What’s Next For LinkedIn?

Photo Credit: Esther Vargas

LinkedIn Corporation (LNKD) Information Technology - Internet, Software & Services | Reports August 4, After Market Closes

Key Takeaways

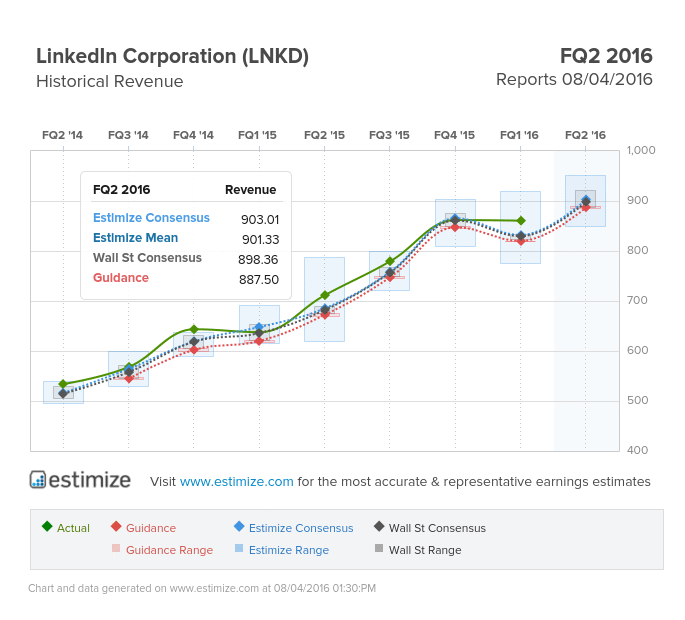

- The Estimize consensus is looking for earnings per share of 82 cents on $903.01 million in revenue, slightly higher than the Wall Street consensus

- Investor’s, as always, will be paying closer attention to user growth, revenue growth, and margins

- The conference call will likely highlight what the future holds after the takeover by Microsoft

- What are you expecting for LNKD? Get your estimate in here!

LinkedIn is scheduled to report second quarter earnings today after the market closes. Unless you live under a rock you know that Microsoft agreed to acquire the professional network for $26 billion. The deal will likely be highlighted in the company’s conference call. This doesn’t mean earnings don’t need to hit expected numbers, because LinkedIn will continue be run as an independent company moving forward. Investor’s as always will be looking for LinkedIn to maintain user growth, margins and revenue growth.

The Estimize community is looking for earnings per share of 82 cents, up 47% from the same period last year. That estimate has increased 9% since LinkedIn’s last report in May. Revenue is anticipated to come in 27% higher on a YoY basis at $903.01 million, marking a 9th consecutive quarter of double digit sales growth. Shares are down 5.34% from a year earlier but it could be more if not for the 50% premium Microsoft paid.

LinkedIn remains a leader in professional networking as it increases its presence and popularity worldwide. The company has recovered nicely from an abysmal fourth quarter that resulted in share prices being cut in half. Last quarter’s results were encouraging and this quarter appears to pick up where things left off. The recent surge can be attributed to the growing popularity of its mobile platform and synergies from acquisitions.

Mobile is clearly the bread and butter for any social media business. Facebook and its shareholders haven’t looked back since the company solved mobile. LinkedIn investors hope to follow in those footsteps. Mobile not only attracts a wider audience but it adds a potential layer of ad revenue. Its past acquisitions of Lynda.com, Newsle and Bizo, help diversify revenue sources outside of its core networking business.

As is the case with all social media companies, eyes will be glued on user growth, which ticked up and impressive 19% last quarter. If this doesn’t meet expectations then expect the stock to tumble.

Disclosure: None.

I've often wondered how many profiles on these social sites are fake. Being that you can buy hundreds of thousands of fake likes on sites like #Linkedin and #Facebook, it must be substantial. I still don't see the value of Linkedin to be nearly $26 billion. $LNKD $FB