AUD/USD Rate Vulnerable To Slowing China Consumer Price Index (CPI)

AUD/USD pares the decline from earlier this week as the U.S. Non-Farm Payrolls (NFP) report disappoints, and the exchange rate may continue to consolidate over the coming days as it fails to extend the recent series of lower highs & lows.

AUD/USD RATE VULNERABLE TO SLOWING CHINA CONSUMER PRICE INDEX (CPI)

AUD/USD holds above the weekly-low (0.7191) as the NFP report shows a 155K expansion in November versus projections for a 198K print, with Average Hourly Earnings holding steady at 3.1% per annum for the second consecutive month.

The lackluster data prints may push the Federal Open Market Committee (FOMC) to deliver a dovish rate-hike later this month especially as Fed Vice-Chairman Richard Clarida warns that ‘we are in a world where central banks, including the Fed, are focused on keeping inflation away from disinflation,’ and Chairman Jerome Powell & Co. may continue to soften their hawkish tone over the coming months as the central bank shows a greater willingness to tolerate above-target inflation over the policy horizon.

In turn, waning expectations for an extended hiking-cycle may produce headwinds for the greenback, but the diverging paths for monetary policy continues to cast a long-term bearish outlook for AUD/USD especially as the Reserve Bank of Australia (RBA) keeps the door open to further support the economy.

(Click on image to enlarge)

As a result, data prints coming out of China, Australia’s largest trading partner, may shake up AUD/USD as the region faces its slowest economic expansion since 2009, with the Consumer Price Index (CPI) expected to narrow to 2.4% from 2.5% in October. Moreover, the lingering threat of a U.S.-China trade war is likely to keep the RBA on the sidelines as it dampens the economic outlook for the Asia/Pacific region, and the central bank may continue to tame bets for higher borrowing-costs as ‘the low level of interest rates is continuing to support the Australian economy.’

Keep in mind, Governor Philip Lowe & Co. also appear to be bracing for a further depreciation in the local currency as official note ‘a broad-based appreciation of the US dollar this year,’ and the RBA’s wait-and-see approach may continue to produce headwinds for the Australian dollar as the floating exchange rate ‘remains an important shock absorber for the Australian economy.’

With said, AUD/USD remains at risk of giving back the advance from the 2018-low (0.7021) as the RBA remains in no rush to lift the official cash rate (OCR) off of the record-low, but retail traders continue to fade the weakness in the exchange rate as the pickup in volatility fuels a rebound in market participation.

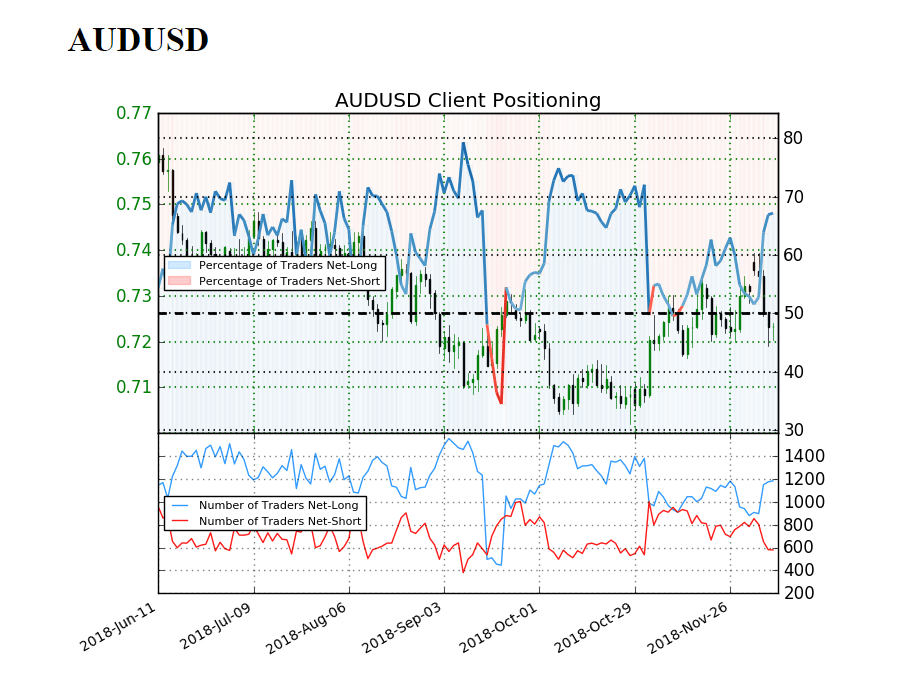

The IG Client Sentiment Report shows 67.2% of traders are still long AUD/USD compared to 69.1% yesterday, with the ratio of traders long to short at 2.04 to 1.The number of traders net-long is 3.0% higher than yesterday and 18.3% higher from last week, while the number of traders net-short is 3.8% higher than yesterday and 30.5% lower from last week.

Profit-taking behavior may account for the drop in net-short position amid the pullback from the monthly-high (0.7393), but the skew in retail position offers a contrarian view to crowd sentiment as both price and the Relative Strength Index (RSI) now snap the bullish formations carried over from October.

AUD/USD DAILY CHART

(Click on image to enlarge)

-

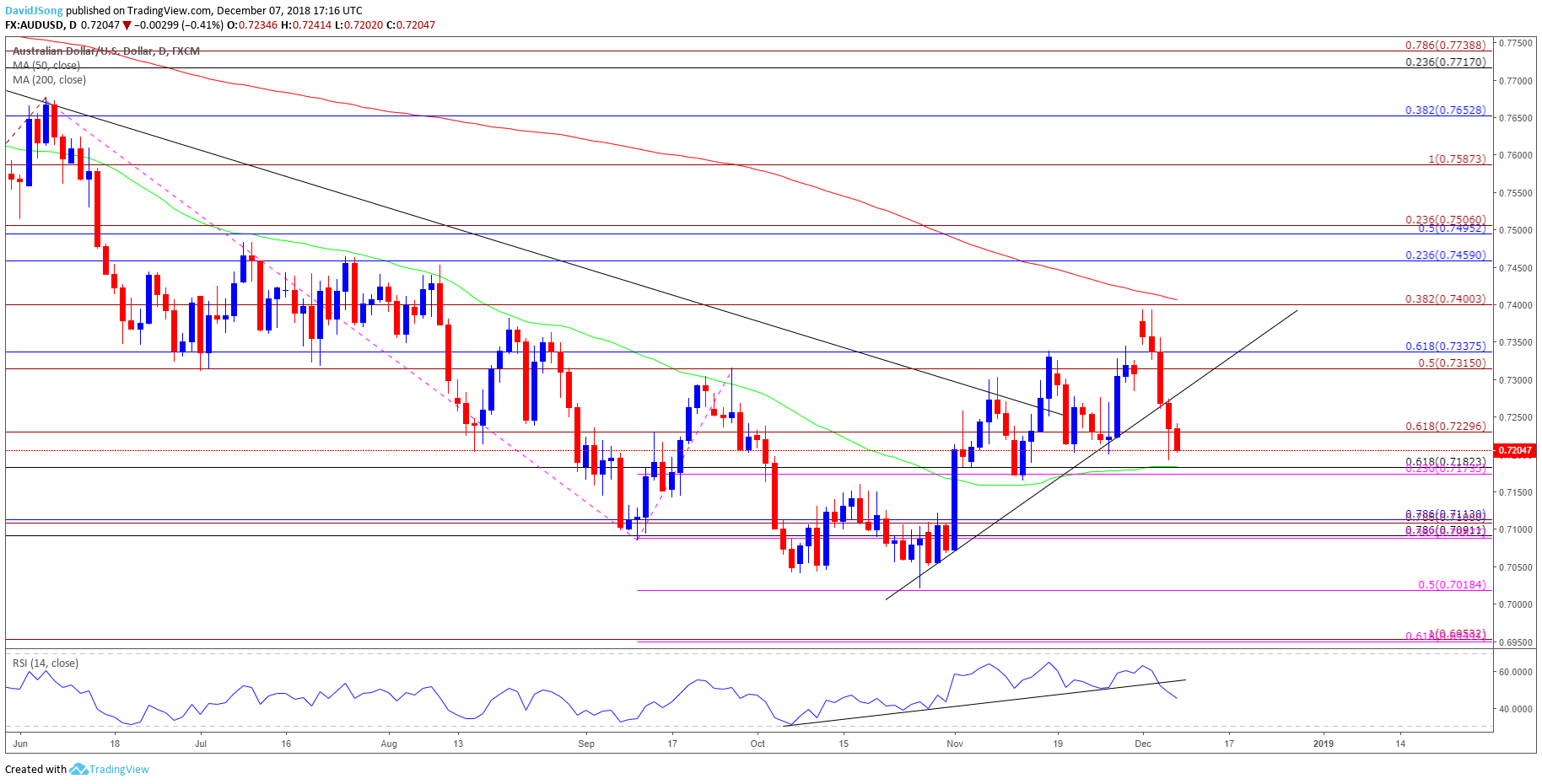

The opening range for December raises the risk for a further decline in AUD/USD as price and the Relative Strength Index (RSI) snap the bullish formations from October, with the 0.7170 (23.6% expansion) to 0.7180 (61.8% retracement) region on the radar.

-

A break/close below the stated region raises the risk for a move towards0.7090 (78.6% retracement) to 0.7110 (78.6% retracement), with the next downside hurdle coming in around 0.7020 (50% expansion), which lines up with the 2018-low (0.7021).

Disclosure: Do you want to see how retail traders are currently trading the US Dollar? Check out our IG Client Sentiment ...

more