|

'Stealth' de-risking of markets has dominated markets for months now in a rotation way. In a sense this has been healthy in holding markets up in this high-level trading range (generally, with Oils and others occasionally poking the indexes to new highs), while masking the gradual increased in sidelined monies, or rotation into 'perceived' less volatility sectors.

The supportive regulatory and now taxation policies have helped; and now it is pretty clear that market indexes can be moved by both Fed policy and the outcome of the present wrangling over sorting-out the nuances of a tax bill.

Odds favor that some bill will be passed; the particulars will matter to stock market behavior perhaps more than bond market action; because of what's coming (or not) with respect to 'when and whether phased-in' corporate tax rates are cut; and the same concern about capital repatriation provisions.

Such nuances will impact whether we get a pop-and-flop on the passage, or whether we get a mild pullback that allows a subsequent firming perhaps to year-end and even beyond. But that's for the Indexes. The internals have of course continued to be in rotating corrections essentially for several months.

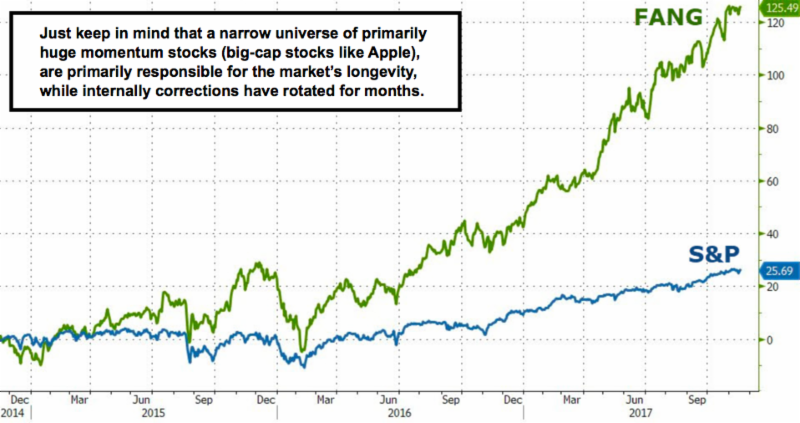

Only now do we hear 'experts' increasingly recognize the quiet correction ( almost a stealth bear) that has impacted fully one-third (or more) of the entire S&P 500. The massive under-performance of the Russell 2000 is also virtually unnoticed. Large-caps tend to do well in the 'late cycle', and I agree in a sense with respect to the narrow-leadership (concentrated universe that's working, like the FANG stocks represented for so long during this year that we forecast the S&P to move higher than anyone thought if Trump won; and he did and so did the S&P). But now that others recognize how this evolved it becomes troubling; and mostly because valuations are stretched and Fed policies are and will have impacts on liquidity as we move forward in 2018.

Now we don't deny that (barring war, pestilence or exogenous events); lots of technological progress lies ahead; including automation trends (sensors a big part of that) as we've speculated about. And we don't see intelligent jobs being replaced by productivity-enhancing robotics; but rather new industries and ways of employing humans evolving too (it better do so to avoid serious societal issues; as by the way it did around the turn of the last Century too).

We may have a trading week ahead that fluctuates based for the most part on speculation (about which there won't be a resolution) tax policy may be good or not so good for markets (there comes the FIFO issue I pointed-out regarding capital gains treatment, and nobody knows as yet if that's going to be part of the reconciliation efforts).

Meanwhile Oil, currency and other (more traditional) influences will highlight the semi-holiday week, during which the congressional recess postpones all other reckoning. As they return and begin infighting, we'll see if a tax bill arrives by Christmas, which is really essential or markets are in trouble for a different reason (failure to move on a key requirement of the Trump bump).

Companies have contingencies regarding how to deploy capital that clearly is dependent on whether we have new policies effective starting with 2018. I will say there is a 'small window' to let this debate slide into early 2018, but it won't help the markets ability to stabilize short-term should that be the case.

In sum

The big concern 'might' be if there is a tax bill passed; but they let the corporate rate either be deferred until 2019, or gradually phase it in. The market's overall reaction will certainly vary depending how that's handled in the final bill that goes for a vote. If everything initiates Jan. 1 of 2018 or is retroactive to Jan. 1 of 2018 'if' the debate slides into the first quarter; fine in terms of the economic outcome and expectations for earnings increases.

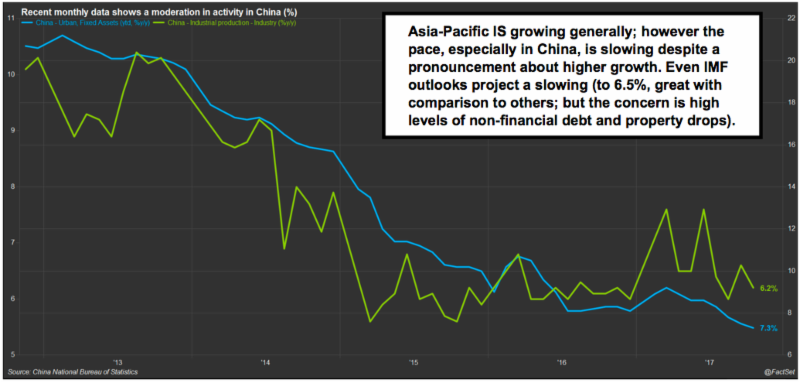

At the same time the S&P's behavior won't necessarily mimic what's good for corporate America. To wit: you can get a 'buy the rumor, sell the news' response; but how drastically the ensuing broad index drop will be relates to what the actual bill provisions are; aside of course other macro issues (like the Chinese debt issue; or for matter Oil prices relating to Middle East risk).

Conclusion

We anticipated Thursday would rebound rather than start out on a weak footing like earlier in the week. Friday was a consolidation day for at least the averages; while breadth was firmer in the broad market. Now to a degree the market awaits Congress returning from holiday recess; and it seems logical that they'll hammer out some sort of tax bill finally.

|