Matinas Initiates Important Phase 2 Study With MAT2203

TM editors' note: This article discusses a penny stock and/or microcap. Such stocks are easily manipulated; do your own careful due diligence.

On November 21, 2016, Matinas BioPharma Holdings, Inc. (MTNB) announced the commencement of dosing in a Phase 2 clinical study examining MAT2203 in patients with vulvovaginal candidiasis (VVC). MAT2203 is an orally-administered, lipid-crystal nanoparticle formulation of amphotericin B. This is an important step for the company's lead pipeline candidate and should provide further clinical evidence of MAT2203 activity against candida infections. Below is a quick review of MAT2203 and my thoughts on why this VVC study is so important.

The Phase 2 Program

The Phase 2 study is a randomized, multicenter, evaluator-blinded study of oral MAT2203 compared to oral fluconazole in adult female patients. Approximately 75 patients with a diagnosis of moderate to severe VVC, more commonly known as "yeast infection", will be enrolled and randomized into three treatment cohorts of 25 patients each. The first cohort will receive treatment with 200 mg of oral MAT2203 while a second cohort will receive 400 mg of oral MAT2203. The third cohort will be treated with 150 mg of oral fluconazole as an active control.

The Phase 2 VVC study is designed to assess the efficacy, safety, and tolerability of MAT2203 in this otherwise healthy population. The results will provide Matinas with excellent balance / juxtaposition to the going Phase 2a NIH study. As a reminder, the NIH/NIAID is currently studying MAT2203 in a Phase 2a open-label, dose-titration study for the treatment of mucocutaneous candidiasis in immunocompromised patients who are refractory or intolerant to standard non-intravenous therapies. These are patients with advanced cancer, organ transplant, or viral infection that no longer respond to oral azole treatment.

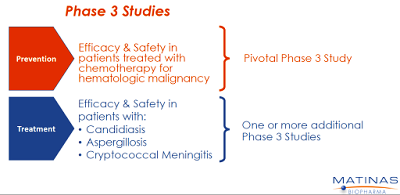

A third Phase 2 study is expected to begin shortly. In this study, Matinas will analyze the multiple dose safety, tolerability, and PK study in patients with mucocutaneous candidiasis undergoing treatment for hematologic malignancies such as leukemia. This study will include patients being treated with the chemotherapy regimen that typically induces neutropenia, causing suppression of the immune system and subsequently puts patients at risk for developing an invasive fungal infection (IFI).

An Astute Strategy

The three Phase 2 trials make up an astute development plan for Matinas.

→ Results of the VVC study should allow management to show the FDA that MAT2203 is safe and works to kill Candida in otherwise healthy individuals with normal immune systems.

→ The NIH study should allow management to show the drug is safe and works to kill Candida in severely immunocompromised patients refractory to other treatment options.

→ Finally, the third study is designed to show safety, efficacy, and pharmacokinetics in the target population for Phase 3, i.e. patients on chemotherapy with a hematologic malignancy such as leukemia.

The first study is an acute, likely uncomplicated infection. The second is a chronic, life-threatening infection. Either way, Matinas wants to show MAT2203 works! If Matinas can show proof-of-concept with MAT2203 against Candida in both instances, and demonstrate it is safe in chemotherapy patients with leukemia, things get very interesting from a market perspective.

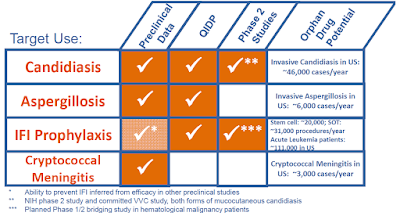

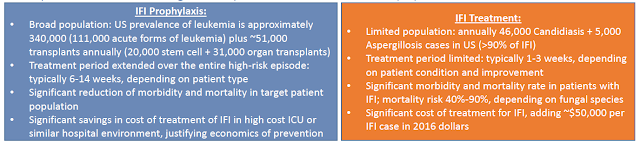

Recall, Matinas would like to develop MAT2203 as a prophylactic. The primary goal of the Phase 2 program is to put together a package for the U.S. FDA that outlines a path to approval for the prevention of invasive fungal infections in at-risk patients with hematologic malignancy. This is the indication for which MAT2203 was granted QIDP designation in September 2016.

Matinas would like to have this meeting with the FDA in the second half of 2017 because the goal is to start the Phase 3 program in 2018. The first patient in the NIH study was dosed in early October 2016. The trial should only take a few months to complete and topline data are expected during the first half of 2017. The VVC study that just got underway will likely take a few extra months, but topline data are still expected around the middle of 2017 because dosing will be only a few days (likely 4-5). I think the company is on track with its plan.

Gearing Up For Phase 3

I expect the first Phase 3 trial will be a 400-500 patient study to evaluate the efficacy and safety of MAT2003 versus a control group for the prevention of IFI in patients with hematologic malignancy being treated with a chemotherapy and the second will be in the treatment of invasive fungal infections in patients with hematologic malignancy. Matinas is trying to position MAT2203 to be the first drug of choice for Candida, either with an active infection or in patients at risk of infection.

Follow-up programs with Aspergillosis and Cryptococcal Meningitis are also expected. Similarly, Matinas is trying to position MAT2203 to be the first-line drug of choice for any patient either with or at risk for an invasive fungal infection. Management thinks they have the ideal drug and the Phase 3 program will look to build upon the foundation from the Candida studies and the impress preclinical and Phase 1 data.

Enormous Market Opportunity

Amphotericin B (AmB) work by binding to ergosterol, a component of the fungal cell membrane, which leads to increased cellular permeability and inhibition of fungal cell growth. AmB has activity against a broad spectrum of invasive fungi, and thus it is the standard of care for many systemic fungal infections. The drug is fungicidal, which means it kills the invading fungal infection, as oppose to azoles like fluconazole or voriconazole that are fungistatic (only halt the spread of the infection). Unfortunately, the high toxicity of intraperitoneal amphotericin B, which shows up at around 1 mg/kg is roughly equal to the therapeutic dose, thus creating a very small therapeutic window for the drug.

Gilead's liposomal formulation, AmBisome® (LAmB) has improved tolerability up to the 10 mg/kg range. However, early work done with MAT2203 (CAmB) shows that oral delivery of the resulted in no overt adverse events at doses up to 90 mg/kg in animal studies; and in a mouse model of Candidiasis (Santangelo R., et al., 2000), CAmB was superior to LAmB. It seems that Matinas has figured out a way to greatly improve the therapeutic window for an incredibly powerful drug.

It is clear that AmB use today is limited because of the nasty and sometimes lethal side effects of the drug, including nephrotoxicity, hepatotoxicity, risk of anaphylaxis, and anemia. As a result of this toxicity, AmB is primarily used either very early on in the treatment paradigm until toxicity shows up, or as a last resort for patients with few other options. Because the drug is administered via intravenous infusion, there is no out-patient use. As a result, when patients leave the hospital, they often leave on less effective azoles or echinocandins. Despite these limitations, the drug did $500 million in sales in 2014.

In 2013, Pfizer (PFE) reported $775 million in sales of voriconazole (Vfend®), while Merck (MRK) reported $309 million in sales of posaconazole (Noxafil®). The former market leading product, Pfizer's Diflucan® (fluconazole), now available as a generic, reported peak sales of $1.17 billion in 2003. In 2013, Merck reported $660 million in sales of caspofungin (Cancidas®) while Astellas reported $307 million in sales of micafungin (Mycamine®). These are less effective drugs with usage far greater than AmB due to the fact that they are much less toxic.

The value proposition for MAT2203 is simple. Infectious disease doctors would like to prescribe an oral amphotericin B product both in the hospital and after the patient goes home, in a broad population, without overt fears of nephrotoxicity or anaphylaxis. AmB, a fungicidal drug, has significantly less developing resistance, unlike what is now being seen with azoles and echinocandins. I believe this is something payors will look very favorably upon, as long hospital stays and resistant infections add significant cost to the system.

I believe an orally-available encochleated amphotericin B could have tremendous uptake. As noted above, Pfizer's Diflucan® (fluconazole) posted peak sales of nearly $1.2 billion, and the drug is far less powerful than AmB. Matinas is astutely studying MAT2203 head-to-head vs. Diflucan in the planned Phase 2 VVC study noted above. If successful, this sets up MAT2203 as a potential for a paradigm shift in how invasive fungal infections (IFI) are treated in this country. Of course, this is all highly contingent upon clinical trial results.

The IFI prophylaxis market is an enormous potential opportunity for Matinas. Mostly all medications today are limited to active infections and dosing typically only lasts for 1-3 weeks. Despite high mortality rates, a typical course of treatment may still run in excess of $50,000. The IFI prophylaxis market is 7X the size in terms of the number of patients. Treatment is also expected to run concurrent with chemotherapy and last as long as 6-14 weeks. We are talking about a potential 20-50X increase in market size. This takes a multi-hundred million dollar opportunity, like AmBiSome's $500 million in peak sales in 2014, and turns it into a multi-billion dollar opportunity.

Conclusion

I am incredibly intrigued by MAT2203. The product has clear differentiating characteristics to existing formulations of AmB, an estimated $750 million market in the U.S. The leading formulation of AmB is Gilead's AmBisome®, a liposomal injection formulation that generated $350 million in sales in the U.S. in 2014. Global sales peaked at $500 million in 2014. MAT2203 looks to have superior safety and tolerability, targeted delivery, and oral administration. Importantly, AmB itself has broad-spectrum activity and limited drug-drug interactions, which all-in makes me think MAT2203 is a potential blockbuster (sales in excess of $1 billion) if approved.

In terms of valuation, successful completion of the MAT2203 Phase 2 program is expected to validate this blockbuster market opportunity. Matinas currently trades with a market value of $100 million. Post the Phase 2 data expected by the middle of 2017, the asset could be worth $350-400 million in value. Importantly, Matinas has a second cochleate product, MAT2501, an encochleated formulation of the antibiotic amikacin, nearing Phase 1 studies

I think MAT2203 has peak sales of $1.25 billion, about the same size as Diflucan® (fluconazole) at Pfizer prior to the patent expiration. Below is a breakdown of my NPV analysis using only a 25% probability of approval, a 15% discount rate, and 5X multiple on peak sales. I've also increased the basic shares outstanding by 50% to account for future dilution and the planned financing of the Phase 3 program in 2018.

My valuation has no input for MAT2501 or MAT9001.

Despite all these aggressive measures, I still find the shares to be 150% under-valued today. Major catalysts are underway and I expect significant value inflection in the next 6-8 months.

Disclosure: Please see important information about BioNap and our relationship with MTNB in our Disclaimer.

more