Vixen In The Hen House

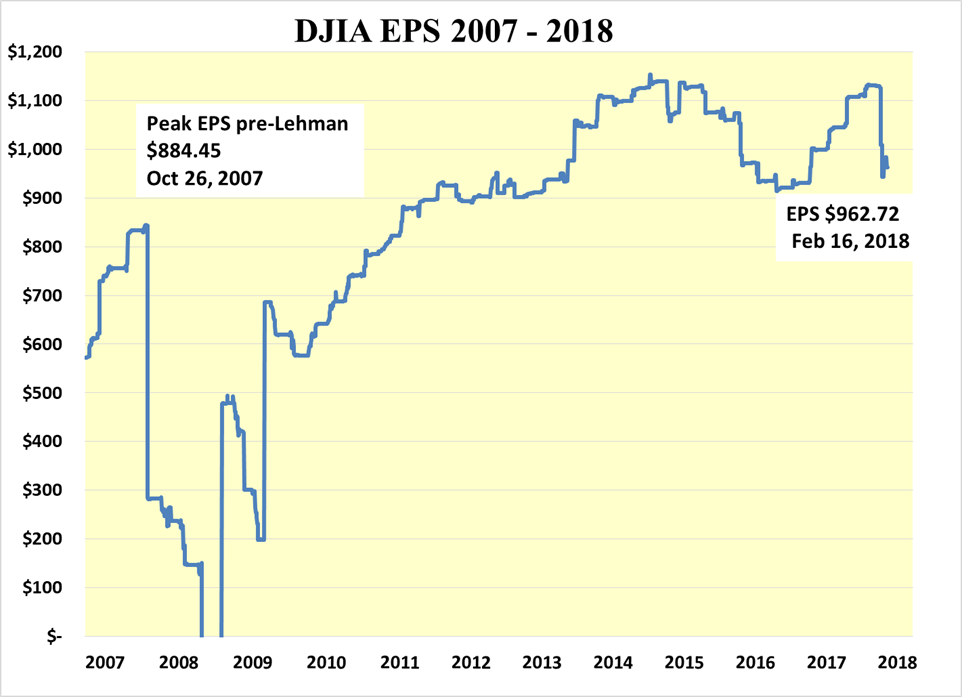

U.S. tax changes are hitting headline Q4 2017 EPS and 52-week trailing DJIA earnings. Quarterly EPS declines should recover as Q1 2018 results are reported in early April showing the true impact of new tax changes.

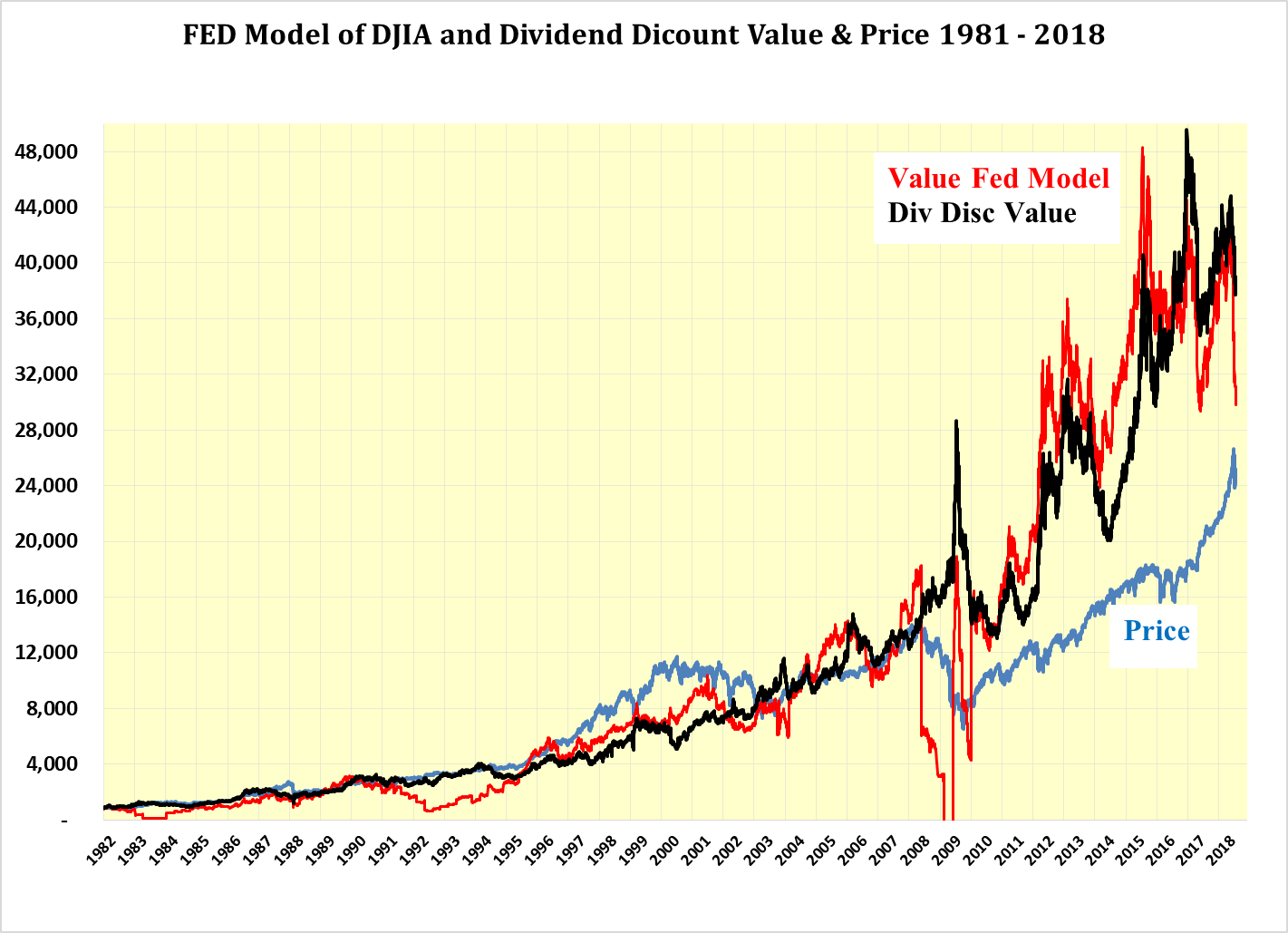

The combination of these changes has driven down the Fed value by 11,346 to 29,898. However, dividend-discount value stands at 37,845 down only 6,100 from 43,945 as the DJIA dividend rose to a record level.

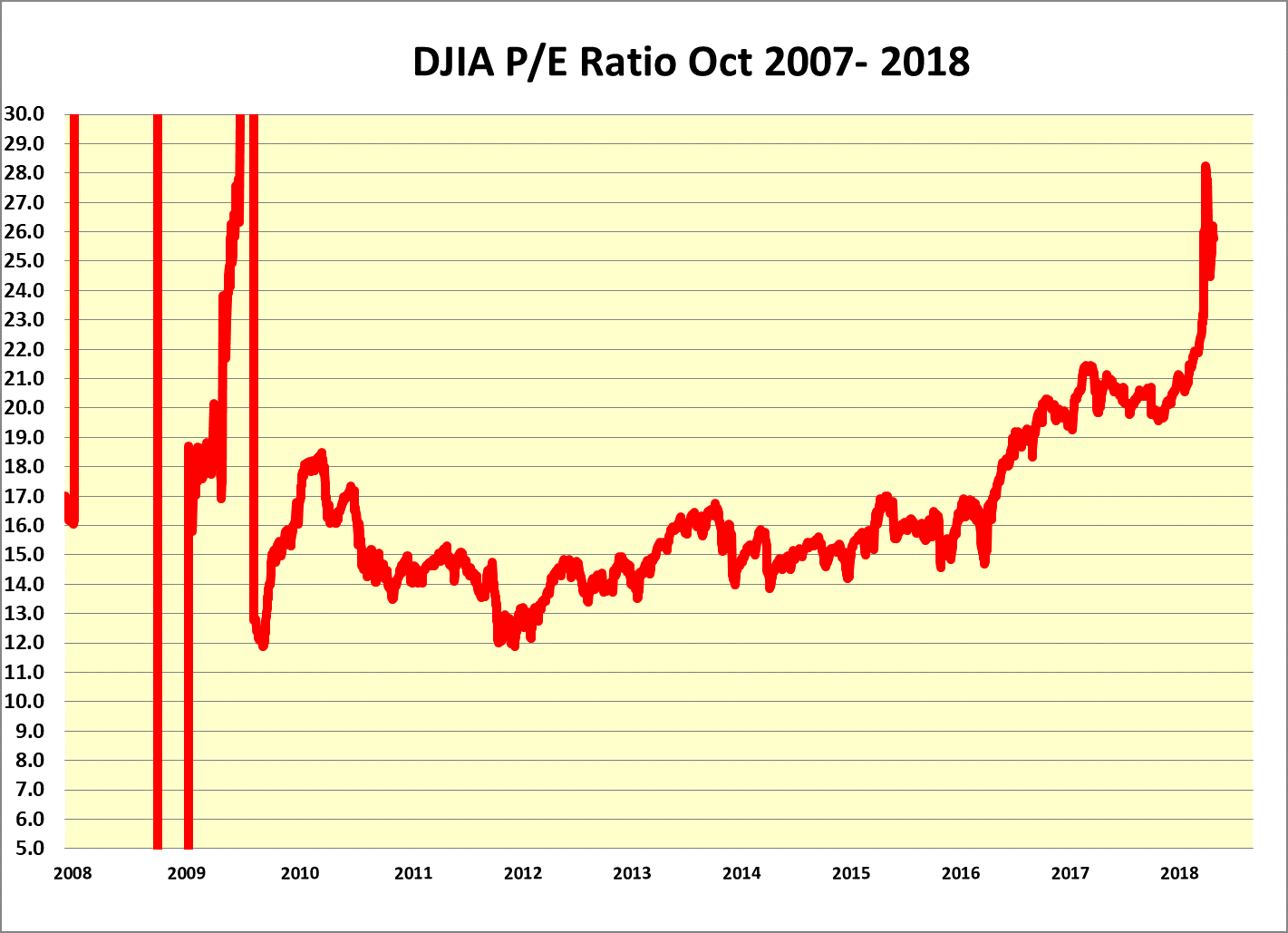

It seems that February’s DJIA unwarranted sell-off was driven by preset algorithms that did not like falling earnings and rising multiples.

Focus, rather, on rising record dividends. The dividend discount value of the DJIA at 37,845 continues to put upward pressure on the price of the DJIA and warrants a continuing “BUY” recommendation.

New Tax Act Good for Headline EPS in 2018 but Very Negative In Q4, 2017

The new U.S. Tax Act should lower corporate taxes and increase earnings in 2018 and beyond. However, there are a number of one-time, write-offs that have been, and are, negatively impacting headline earnings from the fourth quarter of 2017. The 52-week trailing earnings of the DJIA are thus falling giving the impression that another earnings recession is upon us.

The 52 week trailing EPS of the DJIA will finally shake off the Q4 2017 EPS in early 2018. In the meantime, the quarterly comparative EPS should start to show the positive impact of the new taxes in early April 2018 as Q1 2018 EPS are reported. This should be on both a 1st quarter 2018 basis over 4th quarter 2017 basis as well as year over year.

This false earnings recession, along with rising T-bond yields, seems to have triggered automatic selling by algorithmic traders and other machine-driven decision makers, which have been programmed to act when EPS drop and multiples soar well outside pre-set bounds. Selling begets selling as fear spreads.

Such selling is considered unwarranted. While it may take a little time to settle down as algorithms are adjusted to recognize the temporary nature of the EPS recession, the upward pressure on the price of the DJIA should continue back toward equilibrium as the dividend of the DJIA continues to make new records as earnings improve and the repatriation of foreign profits gather apace.

The dividend-discount value, at 37,845, is still well above its price of 24.798. The sell-off that is occurring should be used to buy the DJIA. So, buy now and new highs should be seen later this quarter and early in the second quarter of this year with a DJIA price of 30,000 still a distinct possibility in 2018 and 40,000 in 2019 as headline EPS recover and dividends continue to rise to new record levels.

The Fed Model and the Dividend-Discount Model

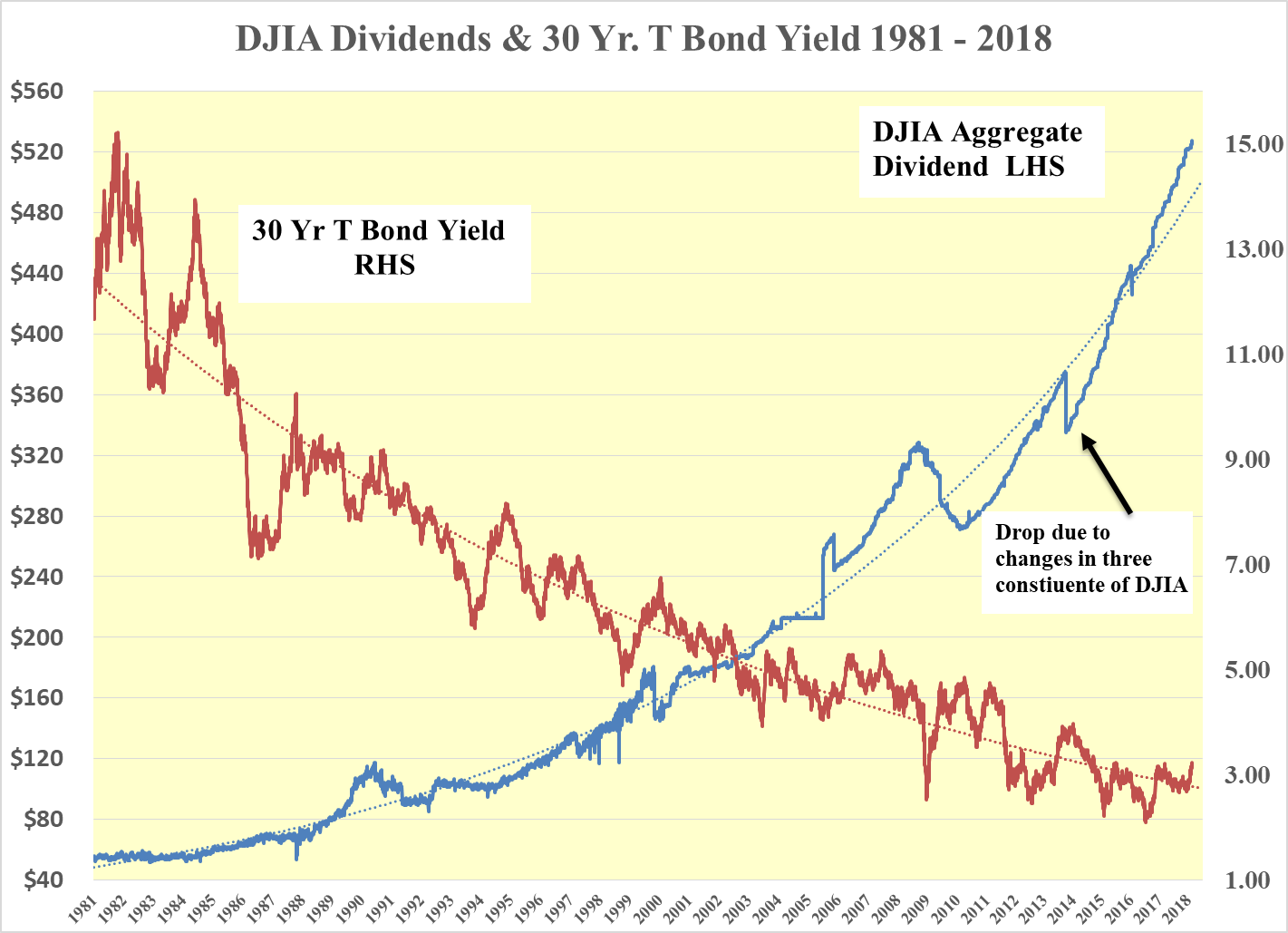

In the Fed model, the value of the DJIA is impacted by changes in long bond yields and earnings. One of the two vectors impacting value in the dividend-discount model is also the level of the long bond yields, the other is the DJIA dividend.

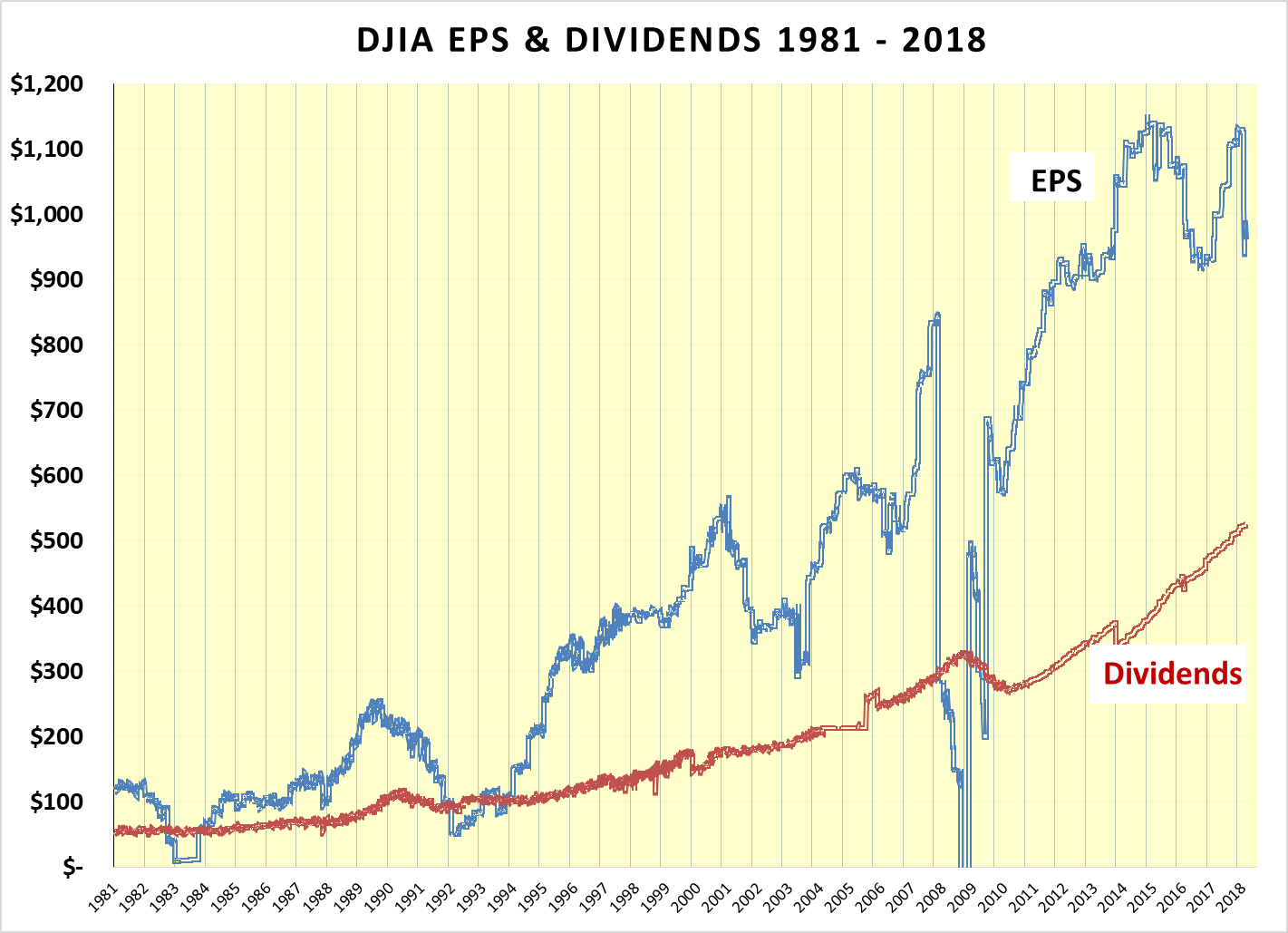

Over time the DJIA dividend has been much more stable than earnings and thus the vector of choice.

The Fed Value vs. Dividend-Discount Value

Since the end of last year, the 30 year T bond yield has risen from 2.74% to 3.22% on February 21, 2018. This has negatively impacted both the dividend-discount value and the Fed value by the same 15%. To this must be added the impact of the changes that have taken place in reported earnings, which are down 15% and dividends, which are up 1.2%.

The dividend discount value has fallen by 6,100 from 43,945 to 37,845 while the Fed value has fallen 11,346 from 41,245 to 28,898, a level comparable to the Fed value reached in December 2016. Both values, however, are still well above the price of the DJIA of 24,798.

While falling headline earnings are reminiscent of the 2007-2009 period, they result mainly from write-offs and adjustments arising from changes in the new U.S. Tax Act. These reductions will continue to be a drag on trailing 52-week earnings through the fourth quarter of 2018. However, the benefits of the tax changes should come shining through by early April 2018.

Falling earnings are often seen as a precursor to falling dividends and in the case of General Electric, this has been the case. However, the one-off, write-downs by Goldman Sachs, Johnson & Johnson and others are not expected to result in dividend cuts for the DJIA as a whole. Rather the repatriation of foreign earnings should result in a significant dividend boost.

This year, falling DJIA earnings along with their high P/E multiples should be downplayed and dividends favored when valuing the DJIA. In accordance with this, the dividend-discount value of the DJIA value remains well above its price and continues to put upward pressure on it. This should soon result in the price of the DJIA resuming its charge to new high ground.

Sources: Chart created by author from FRED and Dow Jones Data