5 Stocks Poised To Beat On Earnings - ZEN, FOSL, NVDA, SAM, VA

Photo Credit: Arturo Donate

It’s been difficult to find bright spots this earnings season, and with less than 25% of the S&P 500 left to report, it looks like the fourth quarter will close as one of the worst since the recession. Not since the third quarter of 2009 has both top and bottom-line growth for the index come in negative, with current figures standing at -3.5% and -2.9%, respectively.

With that said, there are a handful of names reporting this week that carry a very bullish signal. The following 5 companies have a significant positive delta between the crowdsourced Estimize consensus and the Wall Street consensus, and also have a strong track record of beating analyst estimates. Even so, this quarter has forced us to question a value of a beat in this environment, with forward looking guidance capturing most of the attention of nervous investors.

To have your expectations included in the Estimize consensus for this week’s reports,get your estimates in here!

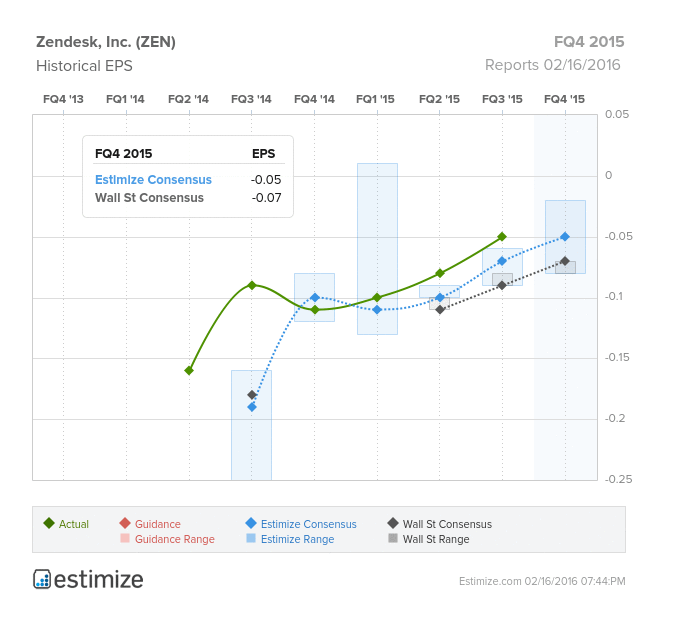

Zendesk (ZEN) was one of our picks for stocks to watch in 2016. Despite the recent unwarranted collapse of enterprise tech names, the US economy by many measures still seems to be in good standing, and that means companies will be investing in the cloud and into their own growth. For the current quarter, the Estimize community is looking for EPS of -$0.05, only two cents higher than Wall Street, but sell-side estimates have been lifting into the report.

Zendesk competes in the customer data management space and is taking on the big guys like Salesforce. Since IPOing in May 2014, the company has had a laser focus on growing revenues, resulting in top-line growth of 63%+ over the last 4 quarters. While still unprofitable, EPS has been trending in the right direction, and the company has beaten Wall Street estimates every quarter.

As of October, ZEN had more than 64,000 customers, up from 50k earlier in the year, and the percentage of clients with 100 or more seats accounted for 30% of recurring revenue. Recent acquisitions such as We Are Cloud certainly strengthen its portfolio and makes it a formidable contender against similar cloud analytics products from Salesforce and Amazon.

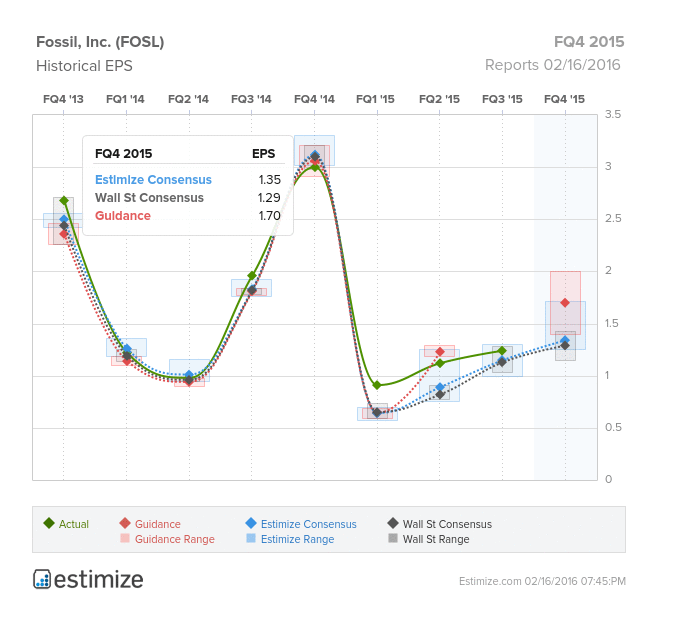

Fashion accessory company, Fossil (FOSL), is also scheduled to report after today’s closing bell. Currently, the Estimize community is looking for EPS of $1.36, a sizeable 7 cents ahead of Street. This is a company that tends to beat the Estimize EPS consensus 63% of the time historically, and the Wall Street consensus an even greater 90% of the time. Despite the wide delta, this still suggests a 54% decline in YoY profits. Fossil is coming off a year which saw share prices fall 67% due to a decline in its portfolio of licensed brands, weaker watch sales, and sluggish international performance from currency headwinds.

Growth of Fossil’s flagship product, watches, turned negative in 2015 for the first time in 5 years, due to a weakened portfolio of licensed brands and market saturation. Slower demand for Michael Kors products has played a large role in Fossil’s sales decline. The Kors brand represents roughly 25% of Fossil’s revenue and has contributed to almost 50% of the company’s sales growth in the past 5 years.

However, the company’s biggest threat comes from the increased popularity of tech accessories including smartwatches and activity trackers. As a result, the company is adjusting its strategy by leaning on investments in smart accessories to revive growth and capture a share of the robust wearables market. Last quarter, Fossil rolled out a line of Fossil branded watches in partnership with Google and Intel, they also recently acquired Misfit, a producer and manufacturer of wearables.

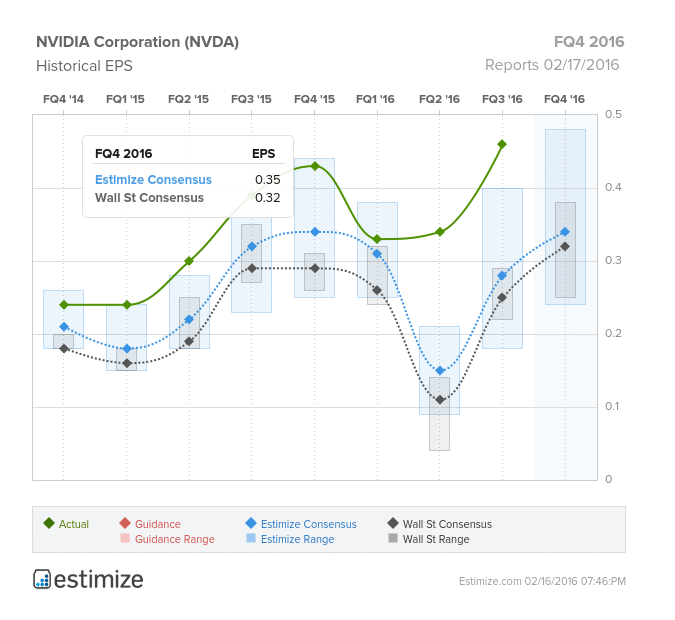

The last couple of years haven’t been kind to semiconductors and chipmakers, but after tomorrow’s closing bell we might just get some welcomed news from Nvidia (NVDA). The Estimize community is calling for EPS of $0.34 on this name, as compared to the Street’s estimate of $0.32. Current estimates reflect an uptick of 35% from Estimize and 18% from the sell-side over the last 3 months. Nvidia historically has surpassed the Estimize consensus 69% of the time, and that number bumps up to 75% for Wall Street.

“How can a semiconductor company be doing well in this environment?,” you may ask, considering the freefall of the PC market and the negative impact of the stronger dollar. Nvidia has kept it’s head above water due to its focus on gaming which accounts for more than 58% of total revenues. The strong momentum in the company’s graphic card sales drove the stock 64% higher in 2015. The gaming business is expected to be a growth driver once again in 2016 as NVDA diversifies from traditional PC gaming into virtual reality. However, the company’s fastest growing segment is autonomous driving, with revenues estimated to have grown 85% in FY 2015.

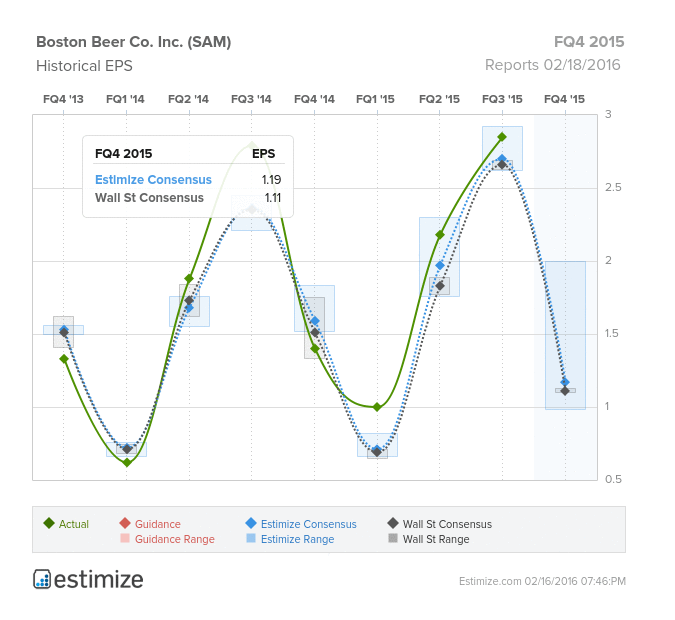

Craft beer is having a moment, and it’s certainly been beneficial for the Boston Beer Company (SAM). The Estimize EPS consensus for Q4 currently stands at $1.21, a dime higher than Wall Street expectations. While this name only beats the Estimize consensus 50% of the time, their history of beating the Street is considerably higher at 63%. Despite coming off of another strong beat last quarter, heavy revisions have brought earnings estimates down 16%.

SAM faces a number of headwinds this quarter. Consistent efforts to build its portfolio of drinks have been key to revenue growth, but a slowdown in depletion trends towards the end of the year points to stiff competition in the craft beer market as well as weakness in the cider category. Hard cider which makes up 20% of total revenues, was hit hard by the popularity of hard root beer in 2015. The first mover in this category was Small Town Brewery’s Not Your Father’s Root Beer which managed to capture 80% of the market, while SAM’s competing product, Coney Island Hard Root Beer only held onto 18%.

International expansion could be the key to future growth for the Boston Beer Company, however, as they focus on acquiring assets to expand geographically and grab market share overseas. The Indian market in particular is considered a goldmine for company.

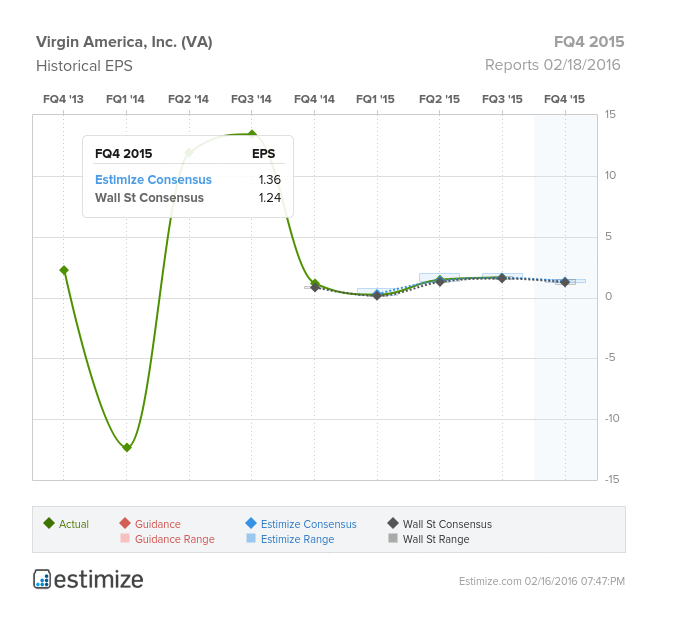

Last on our list is Virgin America (VA), which sits in a segment that has done very well so far in the fourth quarter. Analysts from Estimize predict the domestic airliner will report profits of $1.31 on Thursday, higher than the Street’s $1.24. Revenues of $395.5M are also slightly higher. While the company has historically beaten the Estimize consensus 50% and 67%, respectively, on these two metrics, that number increases to 100% when using the Wall Street consensus. With only 4 quarters as a public company, the Estimize community has been more accurate on this name in each of those periods.

One big trend culled this earnings season was the disparity in results for discount airlines vs. larger carriers. Discount domestic airlines that fly to very few, if any, international destinations, do not have to contend with the stronger dollar impact. Currency headwinds have been such a drag on multinational airlines, that several large carriers have decreased international routes. Virgin America is expected to go the way of it’s contemporaries, JetBlue, Spirit and Allegiant, all which had fantastic quarters when compared to international airliners such as Delta, United Continental and American Airlines.

Disclosure: There can be no assurance that the information we considered is accurate or complete, nor can there be any assurance that our assumptions are correct.