Marko Kolanovic – a.k.a. “Gandalf”, a.k.a. the “half-man, half-God” – has a new note out and it’s great.

For the past couple of years, Kolanovic’s research has been hijacked by the doomsday crowd as part of that crowd’s ongoing attempt to justify a bearish lean that has been perpetually and decisively wrong for a solid decade.

It is of course by no means clear that Marko was a willing accomplice in that effort. Kolanovic’s legend has grown in proportion to the market’s interest in the risks posed by the systematic strategies he covers – i.e. risk parity, CTAs, vol. control funds, etc. etc.

His research is what it is. He documents the evolution of those strategies’ exposure and positioning and tries to draw conclusions. Some of his calls/musings have proved prescient and to the extent his implicit (and sometimes explicit) contention that these strategies pose something that approximates a systemic risk has been borne out during risk-off episodes that are exacerbated by systematic de-risking, those of a bearish persuasion are inclined to count Marko as one of their own.

Last month, the day before the above consensus AHE print that accompanied the January jobs report started tipping dominoes, Marko suggested that the market action from the late January highs through February 1 didn’t presage an imminent systematic de-risking episode. That prediction was proven wrong the following day and once Monday, February 5, rolled around and ushered in the short vol. ETP implosion, it was clear that what Marko had been warning about for years was indeed materializing.

And so, he did what one does when one is the business of trying to figure out what’s likely to happen next – he made a prediction. That prediction was pretty straightforward: the systematic unwind is behind us, buy the dip.

That didn’t go over particularly well with the doomsday crowd and to the extent Kolanovic saying “buy the dip” was a bitter pill for the permabears to swallow, that pill became increasingly bitter as the market bounced off the lows and rallied hard the following week, proving that Kolanovic was in fact right – again.

Well Marko would go on to kind of rub it in over the next three weeks and you can read excerpts from his multiple “I told you so” notes in our Kolanovic archive here.

Now just to be clear, we’re in the camp who employs cynicism and skepticism in each and every market-related post we run. That’s part of who Heisenberg is – it’s embedded in our DNA. But what we don’t do is continually predict that the epic crash which will usher in creative destruction and a final, “glorious” purging of misallocated capital is coming tomorrow. And the main reason we don’t do that is because the chances of that happening tomorrow or next week or next month are basically nil, which means that were we to go that route, the odds are overwhelmingly in favor of us being perpetually wrong day after painful day and week after painful week.

That leaves us free to keep an open mind when someone like Marko says “buy the dip.” So we very much enjoyed watching as Kolanovic continued to advise dip buying and was continually proven right, much to the chagrin of all the folks out there who just couldn’t fathom the idea that Marko would turn “bullish.”

That brings us neatly to his latest note which in many ways represents the final leg of his BTFD victory lap and he kicks it off in spectacular fashion by noting that the inflation scare narrative was “completely debunked” (he’s talking about the AHE miss and the inline CPI print) and then, he takes what certainly looks like a jab at certain “folks” with a reference to fearmongering “clickbait”. To wit, from Marko:

With the inflation scare completely debunked by recent data and bond yields only at ~2.80% (and bond shorts still ‘off the charts’), our views on risks and equity upside have been confirmed by markets. Recently, financial press stories were dominated by fear. This is perhaps understandable given a long period of extremely low volatility before the recent turmoil. Negative stories also tend to attract more attention (clickbait). After running through various negative narratives – inflation, stagflation, hyper growth, rollover of growth, large deficits, tariffs to reduce trade deficits – the most recent bear narrative is trade wars (and particularly one with China). We argue below that this risk is also very low, and if we take the 2015 turmoil as a template for flows from systematic and fundamental investors, markets are likely to reach all-time highs soon.

Again, that is all kinds of hilarious and props to Marko for “going there” because he knows that everyone reads his stuff, so there was no chance anyone was going to miss what amounts to this message for anyone who doubted his BTFD call from early February:

But it gets better – so much better.

Marko then goes on to address the current bearish narrative which of course revolves around the possibility that Trump may end up starting a global trade war. Obviously, that would be negative for markets and Kolanovic says it’s probably not going to happen for one simple reason. But before we get to that, here’s how he sets it up:

See the implication there? Strong words, but little to nothing in the way of action from Trump. So why would Trump eschew making good on his threats? Simple: because if he starts a “hot” trade war, he’ll end up tanking the stock market, putting himself in the decidedly tough spot of having to explain to his base why that equity rally that was so important for America last year, no longer matters this year.

To be clear, we’ve been saying this for months on end. That is, Trump has backed himself into a corner with the stock market balderdash. If you want our most comprehensive take on this, see our piece for Dealbreaker here, but here are a couple of excerpts:

The reason he’s doing this is because he doesn’t have anything else to point to in terms of “achievements” since his inauguration and so, he’s going to keep tweeting about record high stock prices in an effort to convince his base that i) record highs on the Dow are somehow meaningful to them, and ii) those record highs are somehow related to his presidency.

What I would note here is that he is digging his own grave, because to the extent he’s convinced his base that he is in fact responsible for the latest leg higher in equities, he is going to have to explain to that same base why stocks aren’t actually important to them in the event the market sells off.

That last bolded bit goes double if there’s a reason for people to believe he’s the proximate cause of the selloff.

Now that the mid-terms are just around the corner, the idea of a dramatic decline in equities is a non-starter. Because if that were to happen, it could bolster Democrats by removing one of the only things Trump can point to as evidence of his “success”. Well, if Democrats score too many victories, that bodes poorly for a President who is under fire from all sides. Here’s Kolanovic again:

Let’s note that there is a large asymmetry of the outcome rewards by participants. A significant trade war started by this administration would destabilize global equity markets. Should this happen ahead of the November election, it would impair the administration’s ‘market scorecard’ and likely lead to an election loss. Lost elections open a path to impeachment, and other complications.

Yes, “and other complications.” “Complications” which Trump is making even more “complicated” by the day with his ongoing effort to subvert the Mueller probe.

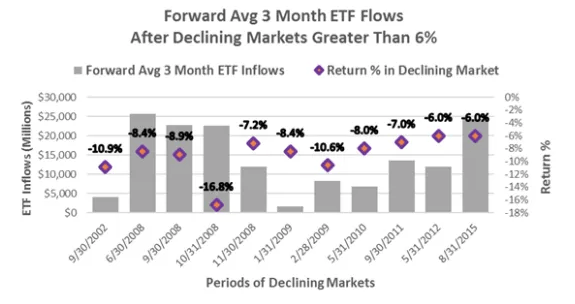

Finally, Marko reminds you one more time about what he “wrote in his previous research” on the way to drawing a parallel with August 2015 (when the Chinese yuan devaluation destabilized markets):

Throw some buybacks on top of systematic re-risking (as it were), and you’re in business where that means well on the way to a plausible bullish narrative (see here for the full buyback story and how it relates to the above).

So there you have it folks, “Gandalf” on BTFD, new highs, a game theoretic approach to the global trade war that will not, in his view, come to pass, and on the extent to which Trump needs the market to remain elevated in order to avoid impeachment “and other complications.”

Again, great note.

Comments

Log in or sign up to join the conversation.