Market Briefing For October 24, 2016

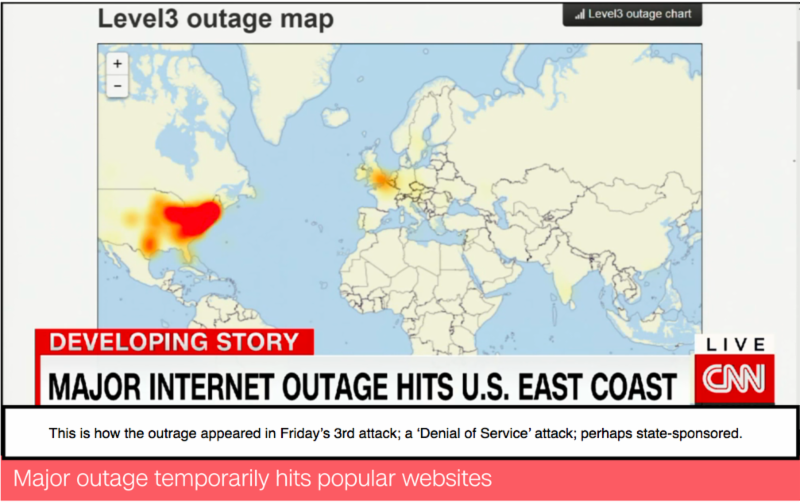

The term 'internet vandalism' is being used to describe the massive or crippling attack on many American websites on Friday. The character of this attack was different; as although it was a 'denial of service' type attack (which struck millions of IP Addresses); it was also an attack on the 'internet of things', which means it was 'new' in that it had potential to disrupt everything from a DVR to a camera on a phone or a toaster.

Though everything was restored by early evening Friday; the risk may have done humanity a service; by making a point that despite knowing of such threats, everything that has an IP Address needs some security which almost nothing outside of the computer realm has. Today there's an IP Address in 'smart TV's; in cars themselves; not just entertainment systems. No, incidentally; that's not why Tesla is in an evolving or slow downtrend, but as its competitors blossom (that's why we got just a bit tepid towards that company and its recent delay of new products for delivery; giving time for BMW, Mercedes and others to refine newer products); one will recognize a car can crash without physical damage. In-theory such cars better have complete security themselves.

One note about security. For years we've contended consumers have far better security with Macs than Windows computers; and today IBM (IBM), which has expanded their relationship with Apple (AAPL), noted they bought at least 30,000 MACS for IBM employees, aside from iPhones and iPads, and that over a three year period the more expensive computers cost 'less' if one considers software and IT support of the equipment. This is what I've pointed out for years as part of why Apple traditionally isn't beloved by IT departments or open-source requirements.

I contended a couple years back that the IBM relationship will elevate Apple a lot over the years in the business realm, as we see in medicine with apps provided by IBM. This has good long-term implications, and I suspect that while the crest of consumer PC's is behind the new and refreshed MACs coming on the 27th will be well-received. The iPhone 7 is however experiencing the 'bloom off the rose' syndrome a little, as everyone knows the next version is the serious upgrade; while in China there are effective competitors increasingly available. (This is distinct of course from demographic or other dangerous rising Chinese financial risks.)

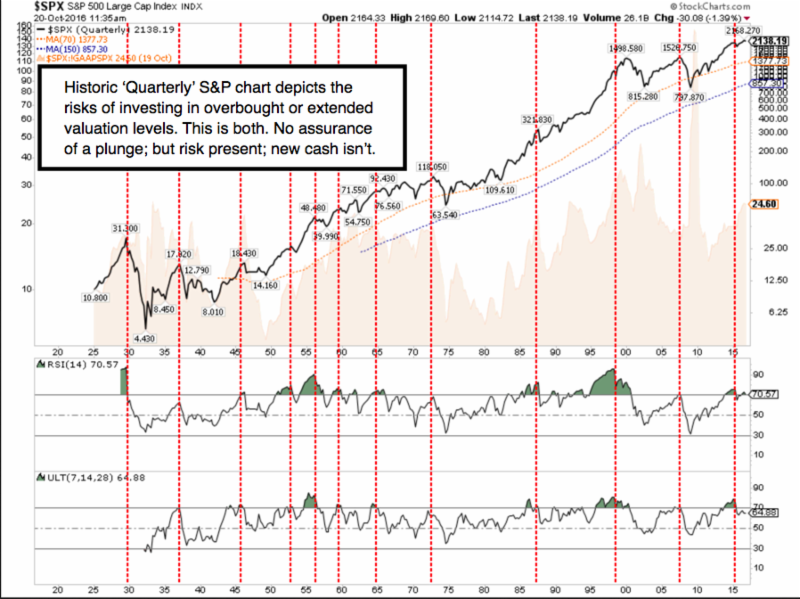

Two weeks ago Friday we did a short-sale guideline from Dec. S&P 2167, after the rebound from harvesting gains on a prior 2180 short. It is retained 'officially' with partial profits taken awhile back now; given an approach of almost always harvesting gains equivalent to what's risked and some profit; with the idea of having some 'skin in the game' for the downside post-Expiration risk; as this past week provided failing rallies to give speculators desiring to do so some spots to increase equivalent tactics (there are many surrogates to the S&P) or for investors overall to redeploy positions into a more defensive stand while building 'cash'.

We stay short, viewing this as a bearishly-biased risk-reward ratio. The market can crash too; though it's been slipping for some time, with strength in some techs, in some drugs, and in most Oils, masking what is otherwise a low-volume slog along a last-ditch technical support area that we have persistently noted oversees a potential downside vacuum

Monetary policy excesses set the stage for an alternative bubble in the mid 2000's; leading to our 'Epic Debacle' call in 2007-'08, prior to a bust, and based on our earlier view of the property bubble head toward disaster, and escalated once we learned of the CDS/derivatives mess (and how they were used improperly as 'net capital' by major firms) in 2007. What we have now also sets a stage for significant threat risks.

Daily action was extremely narrow on Expiration Friday; although on the surface it did have the general down-up-down flavor to it. We have discouraged excessive trading by scalpers during this time frame, while retaining 'skin-in-the-game' via the December S&P 2167 short-sale of a couple weeks back. That guideline remains for now.

Whether we get comparable effects isn't really debatable. We probably won't see that kind of outcome, because the Financial sector currently is well aware of that kind of prospect, and while leverage isn't unwound at least the capital structure has 'somewhat' been ameliorated. I say it that way, because the 'theoretical' risk is actually greater now than the 2007 situation; but you don't have the extended spillover risk for larger numbers of 'average' Americans, as you did back then.

However, my point is that we do have a 'bubble'; particularly in balance sheets of central banks; such as our Fed and the ECB. A sensitivity to this was evidenced by the markets favorable reaction to ECB's Draghi this morning spinning his QE and bond buying programs as seriously helpful; and then quietly responding to a question by nothing just briefly that "nothing lasts forever". You would think money managers assume that; but given the responses to such remarks over there and right here one has to believe many are along for the ride so long as the horse just bucks a bit, but doesn't throw them off.

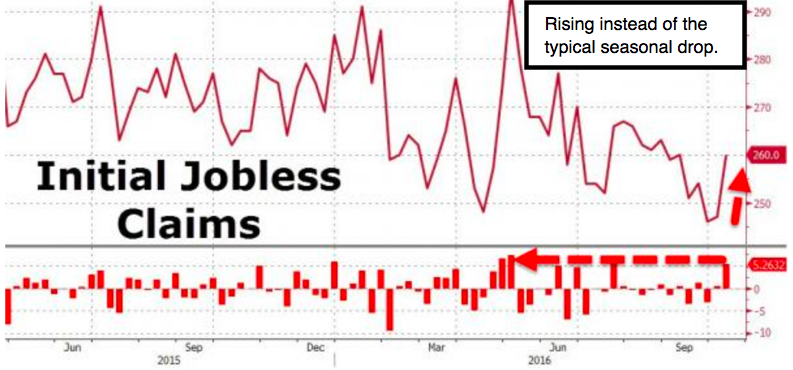

A buying panic ended long ago; with a somewhat agonizing period of jostling within a comparatively narrow range prevailing for awhile. At the same time fundamentals have backed our contention of economic slowing sufficient to perhaps be tracked as the start of renewed bouts of recession, from roughly mid-July forward of this year.

Concurrently you have the 'stuck' mode of Fed monetary policy; failure of most stocks to respond impressively on favorable earnings reports; complacency towards the deteriorating credit market conditions and a fairly benign response to international developments.

Hanging onto support becomes increasingly difficult for an S&P that is lacking in leadership; unable to get much going with rebounds or favorable responses to big-cap earnings (typically sold into) and really in an increasingly perilous posture relative to taking out recent lows.

Technically, I have highlighted the underlying 'vacuum' beneath the September lows (got very close again twice in the last few days); that in my humble opinion should not be a comforting picture for any money manager to look at, especially those that are locked in heavily long or not easily 'pliable' portfolios. Some can hedge; some rearrange, while a slew of others are complacently rationalizing, since they are stuck while unable to be as candid, perhaps as eye-opening Fed Vice Chairman's remarks yesterday would imply one should be.

Bottom line

There is lots of news with very little market movement, so far. We are past expiration and approaching (for most) the mutual fund fiscal year end. I discuss (though didn't follow-through my thought too well) the lack of 'heroic' tactics by most fund managers because they tend to try to 'peer match' rather than excel other money managers. It's different for hedge managers, who often have been candid about risk. I, in fact, am counting on the 'peer matching' crowd to provide significant portions of liquidations, should a market break trigger redemptions.

| (Minor errata: the Sat. main video was recorded in 5k High Resolution; so may buffer a bit longer for some internet connections. Please ignore the 'glitch' in video as well as know a casual reference to the first 'wireless' implementation of Apple CarPlay referred to the all new BMW 5 Series coming next Spring; not to a non-existent I-5 as I referenced it. Also in an effort to expedite this report, the discussion of AT&T / Time Warner is within the video.) |

Disclosure: None.