Puma Biotech: Is It Time For This Kitty To Roar?

Full steam ahead. Cantor Fitzgerald’s Alethia Young sees a promising future for this groundbreaking cancer-focused biotech stock.

If you haven’t heard of Puma Biotech Inc (PBYI– Research Report) before, this is a small-cap biotech definitely worth watching. Top-rated analyst Alethia Young (Track Record & Rating) has just initiated coverage of Puma with an Overweight rating and 12-month price target of $75. This means that shares could potentially surge just over 70% upside from current levels.

Puma is an oncology company with drug Nerlynx approved for HER2 positive adjuvant breast cancer. But the market has yet to appreciate the drug’s full potential: “We believe that the company’s first oncology drug Nerlynx will become a bigger product than what investors currently expect. We estimate peak sales of close to ~$1B, while the current market cap is $1.8B” states Young.

This creates an intriguing investing opportunity for investors. Although investor debate is high on Nerlynx, she thinks the drug will continue to grow in the US and Europe. “We believe that there is a disconnection with our expectations vs the current valuation because there are still concerns around trends related to the Nerlynx launch.”

Most critically, investors are concerned that the Nerlynx launch will slow due to more patients discontinuing after their 12-month cycle of treatment and fewer numbers of new patients will start drug. However since the 2017 launch, the drug has already enjoyed ‘moderate success’and is on track to achieve its guidance of $175-200M in revenues for 2018 (perhaps even with some modest upside to boot).

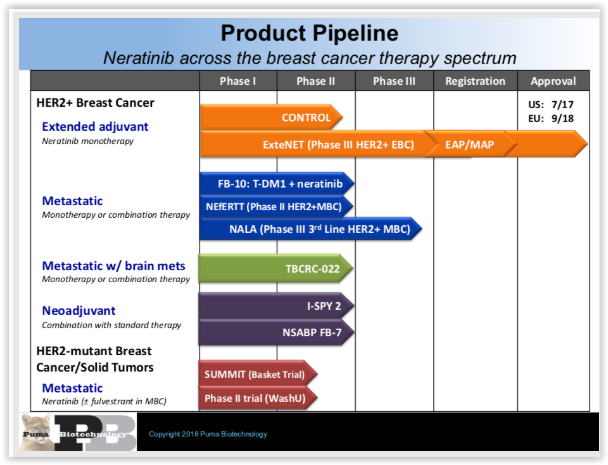

“We are still bullish on Nerlynx’s long-term potential and have greater conviction after following the launch so far” she says. Providing a handy boost is the fact that the drug has also now received European approval. This means that the drug should launch there in 2019, generating peak sales of $375M. Also in the background are further trials for the same drug but in metastatic breast cancer (a peak annual opportunity worth about ~$200-300M). Here we can the full range of the company’s current pipeline:

Also worthy of note: PBYI currently trades at significant discount vs peers based on EV/S multiples. This is despite the fact that Nerlynx’s clinical efficacy data in adjuvant setting look better than competitor Roche’s Perjeta data seen in the APHINITY trial.

Word On The Street

Overall, top analysts have a ‘Moderate Buy’ consensus rating on Puma stock. This comes with a $75 average analyst price target (68% upside potential). Also in the stock’s favor, note that the highest price target comes from Guggenheim’s Michael Schmidt- a five-star analyst who just initiated PBYI coverage with a bullish $85 price target (90% upside potential).

(Click on image to enlarge)

In contrast, the stock’s most bearish Sell rating- and lowest price target- comes from the worst-performing analyst.