The Deflationary Impact Of The Decline In Oil Prices In Canada

History may not repeat itself exactly, but it can be an excellent guide to what lies in store, especially in the oil industry. Dramatic changes in the price of oil have long been a harbinger of the big changes in prices and incomes for a major producing country such as Canada. Let’s start by looking at the experience of the 2014 -2016 to gauge how Canadians will adjust to the seismic shift in the world oil industry we witnessing today.

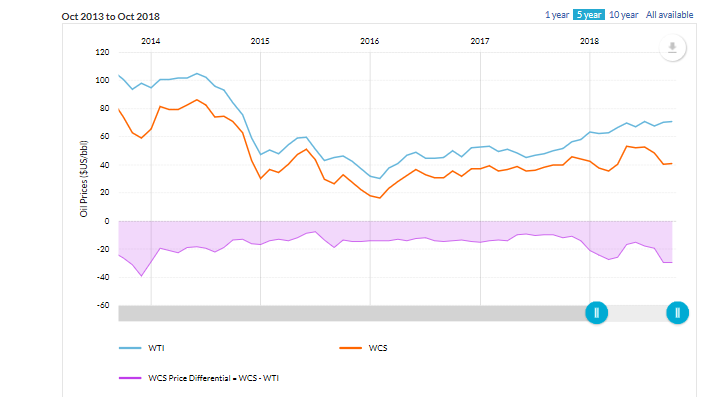

Historically, Western Canadian Select (WCS) normally trades at a discount of US$ 15 bb/ to the West Texas Intermediate (WTI). The discount reflects the higher cost of refining Canadian heavy oil (Figure 1). The collapse in world oil prices starting in 2014 hit the Canadian producers rather hard. By 2016, WCS fetched roughly $15/bbl in March of that year compared to $30/bbl for WTI.

(Click on image to enlarge)

Figure 1 Canadian and US Oil Prices 2014-2018

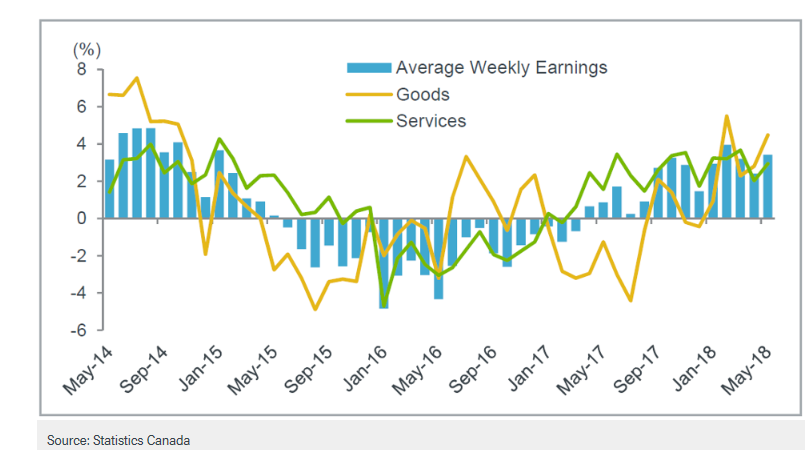

The impact on the Albertan economy was swift and dramatic. Prior to the oil price drop in 2014 average weekly wages in the goods-producing sector were registering gains of 4-6 percent, only to contract by 4-6 percent by 2016. (Figure 2). It took another four years for wages to match the annual growth prior to 2014. It was a painful period in a province that was used to strong growth from natural resource development.

Figure 2 Impact of Oil Collapse on Alberta Economy

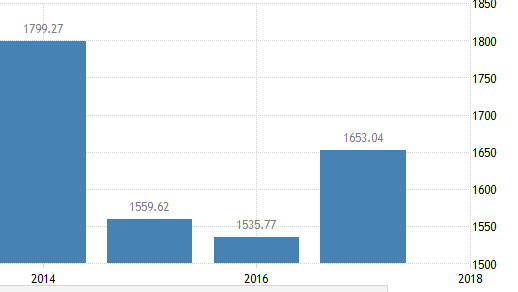

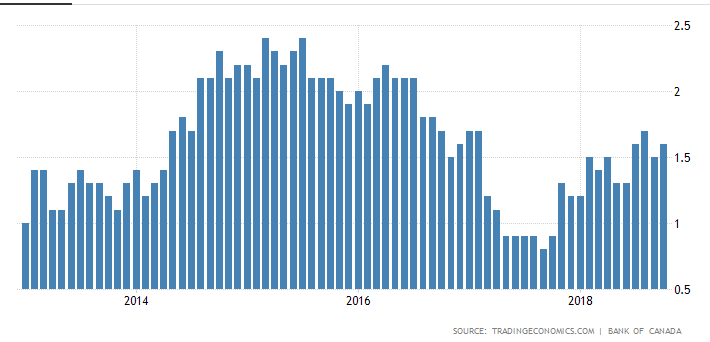

The dramatic fall in oil prices eventually affected other regions of the country as national output declined in 2015 and it was not until 2017 that economic growth emerged (Figure 3). Initially, consumer prices continued to increase at around 2 percent. However, the weakness in the economy eventually resulted in the CPI advancing at less than 1 percent by 2017 and averaging about 1.5 percent since (Figure 4).

Figure 3 Canadian GDP (US$)

Figure 4 Changes in the Canadian CPI

The Bank of Canada cut the bank rate twice from 1 percent to ½ percent in response to the deteriorating conditions. It is only in this past year that the Bank has, in a sense, lifted these emergency rate cuts, an indication of the lasting effects of the 2014 oil price collapse.

Turning to the situation today, Canadian oil producers are facing more serious challenges than those that existed in 2014. As Figure 1 reveals, the spread between WCS and WTI is the steepest it has ever been. WCS now trades at a $35-40 discount to WTI. Several factors can account for this widening of the discount.[1] In Canada, pipeline and rail bottlenecks have reduced the flow of oil to the United States, putting Canadian producers at a disadvantage. Across the border, U.S. oil production has reached record levels at a time when domestic demand is softening. Canadian producers are simply caught between a rock and a hard place. There is no foreseeable recovery expected in the Canadian oil patch.

The question is: what will the Bank of Canada do? So far, the Bank has not given any signal that is about to change its path of rate increases. The most recent bank statement in October left the door open for further rate hikes. The Bank intends to move the rate closer to the ‘neutral’ rate of 3 percent. With the bank rate at 1 ¾ percent, the Bank should be prepared to pause until there is greater clarity on the future price of oil and hence the future growth in Canada. If 2014 presented an emergency, then today’s oil market presents a greater challenge as Canadian oil falls further relative to the world price.