately salary based with less than 15% stock and option rewards in the mid-1960’s to one heavily dependent on stock and option rewards averaging well over 80% in 2013.These stock-based incentives make executives highly motivated to keep their stock price elevated at all costs.The compensation structure in conjunction with the rise in pressure from Wall Street and investors to keep stock prices elevated arguably leads to short-term decision-making that ultimately does not afford proper consideration of the long-term problems those decisions create.

One of the most prevalent ways in which executives can carry out such a compensation-maximizing scheme is through share buybacks.Share buybacks as a percentage of corporate use of cash are at near-record levels and rising rapidly. In a market where all major indices and the majority of publicly-traded company shares are near all-time highs, the proper question is, why?As Warren Buffett wrote in his 1999 letter to shareholders, “Managements, however, seem to follow this perverse activity (buy high, sell low) very cheerfully.”As outlined in Part 1 on this topic, Connecting Dots to the F-Word, the three reasons CEO’s give to justify this action do not stand on their own. The purpose of this article is to explore more deeply, as a point of emphasis, the backdrop which allows such activity to proliferate and to further expose the “chicanery” (Buffett’s word) being employed by corporate executives in continuing to engage in share buybacks in defiance of sound business practices.

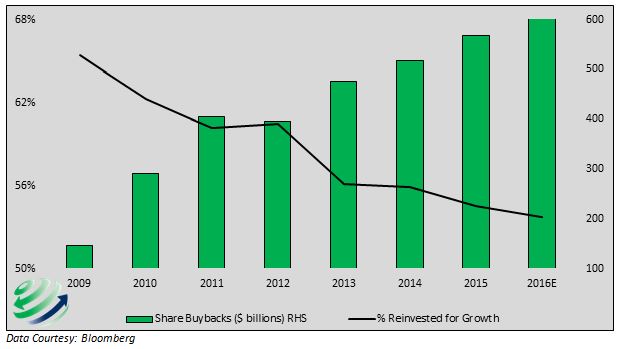

In 2007, companies in the S&P 500 returned over one-third of their cash, $635 billion, to shareholders through buybacks as shown below.At the time, this played a meaningful role in helping to elevate equity market valuations into the teeth of the subsequent financial crisis when stocks fell by over 50%.Now in 2015, share buybacks are expected to rise 18% on a year-over-year basis.Like 2007, corporations will again spend nearly one-third of cash, over $600 billion, on buybacks. The growing popularity of buybacks is graphed below along with the disturbing trend in the percentage of cash invested for future growth. Similarly, stock valuations measured several different ways rival levels only seen with the exuberance of 1929, 2000, and 2007.

Share Buybacks versus the Percentage of Cash Reinvested for Growth

Naturally, the data appears disturbing but a recent report from Reuters puts an even finer point on the issue.In an investigative article entitled The Cannibalized Company, Reuters states:

“Almost 60 percent of the 3,297 publicly traded non-financial U.S. companies Reuters examined have bought back their shares since 2010.In fiscal 2014, spending on buybacks and dividends surpassed the companies’ combined net income for the first time outside of a recessionary period, and continued to climb for the 613 companies that have already reported for fiscal 2015.In the most recent reporting year, share purchases reached a record $520 billion.Throw in the most recent year’s $365 billion in dividends, and the total amount returned to shareholders reaches $885 billion, more than the companies’ combined net income of $847 billion.”

The premise behind the current executive pay structure argues that the talent associated with the strategic decision-making and leadership qualities required to successfully drive large organizations is unique, hard to find and, once found, critical to be retained.In efforts to better align the incentives of corporate executives and the interests of the company, executive compensation has increasingly become tied to outcomes associated with stock price.Award executives more stock, and, assuming they make good decisions for the growth of the company, the share price will rise and reward the executive and shareholders alike.

Alternatively, what is happening is the compensation structure for CEO’s and senior executives has become so skewed towards stock-based incentives of such gargantuan size that it has become the predominant driver of corporate decision-making.Companies eschew the idea of making longer-term investments through capital expenditures because it does not immediately help the measurement ratios upon which Wall Street bases “success”, and it may indeed hurt those ratios.Of course, these are the same ratios upon which executive compensation depends, since Wall Street analyst recommendations drive share prices and share price drives executive compensation.The result in one case is strategic decision-making that naturally neglects long-term commitments of capital into what Clayton Christensen calls “market-creating Innovations” in favor of “efficiency innovations”.As described in Innovation, companies become increasingly dependent upon efficiency innovations and the balance between important long-term and short-term uses of capital is quickly lost causing economic harm.

In another case, executives use precious capital, often borrowed, to conduct share repurchases precisely because it has the immediate effect of driving share prices higher.As 2007 illustrated, this façade of “value” is short-lived because it does nothing to organically enhance the value of the company and hurts long-term prospects by diverting cash to a very expensive use. In this case, the perceived “talent” of leadership required in senior executives to successfully drive large organizations is fallacious and runs counter to the logic applied in their exorbitant pay structures.It also disregards “the eternal rules of order” George Washington spoke of in his first inaugural address.

The end result of either case is that corporate cash, earned or borrowed, is squandered for the self-serving purpose of maximizing executive compensation instead of being used for productive purposes.

“Maximizing Shareholder Value”

Several events have come together over the years to enable and encourage such behavior by executive leadership.In the mid-1970’s, the concept of maximizing shareholder value was introduced by Jensen and Meckling, professors at the University of Rochester.Thus began the era of myopia related to stock-based incentives for executives with no foresight as to the long-term implications of such an ill-conceived concept.We see this effect repeatedly in policy construction within our government.Politicians identify a problem and then set about crafting a bill that will address it without realistic consideration for either the immediate peripheral implications or the long-term unintended consequences.What begins as a well-meaning, if not vote-attracting, proposal soon becomes a law that in 5 or 10 years mushrooms into a vast government program and deep financial burden offering little economic benefit.

In 1982, the Securities Exchange Commission created a rule that allowed companies to buy back their own shares.Rule 10b-18 allows a company’s board of directors to authorize senior executives to repurchase up to a certain dollar amount of stock over a specified or open-ended period of time.The company must publicly announce the program after which it may then proceed to repurchase their own shares on the open market without concern that the SEC will charge it with stock price manipulation.There are a few guidelines within which the company must operate regarding repurchases but the oversight is structurally weak and only monitored quarterly.Rule 10b-18 explicitly legalized stock market manipulation through open-market repurchases.

The rule was radically divergent from the agency’s original mandate laid out in the Securities Exchange Act of 1934 which properly responded to the multitude of corrupt activities that fueled speculation and led to the 1929 stock market crash.The adoption of Rule 10b-18 reflected the view of then commission chairman John Shad, former vice-chairman of E.F. Hutton and obvious Wall Street insider, that the risks of sweeping deregulation of securities markets were justifiable.With the stated mission of the SEC in mind, “to protect investors, maintain fair, orderly, and efficient markets, and facilitate capital formation”, liberties currently afforded corporate executives through share buybacks are at odds with that mission.

Taxpayers Subsidize Corporate Spending - Buybacks Subsidize Executives

The power and influence of corporate America is further on display in their lobbying efforts to extract public-sector funding for assistance in trade and research and development.Despite trillions in accumulating public debt and on-going deficits, publicly-held companies with record profits, lobby for and receive assistance in funding pet projects to their benefit.At the same time, instead of using their own cash to advance these projects, they engage in share buybacks which divert capital toward a highly self-serving purpose.Although the public assistance of funding such projects occurs under the guise that the U.S. corporations cannot remain competitive without the aid of federal funds, it is unclear why taxpayer funds should be used to subsidize the investment activities of corporate entities which at the same time are using their own capital to repurchase stock.

According to William Lazonick a professor at the University of Massachusetts at Lowell who cites the Center for American Progress, Exxon Mobil received $600 million per year in subsidies for oil exploration.The energy giant spent approximately $21 billion a year on share buybacks while spending approximately zero dollars on alternative energy efforts.Microsoft, GE and other companies lobbied the U.S. government to triple their investment in alternative energy research and subsidies to $16 billion per year.Over the past ten years, Microsoft and GE spent about the same amount annually on share repurchases.

The same thing happens in nanotechnology, pharmaceuticals and virtually every other business sector.Powerful companies lobby congress for federal spending on what are certainly important issues that deserve research and development focus.However, the companies themselves turn around and spend multiples of billions manipulating their stock price which boosts already egregious executive compensation.Lazonick points out that Intel spent four times the budget of the National Nanotechnology Initiative (NNI), which receives federal funding, then on buybacks in 2013.According to the Wall Street Journal, Intel CEO Brian Krzanich received $10 million in compensation in 2013, less than 10% of which was base salary (Krzanich received a 20% pay increase in 2014).

Major pharmaceutical companies such as Merck, Allergan, AbbVie and Pfizer generally argue that the profits from high priced healthcare drugs permit more research and development to be done in the United States.Importantly, Lazonick points out that these firms coincidently enjoy tremendous benefits of favorable intellectual property rules and weak price regulation by doing their business in the US.Yet in the 10 years between 2004 and 2013, Pfizer alone used over 70% of its profits for share buybacks.The painfully high prices Americans pay for prescription drugs has far more to do with stock price manipulation and inflated executive compensation than the stated cost of conducting R&D in the United States.That explanation is a smokescreen intended to deceive legislators, regulators and the public.Pfizer CEO, Ian Read, was paid $23.2 million in 2014, nearly 70% of which was stock and option-based rewards.

Conclusion

The prophetic warnings of corruption of America’s moral ideals may have begun in 1789 with the words from America’s first President, but they have been routinely revisited throughout our history.In 1961, Dwight Eisenhower also issued a dire warning in his farewell address to the nation.In that address he pointed specifically to the military-industrial complex, a term he coined, but words which today have far broader application.

“…we must guard against the acquisition of unwarranted influence… The potential for the disastrous rise of misplaced power exists and will persist.Only an alert and knowledgeable citizenry can compel the proper meshing of the huge industrial and military machinery of defense with our peaceful methods and goals, so that security and liberty may prosper together.”

It is vital to give proper consideration to the improper liberties that are being taken by those with “unwarranted influence” and “misplaced power”.Value extraction has replaced value creation in pursuit of short-term, self-serving benefits at the expense of long-term stability and durability of corporate America and therefore the country as a whole.As citizens, our obligation is to be well-informed, cognizant, outspoken and to vote.As investment managers, our role is to always protect the wealth of clients through a critical view of the actions of authorities with fair and rigorous questioning of intentions and incentives.The words of men may temporarily suspend but they do not alter the laws of financial dynamics. The fundamentals always take precedence eventually.

This likely will not be the last piece 720 Global writes on stock buybacks. We will continue to focus on this topic in an effort to inform equity and bond investors of the harmful activities they are knowingly or unknowingly supporting.

Disclosure: Opinions expressed herein are current opinions as of the date appearing ...

more