Saratoga CFO: Healthy Dividend, Lots Of Dry Powder

After speaking with the Chief Financial Officer (Henri Steenkamp) of Saratoga Investment Corp. for 40 minutes earlier this week, our main takeaway is that the 9.2% dividend yield of this small cap Business Development Company (BDC) is healthy (with room to grow) because the company continues to enjoy an attractive valuation (even after the shares strong rally so far this year), several important competitive advantages (for example, access to plenty of low-cost capital, aka “dry powder”), and may actually be less impacted by some of the big risks facing the BDC industry as a whole.

Overview:

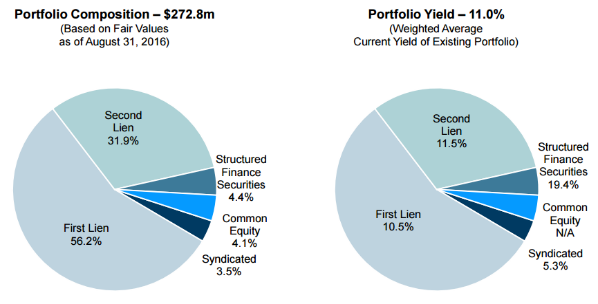

Saratoga Investment Corp (SAR) is a publicly traded BDC providing financing solutions to lower middle market companies through its SBIC-licensed subsidiary and a $300 million Collateralized Loan Obligation (CLO) fund. As the following chart shows, Saratoga’s portfolio is composed mainly of first and second liens, and the yields on these financing arrangements are significant (this is how Saratoga supports its healthy dividend).

And for reference, Saratoga’s investments are diversified geographically and across industries as shown in the following charts.

Dividend History:

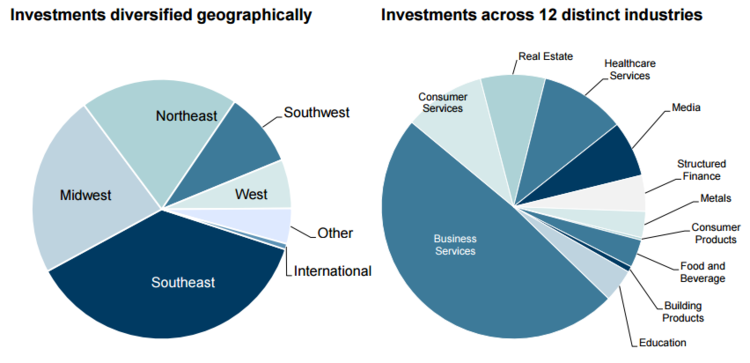

Understanding the recent evolution of Saratoga’s dividend is helpful in gauging its prospects going forward. For starters, when Saratoga first took over the BDC in 2010, the company was in distress, and management’s focus was on preserving capital. Saratoga was eventually able to offer a dividend that was paid 80% in stock and only 20% in cash. In 2014, Saratoga was able to move to a 100% cash dividend with the option of a dividend reinvestment program (DRIP) whereby the dividend could be used to purchase more shares at a discount to their market price (note: the market price is also trading at a discount to NAV, more on this discount later). The dividend has since then continued to grow (see chart below), plus Saratoga has recently paid an additional supplemental dividend of $0.20 (because they had extra income above and beyond the normal dividend amount).

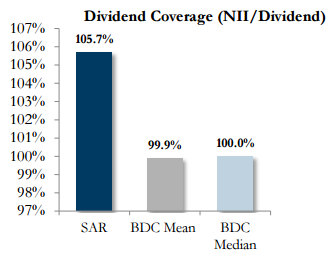

The relatively large supplemental dividend is a testament to the strength of Saratoga’s business, its conservative dividend policy, and a signal of more potential dividend increases ahead. For reference, this next chart shows Saratoga’s strong dividend coverage ratio relative to other BDCs.

Valuation:

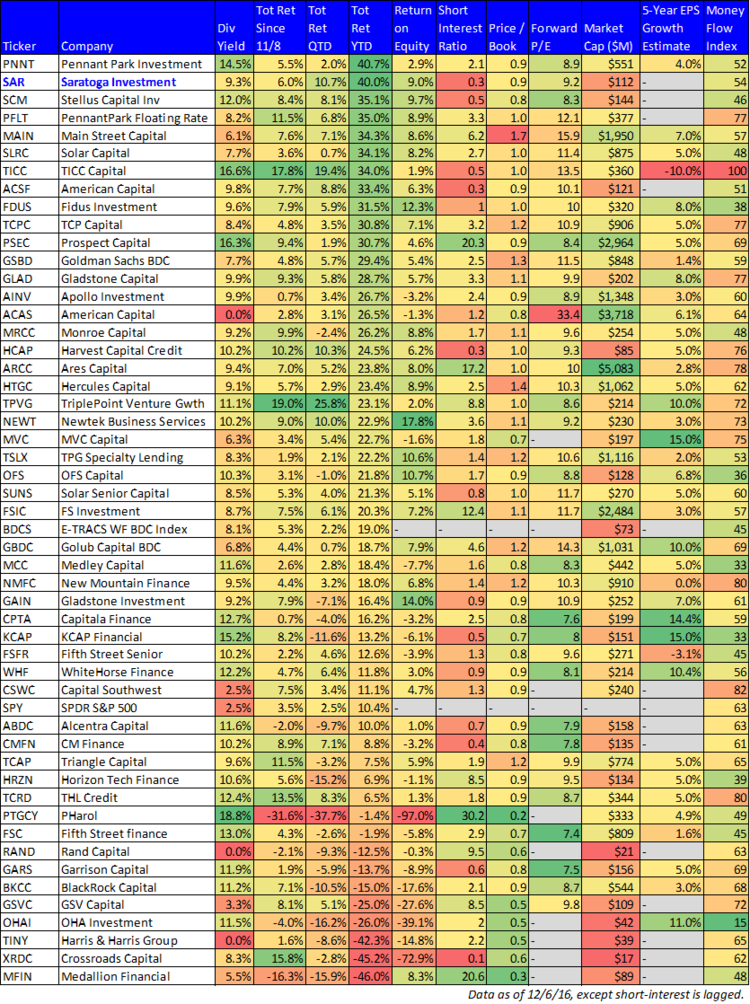

From a valuation standpoint, Saratoga currently trades at a discount to its net asset value (NAV). For some perspective, the following table includes Saratoga’s price-to-book ratio (+0.9) relative to other BDCs.

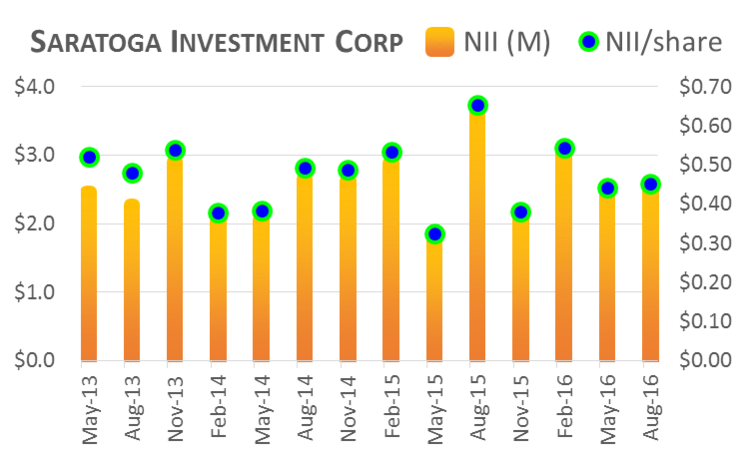

Another important metric to consider is Saratoga Net Investment Income (NII) as shown in the following chart.

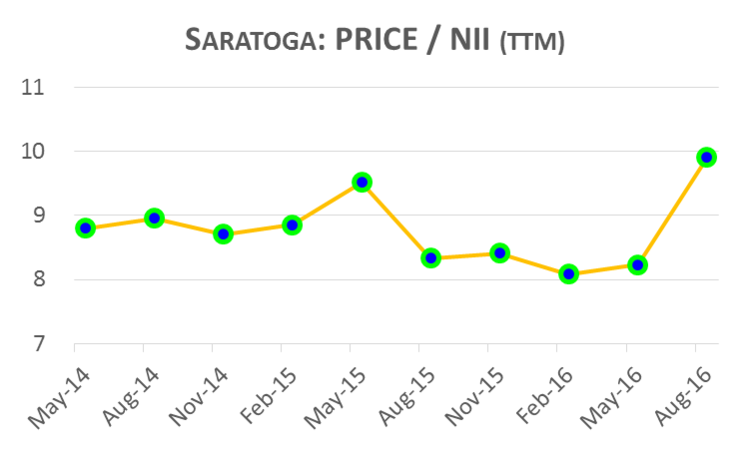

NII has not been growing, but it has been relatively steady. And in the case of Saratoga (as with most BDCs) the quality and safety of the income generating assets are far more important than simply growing big fast. Also worth considering, Saratoga’s price to NII ratio has been on the rise, but remains relatively reasonable as shown in the following chart.

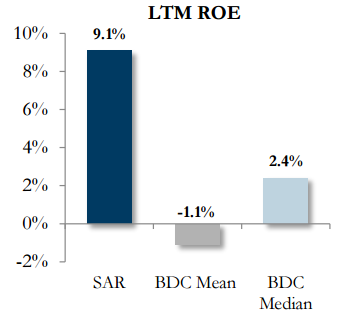

However, one short-coming of the price to NII valuation multiple is that it doesn’t include net realized gains and losses. Perhaps a more comprehensive metric is return on equity (ROE), and Saratoga stands out in this regard relative to its peers as shown in the following chart.

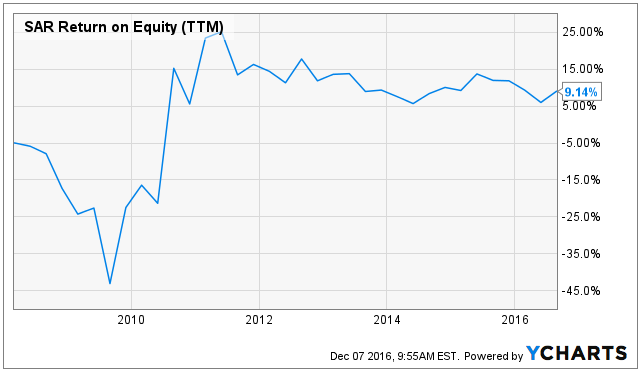

And for reference, the following chart shows Saratoga’s historical ROE (incidentally, this chart also shows the improvement since Saratoga took over the BDC in 2010).

Another way to gauge the value and safety of a BDC and its dividend is the dividend coverage ratio. And as shown in our earlier chart, Saratoga’s NII easily covers its dividend whereas many of its peers struggle.

Competitive Advantages:

SBIC License:

In addition to a reasonable valuation and a relatively safe dividend, Saratoga has several important competitive advantages, such as its SBIC-licensed subsidiary. For reference, according to the Small Business Administration, the SBIC program is…

A multi-billion dollar program founded in 1958, the SBIC Program is one of many financial assistance programs available through the U.S. Small Business Administration. The structure of the program is unique in that SBICs are privately owned and managed investment funds, licensed and regulated by SBA, that use their own capital plus funds borrowed with an SBA guarantee to make equity and debt investments in qualifying small businesses. The U.S. Small Business Administration does not invest directly into small business through the SBIC Program, but provides funding to qualified investment management firms with expertise in certain sectors or industries.

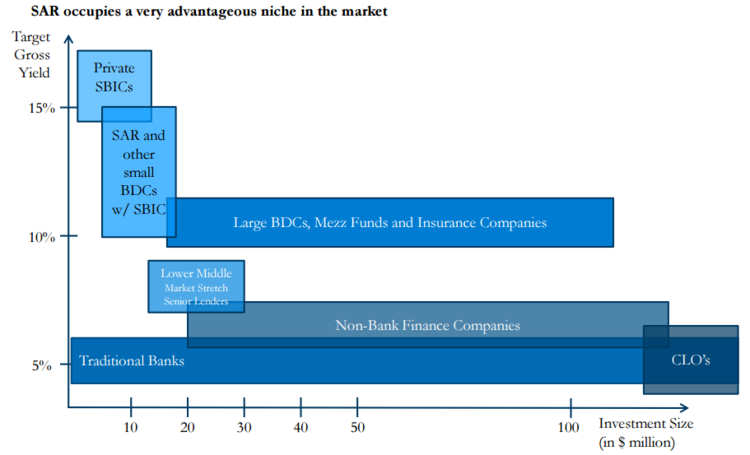

The reason the SBIC business is a valuable competitive advantage for Saratoga is because most other BDC are too big for such a program to make a difference. However, because Saratoga is relatively small (its market capitalization is only $112 million) the program provides access to very attractive capital in amounts that are significant enough to move Saratoga’s needle. Said differently, it’s a great business for Saratoga to be in.

Lots of Dry Powder:

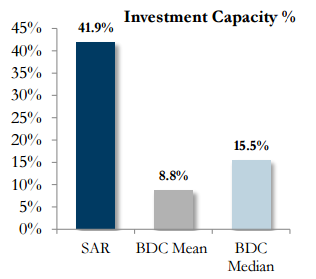

Another competitive advantage is Saratoga’s ability to grow its assets under management by 42% without any external capital. This sets Saratoga apart relative to its BDC peers as shown in the following chart.

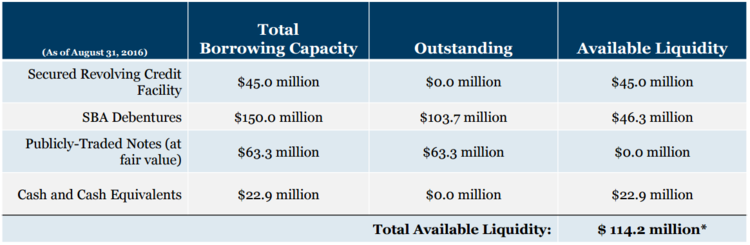

For more color, the following table shows Saratoga’s current borrowing capacity and available liquidity.

Saratoga has more capacity to fund growth under its Secured Revolving Credit Facility, SBA Debentures, and Cash and Cash Equivalents. Specifically, Saratoga benefits from its low-cost 10-year fixed SBA debentures and fixed cost covenant-free baby bonds.

Quality Portfolio:

Another competitive advantage is the high quality of Saratoga’s loans, which is something many other BDC’s do not enjoy. For example, over 99% of Saratoga’s loan investments have the highest quality internal credit rating (this was not the case when Saratoga took over the BDC in 2010), and Saratoga currently has zero loans in non-accrual. During our recent call, Saratoga’s CFO Henri Steenkamp explained:

“We’re not afraid to not grow in a quarter, our most important thing is not to sacrifice credit quality.”

This quote helps explains all the “dry powder” (quality over quantity) and the attractive quality of having zero loans in non-accrual.

Risks:

Rising Interest Rates:

Saratoga faces many of the same big risks as other BDCs, such as rising interest rates. However, Saratoga may be less impacted than some of its peers because of the way its balance sheet is structured. For example, all of Saratoga’s outstanding liabilities are fixed rate (for example, the SBA debentures are 10-year fixed rate). The only piece that would rise with interest rates is the credit facility ($0 outstanding), and rates must go up 125bps before that moves. And on the asset side, only ~18% is fixed (a good thing). However, ~60-70% of assets have floors. Essentially, on the asset side the first 100bps makes no difference versus the first 125bps making no difference on the liabilities side, and the liabilities piece is much smaller than the assets. Overall, as long as rising rates don’t significantly slow business, Saratoga is in good shape if/when rates rise.

Less Banking Regulation:

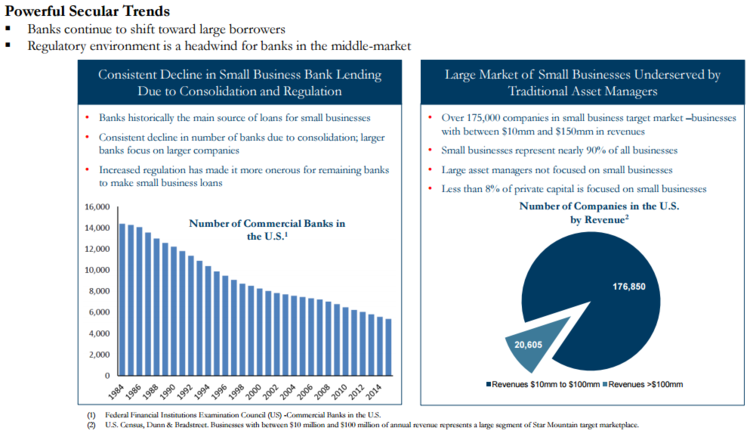

Another BDC industry wide risk is the possibility of less banking regulation. In particular, president Obama’s administration has aggressively pursued banks in the form of lawsuits and more regulations that prohibited risk taking as shown in the following charts.

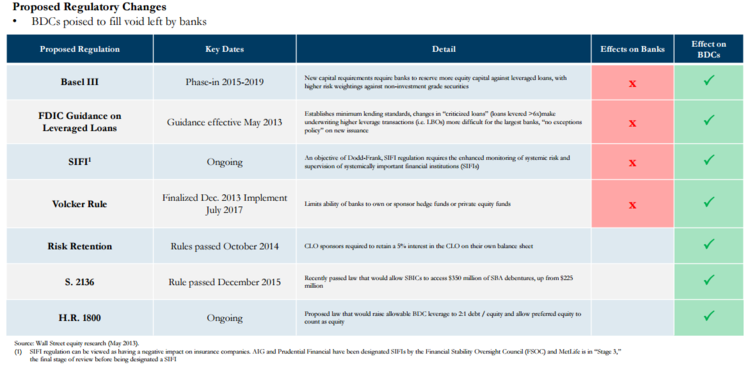

However, following Donald Trump’s recent victory the banking sector has soared, and this may be bad news for BDCs. Specifically, banks may be able to increase their lending to riskier middle market companies which would essentially mean less business and/or more competition for BDCs. However, Saratoga may be less impacted by this risk because of its niche position in smaller middle market companies that may be of less interest to big banks, and because of its SBIC license, as shown in the following chart.

Macroeconomic Headwinds:

Another big risk facing the BDC industry is a general economic slowdown. Because BDC generally lend to higher risk smaller business, they are often the most negatively impacted if/when the economy turns south. However as mentioned previously, Saratoga has very high lending quality standards (no loans are in non-accrual). Plus, we may see higher infrastructure spending and lower taxes from the new administration which could help the economy in general.

External Management Team:

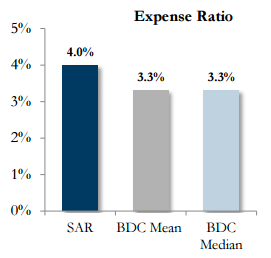

Even though most publicly traded BDCs are externally managed, this still presents potential conflicts of interest. One such conflict of interest/risk is higher expense ratios, of which Saratoga (externally managed) is not immune, as shown in the following chart.

However, a large part of the reason the expense ratio is high is because Saratoga is small relative to other BDCs, and this creates few economies of scale. As Saratoga continues to grow, the fixed costs will shrink as a percentage and the expense ratio will come down. Also worth noting, approximately 24% of Saratoga’s shares are owned by management, and an additional ~13% are owned by non-management insiders. This helps to align the interests of the external management team with shareholders.

Conclusion:

Over the last six years, Saratoga has evolved from a high risk company, to a relatively lower risk company with a healthy, growing dividend. Despite its strong year-to-date stock price performance, its valuation remains relatively attractive, as measured by its discount to NAV, healthy NII, and strong ROE. Further, it has several competitive advantages and may be less exposed to the risks faced by other BDCs. We don’t currently own shares of Saratoga, but we’ve added it to our Blue Harbinger watch list, and may consider a future purchase should the shares show any significant weakness.

Disclosure: None.