The Shorts Have It All Wrong - Why You Should Buy Herbalife

That Herbalife Miss...

Herbalife's streak of beating earnings guidance every quarter since 2008 is over. They missed this quarter - not by much - but it is a miss for a company that seems to grow like topsy.

The shorts on Twitter/Seeking Alpha, having spent some time saying that the numbers don't matter (just the business model), are now claiming some victory on numbers. Herb Greenberg (the only regular short I really have a lot of time for) stated that he thought the numbers don't matter but he now wants to assert meaning in the numbers.

--

But lets examine them dispassionately.

Short-sellers in this stock (particularly Bill Ackman) have a thesis that the company is a con - a scam which requires endless new victims to sign up and buy a whole lot of inventory in the promise of getting rich. They assert that there are very few real customers. [In Bill Ackman's first presentation one of his staff suggested it was possible that there were no real customers.]

They want government intervention to shut the company down - but if it is a pyramid as such it will collapse on its own. New victims can't be found forever. In other words the shorts would like government intervention but they are not dependent on it.

My view (and the long view generally) is that there is a huge amount of real consumption and real consumption is easily visible. Go to a few Herbalife distributors and you will see daily consumption. Lots of it. (I have visited Herbalife distributors in multiple countries and spoken to many more and I have yet to visit a Herbalife distributor consistent with the Ackman thesis).

What you find is a sort of cult of weight loss. If you drink protein shakes and diet suppressing teas daily you will lose weight. The only problem is sticking to that diet. Enter Herbalife who provide a (for profit) community to help you to stick to that diet. The community combined with the shakes is the product.

Visit Herbalife distributors and what you see is very large numbers of people who have entered or aspire to enter a routine of "daily consumption".

You see repeat customers.

Repeat customers are central to the bull case. If you get more of them earnings can grow for a very long time. Moreover it is very hard (nay impossible) to argue that someone who buys $100 worth of product, then in two months buys $100 more, and two months later buys some more and so on for years is scammed in the Bill Ackman sense. They know what they are getting. They are not deceived.

In my view the network recruits vast numbers of people to the diet-cult. Most fail consistent with most diets. A small number become daily consumers and this tribe of daily consumers grows nearly continuously. Most of the sales of Herbalife are to the tribe of daily consumers - the sales to new recruits whilst important don't actually drive current quarter sales. [Some of these new recruits however will become daily consumers and drive sales for years.]

The bull case - and it is a very strong bull case indeed - is that the daily-consumption tribe will continue to grow at mid-single digit for a very long time. You could wake up in ten years and earnings be $30 a share and the stock (say) $600.

---

The problem with endless growth stories

Imagine a company growing 10 percent per annum with a very high return on equity (so little capital is needed for additional sales).

Moreover assume that the discount rate is 7 percent.

Then try doing a discounted cash flow analysis.

If you assume that the growth goes forever then the value of the company is infinite.

So you must quite reasonably assume that the growth stops at some point. And the value of the company depends critically on when the growth slows. If it slows in 30 years it makes sense to pay a very big PE ratio for the company now.

If it slows next year you will get crushed buying at a high price.

Herbalife has grown fast enough since 2008 that you can engage in fantasies as to its ultimate valuation. Revenue in 2008 was $2.3 billion. It is now over $5 billion. And until the first quarter of this year it was growing uninterrupted in every geography. And the growth was volume growth - not just revenue.

Moreover the potential market is huge: fat people. This company sells roughly 10 percent of the number of "meals" as McDonalds but it sells then to far fewer people (mostly daily consumers). The potential number of daily consumers is a large multiple of the current number.

The enormous growth does enable fantasies. This stock could be very good indeed.

--

Alas - the slowing down of Herbalife growth

Herbalife was growing, quite fast, in all jurisdictions in all quarters until very recently.

One year ago they published their volume growth and sales leaders numbers and they looked as follows:

Volume growth was 11 percent in North America, 16 percent in Europe, Middle East and Africa, 33 percent in South and Central America and 49 percent in China. It was 1 percent in Asia Pacific - which mostly means Malaysia. But that was after years of torrid growth.

Jokingly I suggest: try putting those numbers into your discounted cash flow analysis.

But the shorts would argue that the Chinese numbers are anomalous - they are just finding another billion people to scam. That seemed delusional. The sales growth in North America - the most mature market - and hence the one where the pyramid-style collapse should have already happened - was still double digit. [I concluded - and still believe - the shorts are slightly unhinged.]

Moreover the sales growth per active sales leader is increasing in many markets. This means that mid-level distributors are getting paid more. That makes for a happy network.

In the first quarter of this year Herbalife had its first slowdown of any kind. These numbers shocked me to the downside and my position has been smaller ever since.

Note the sales decline in Asia Pacific. This was the first sales decline in any region that I remember.

The point is that if sales are shrinking in one region they may in turn shrink in any region. It means the growth that seemed bullet-proof from 2008 to 2013 was no longer bullet proof.

Moreover the sales leaders grew faster than sales. This meant the income of mid-level distributors was starting to get pressured. This is not good news.

Still North American growth was high (9 percent, not double-digit) and China was off-the-scale good.

These are not the numbers of a stock trading at a 10 times forward price earnings multiple. But they are no-longer the numbers that allow me to indulge $1000 a share fantasies. To get to $1000 a share in any reasonable time-frame growth numbers have to be impregnable. They clearly showed some vulnerability.

The sales decline it appears was almost entirely in Malaysia where one explanation on the ground is that they had a new competitor. Malaysia was at the time the number one market in the world for Herbalife according to Google Trends. Trends in Malaysia had been unbelievably good.

Malaysia for the unaware (meaning most my readers) has a different typical Herbalife distributor to (say) New York. New York tends to have "nutrition clubs" which feel a bit like down-market coffee shops where people sit around and drink shakes.

Malaysia has boot camps.

The shtick is that you turn up in a public park on a weekend morning and you do fitness classes. The first class is typically free. They are hard work. Over time they sign you up for both paid fitness classes and Herbalife shakes.

There is a quid-pro-quo. The fitness classes also have evening social outings - dances which serve multiple functions: weight loss support, Herbalife cult-revival, matchmaking. There are several vidoes on YouTube of these.

The first is a picture of a (soft) exercise class in a park for overweight (mostly Muslim) Malays:

The second video shows something that I have never seen elsewhere - women in full Muslim dress dancing.

This is a different image of Herbalife: part bootcamp, part fitness club, part diet club, part dance party. There are many hundreds of people at some of these clubs. These are reasonable sized businesses.

There is one of these clubs in Sydney now - with a Malaysian upline. See the 24 Fit Club. It is clearly a Herbalife club - but the meal plan is only part of what they sell.

I always - and instinctively thought that the Malaysian model was better than the Latin American/New York model. Exercise plus diet shakes clearly works better than just diet shakes. [I have seen cycling groups associated with Herbalife clubs in Miami - so the models do change according to the skills and interests of the distributors.]

Anyway an ugly sales decline in Malaysia was a decent sized kick to the Herbalife fantasy. If sales declined sharply in one market because of competition - especially when the market looked so viable - they could decline everywhere. It was impossible to project growth forever.

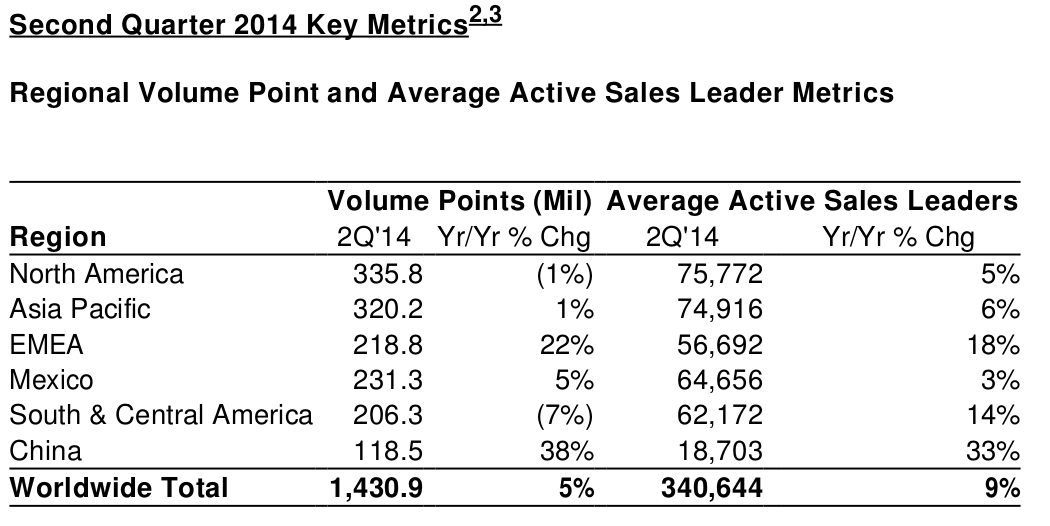

The 2014 second quarter earnings miss

This quarter the sales growth by region does not look anywhere near as good as in the past.

Notably there was a sales decline year on year in North America. That is a first. And there was a sharp sales decline South and Central America. This is clearly evidence that growth at this company is no-longer a given. Fantasies of enormous stock prices become more difficult to support.

However the observant will notice that Asia Pacific grew quite substantially (6 percent) quarter on quarter even if the annual growth rate was only 1 percent.

According to the short thesis this is not meant to happen. These things are meant to implode like Ponzis, not stage resurgences.

The resurgence is particularly notable because it seems that the competitor did not gain traction: the network effects of Herbalife are particularly strong. That is bullish.

Moreover whilst Herbalife sales have some seasonality (people want to lose weight for summer because of bikinis and the like) Malaysia is - climate wise - probably the least seasonal market possible. It is just hot there. So there is not a seasonal driver here.

Volumes are essentially flat quarter on quarter in North America. Its annoying and a challenge to the bull thesis but it is not disastrous.

By contrast the quarter on quarter declines in South America were quite sharp. I am wondering whether this looks like Malaysia last quarter or whether something else is happening. Whatever: as a Herbalife bull it is not good news.

Valuation

This stock remains less than ten times forward earnings. Volumes are still growing 5 percent though that volume growth is down from 14 percent a year ago and the numbers no longer look impregnable. Incremental ROE is high - and there is a huge runway for growth in Asia and China.

They buy back their shares with their profits.

The management are focused on returning profits to shareholders through buy-backs at least in part to drive out the shorts.

I can think of no other business with that sort of volume growth, such a high incremental ROE and equity shrink. This is a great stock.

Just not as great as it was before. The upside has shrunk. No question about it.

But I can imagine few worse shorts. I have visited many Herbalife distributors and the Ackman thesis is supported nowhere. And the shorts flit between the numbers not mattering and the numbers being critical.

The numbers do matter. They are not as good as they were. The upside is capped at a lower number but still closer to $200 a share than $100. I think I can wait. Just not as happily as before.

Disclosures: I purchased some in the morning of Ackman's speech. I turfed some later in the day (and I am not normally a day trader). I repurchased some of those in the after-market today. The ...

more