These Toymakers Are Expected To Miss Big This Week, And 5 Other Earnings Surprises

Keeping with the trend of the early earnings season (and with historical trends), far more companies reporting this week are expected to beat on EPS expectations than miss. There are seven names in particular this first peak week of earnings that are on our radar. Four are anticipated to be beats and three are expected to be misses.

The Beats

To determine possible positive surprises we look for companies that have the following characteristics: 1. Large positive deltas vs. Wall Street 2. Significant upward revisions momentum into the report 3. Positive YoY growth expectations 4. A long history of beating 5. A long history of Estimize accuracy vs. the Street

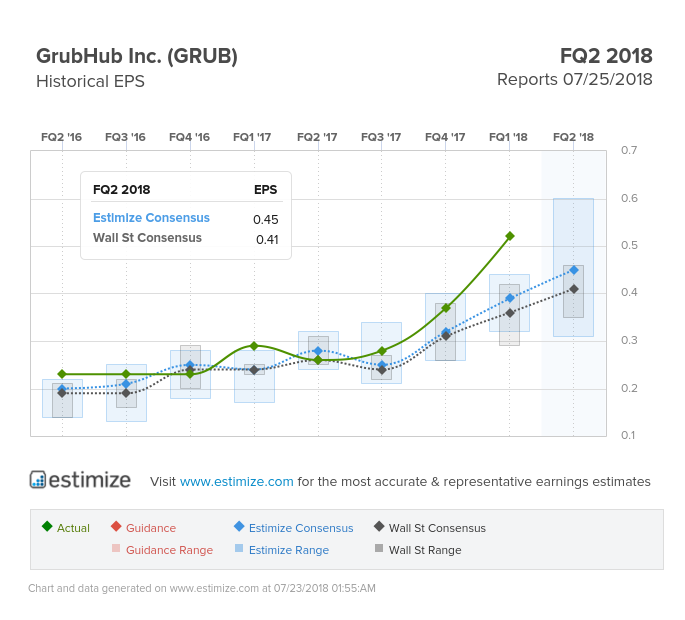

GrubHub (GRUB)

Information Technology - Information Technology & Services | Reports July 25, before the open.

The Estimize community is looking for earnings per share (EPS) of $0.45 when GrubHub reports on Wednesday, revised upward by 14% in the last 3 months and 11% higher than Wall Street’s $0.41. Revenues are also expected to come in higher at $234.6M as compared to the sell side’s consensus of $232.6M. Year-over-year (YoY) EPS and revenue growth are expected to come in healthy at 75% and 48%, respectively. GRUB tends to move up an average of 7% in the 30-days post earnings release. This is also a name that tends to beat the Estimize consensus 67% of the time on EPS and 73% on revenues, and that Estimize is more accurate than Wall Street on 60% of the time on EPS and 73% on Revenue.

While EPS and revenues are important for GRUB, it’s Active Diners that investors will be eager to hear about. Right now the Estimize community is anticipating Active Diners to come in at 15.6M for Q2, an increase of 70% YoY. While this metric came in better than expected last quarter, food sales and daily active orders did not. Still, the company raise guidance for Q2, and hopes to benefit from a healthy US consumer as well as partnerships such as the recent one with Yum! Brands (YUM).

Advanced Micro Devices (AMD)

Information Technology - Semiconductors | Reports July 25, after the close.

The Estimize community is looking for earnings per share (EPS) of $0.14 when AMD reports on Wednesday, revised upward by 38% in the last 3 months and 12% higher than Wall Street’s $0.12. Revenues are also expected to come in higher at $1.759B as compared to the sell side’s consensus of $1.718.B, a number that has been revised upward by 14% since last quarter. Year-over-year (YoY) EPS and revenue growth are expected to come in healthy at 595% and 44%, respectively. AMD tends to move up an average of 6% in the 30-days post earnings release. This is also a name that tends to beat the Estimize EPS consensus 58% of the time, and that Estimize is more accurate than Wall Street on 58% of the time.

Competition between Advanced Micro Devices and Nvidia (NVDA) has started to heat up, with sales of AMD’s brand of APUs and CPUs, Ryzen, up 60% last quarter. Gross margins will also be important to watch again this quarter, with Estimize expecting them to come in at 37.16%, demonstrating a continual upward growth pattern over the last 4 quarters. The one area of concern revolves around their graphic card segment which has been hurting due to declining cryptocurrency prices.

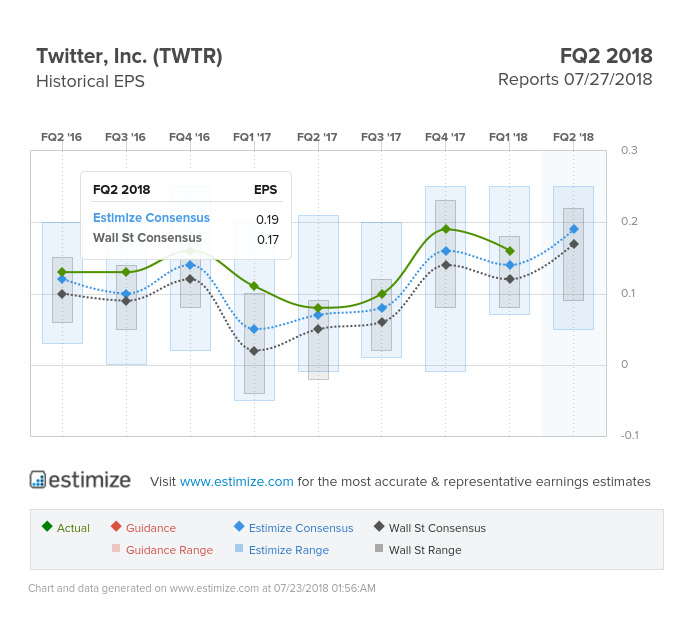

Twitter (TWTR)

Information Technology - Internet Software & Services | Reports July 27, before the open.

The Estimize community is looking for earnings per share (EPS) of $0.19 when Twitter reports on Friday, revised upward by 35% in the last 3 months and 9% higher than Wall Street’s $0.17. Revenues are also expected to come in higher at $708M as compared to the sell side’s consensus of $700M, a number that has been revised upward by 11% since last quarter. Year-over-year (YoY) EPS and revenue growth are expected to come in healthy at 132% and 23%, respectively. Twitter tends to beat the Estimize EPS consensus 85% of the time, and Estimize is more accurate than Wall Street 95% of the time.

The big number to watch with the social media names is always monthly active users (MAUs). This quarter the Estimize community is looking for TWTR to report MAUs of 340.3M, a slight increase of only 4% YoY, keeping in line with their longtime trend. Those estimates have remained mostly steady, even after analysts and investors worried that a recent move to suspend millions of accounts in order to remove malicious actors from the social network and improve the “health of the service” according to CFO Ned Segal.

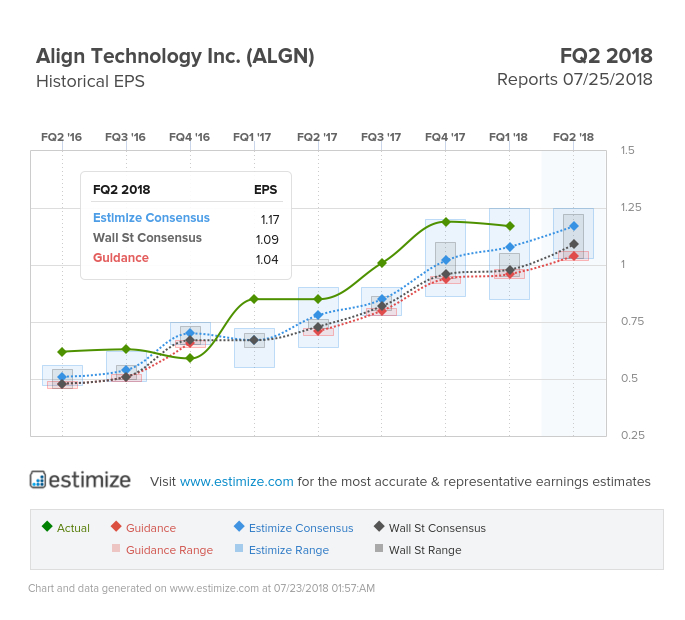

Align (ALGN)

Health Care - Health Care Equipment & Supplies | Reports July 25, after the close.

The Estimize community is looking for earnings per share (EPS) of $1.17 when Align reports on Wednesday, only revised upward by 2% in the last 3 months and 7% higher than Wall Street’s $1.09. Revenues are also expected to come in higher at $479.2M as compared to the sell side’s consensus of $469.2M, a number that has been revised upward by 5% since last quarter. Year-over-year (YoY) EPS and revenue growth are expected to come in healthy at 38% and 34%, respectively. ALGN tends to move up an average of 4% in the 30-days post earnings release. This is also a name that tends to beat the Estimize EPS consensus 74% of the time, and that Estimize is more accurate than Wall Street on 87% of the time.

Align is expected to continue to benefit from a healthy US consumer that is willing to spend discretionary income on health and wellness products. Total Invisalign shipments for Q2 are anticipated to come in atl 302,590, an increase of 11% QoQ and 29% YoY.

The Misses

To determine possible negative surprises we look for companies that have the following characteristics: 1. Large negative deltas vs. Wall Street 2. Significant downward revisions momentum into the report 3. Negative YoY growth expectations 4. A long history of missing 5. A long history of Estimize accuracy vs. the Street

The toymakers - while Hasbro and Mattel have been suffering for several quarters now, the bankruptcy of Toys R Us earlier this year has really exacerbated those losses, and both are expected to be two of the worst reporting companies this week.

Hasbro (HAS)

Consumer Discretionary - Leisure Equipment & Products | Reports July 23, before the open.

The Estimize community is looking for earnings per share (EPS) of $0.29 when Hasbro reports tomorrow morning, revised down by 49% in the last 3 months and lower than Wall Street’s $0.30. Revenues are also expected to come in lower at $837.9M as compared to the sell side’s consensus of $844.2M, a number that has been revised downward by 14% since last quarter. Year-over-year (YoY) EPS and revenue growth are expected to come in at -46% and -14%, respectively. This name tends to beat the Estimize EPS consensus 69% of the time, but only beats on revenues 42% of the time. Estimize is more accurate on EPS 69% of the time, an 58% of the time on revenues.

Mattel (MAT)

Consumer Discretionary - Leisure Equipment & Products | Reports July 25, after the close.

The Estimize community is looking for earnings per share (EPS) of -$0.35 when Mattel reports tomorrow morning, revised down by 163% in the last 3 months and lower than Wall Street’s -$0.32. Revenues are also expected to come in lower at $859.7M as compared to the sell side’s consensus of $863M. Year-over-year (YoY) EPS and revenue growth are expected to come in at -149% and -12%, respectively. This name tends to beat the Estimize EPS and revenue consensus only 42% of the time.

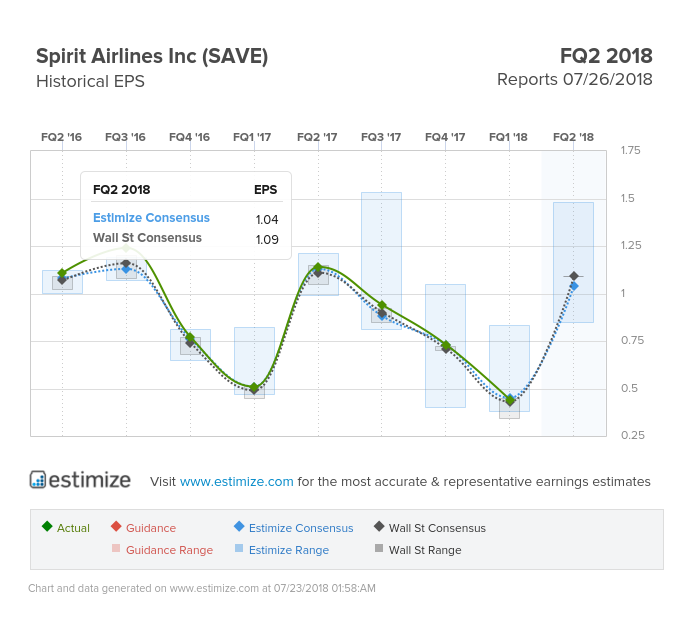

Spirit Airlines (SAVE)

Industrials - Airlines | Reports July 26, before the open.

The Estimize community is looking for earnings per share (EPS) of $0.99 when Spirit Airlines reports on Thursday, revised downward by 5% in the last 3 months and 9% lower than Wall Street’s $1.09. Revenues are also expected to come in lower at $845.5M as compared to the sell side’s consensus of $851.8M, a number that has been revised downward by 1% since last quarter. Year-over-year (YoY) EPS and revenue growth are expected to come in at -13% and 21%, respectively. SAVE tends to beat the Estimize EPS consensus 70% of the time but revenues only 35% of the time. Estimize is more accurate on both 60% of the time.

While most of the the major airlines beat Wall Street expectations already this quarter, Delta, United and American all mentioned the pinch of higher oil costs. While those larger carriers have options to hedge against higher oil prices such as passing those costs along to the consumer, Spirit really has no way to hedge as an ultra low cost carrier that counts fuel as it’s biggest expense.

Disclosure: There can be no assurance that the information we considered is accurate or complete, nor can there be any assurance that our assumptions are correct.