Market Briefing For Monday, Sept. 25

Accommodative monetary policies have delivered a market persistence basically of record duration, at price levels no higher than outlined likely for the past few weeks (S&P 2500 and then a bit more, but nothing significant).

The shakeout in Apple has been somewhat offset by strength in Oils, given that Apple represents almost a quarter of S&P capitalization these days. An issue remains Chinese market penetration and perhaps the lack of the new iPhone X to be compatible with T-Mobile's newer (better penetration) band both issues that are generally unknown by many investors.

Overall the market has ignored a degree of global turmoil and disasters, lots of which have varying impacts on more than financial capacity to respond. I point out that might even include the dam burst in Puerto Rico but perhaps not quite so glib if Hurricane Maria impacts the East Coast. At this point coastal residents are being warned.

I don't believe the market (despite Apple) is likely to crater quite yet but risk is rising in an overbought condition as we try to finish out the month and go into a presumably nervous October. It won't be 'Rocket Man' in North Korea or even the mixed aspects of monetary policy that has much impact but just an overdue correction that can rationalize almost anything as a catalyst after a shakeout gets underway.

Daily action expects some continuity of high-level stability into month-end, especially if Apple temporarily arrests its proclivity to decline for a day or so.

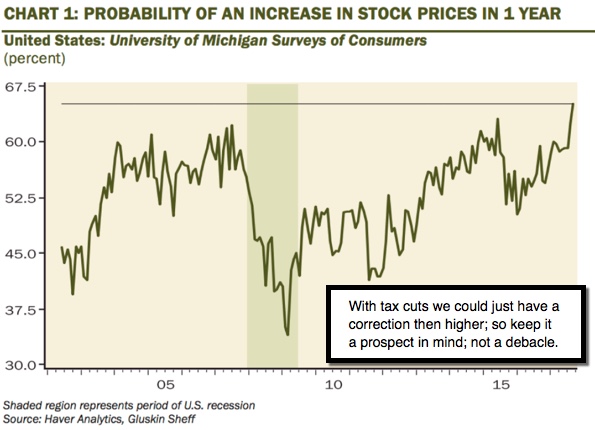

Overall we continue to be on guard for newly defensive market behavior and are by no means as complacent about the overall status as markets or the VIX might imply. We have however resisted short-selling the market given the belief that the market still holds out hope for tax cuts and more.

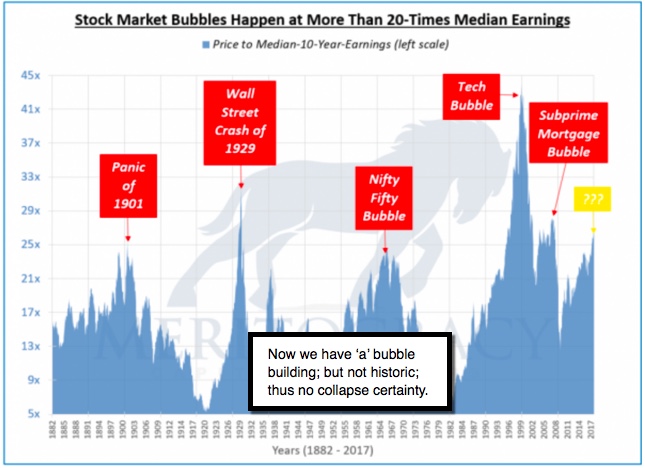

Regardless, the disconnect between market levels and economic activity is of course historic, as is the duration of the overall advance. We expected it to rally smartly if Trump won; we know all the pro-and-con arguments but simply felt the market would distinguish at least enough to mount the advance it did.

Now after considerable rotational corrections (from March forward) led to an additional thrust to S&P 2500 plus, we are overbought with risk building yet again. That's a focal point to keep in mind looking forward to October.

Weekend (final) MarketCast

Friday (midday) MarketCast

|

|

Disclosure: None.