Parsing Yesterday’s Stock Market Slide

No one knows if yesterday’s 3%-plus plunge in US equity prices is noise or the start of an extended decline. What we do know is that the slide wasn’t entirely unexpected given the strong relative and absolute performance of US stocks in recent history.

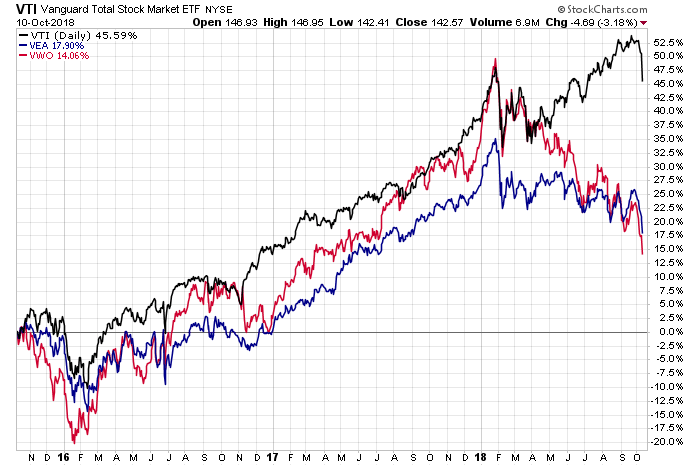

As noted in Monday’s review of global markets through an ETF lens, equities in the US have been on a tear lately. As of last week’s close, Vanguard Total Stock Market (VTI) was up more than 14% for the past year vs. a roughly flat performance for foreign stocks in developed markets (Vanguard FTSE Developed Markets ETF (VEA)) and a roughly 10% loss for emerging-markets equities (Vanguard FTSE Emerging Markets ETF (VWO)), as of Oct. 5.

Longer-run windows also show a dramatic edge for US equities. For the trailing three-year window, for instance, VTI is still up sharply (annualized 11.1% return) vs. VEA and VWO (+2.6% and +1.9%, respective), even after yesterday’s rout.

The divergence in favor of the US market has been particularly striking since March. While foreign equities have been trending down for months, US stocks have been consistently making new highs – a mismatch that’s gone to extremes…until yesterday.

History tells us that while large divergences are possible at times, they’re unsustainable. What was the source of the divergence? Maybe the crowd had assumed that an extraordinary economic boom in the US would carry the day. Whatever the explanation, a huge gap unfolded in performance between the US and the rest of world – a gap that was destined to close at some point.

“The sharp rise in US 10-year yields has caused investors to suddenly reprice the impact of moving from post-crisis low yields to a rising rate environment,”advises Eleanor Creagh, a strategist at Saxo Capital Markets in Sydney. “We have the global growth engines, price of energy rising, price of money rising and quantity of money falling combined with the ongoing trend of de-globalization which has started to impact markets and the cracks are showing.”

Analyts at ANZ agree, opining that “equity markets are locked in a sharp sell-off, with concern around how far yields will rise, warnings from the IMF about financial stability risks and continued trade tension all driving uncertainty.”

The question from a US perspective is whether an extended slide in stock prices is warranted? Quite a lot of the answer will be based on the economy. For the moment, the numbers still look encouraging. Recession risk remains virtually nil, as noted in this week’s update of the US Business Cycle Risk Report, based on data published through Oct. 5.

Meanwhile, the outlook for the immediate future remains upbeat, based on the latest nowcasts for third-quarter GDP, which is due later this month’s in the government’s preliminary Q3 update. The Atlanta Fed’s GDPNow model (as of Oct. 10) points to another strong quarterly gain, projecting a 4.2% rise in output for the three months through September. The New York Fed’s Q3 nowcast (Oct. 5) is considerably softer via a 2.3% estimate, but it’s safe to say that both numbers strongly suggest that the nine-year US expansion will roll on for the foreseeable future.

If the economy continues to grow, there’s a reasonable case for seeing any slide in stock prices as a buying opportunity rather than a signal that an extended bear market is upon us. Ongoing rises in interest rates could temper a rebound in equities, but as long as yields are trending up due to solid economic activity it’s reasonable to assume that the big picture for stocks remains productive. Expected returns may no longer be stellar, although the further stocks fall the better the outlook.

The usual caveats apply, of course, but the first order of business for putting a market tumble into perspective is monitoring how the macro trend evolves. By that standard, it’s premature to assume the worst. By contrast, if the incoming data reveals that the macro profile is deteriorating, we may be looking at more than a “normal correction,” as US Treasury Secretary Steven Mnuchin characterized yeseterday’s sharp decline in the stock market.

Disclosure: None.