Market Briefing For Monday, June 25

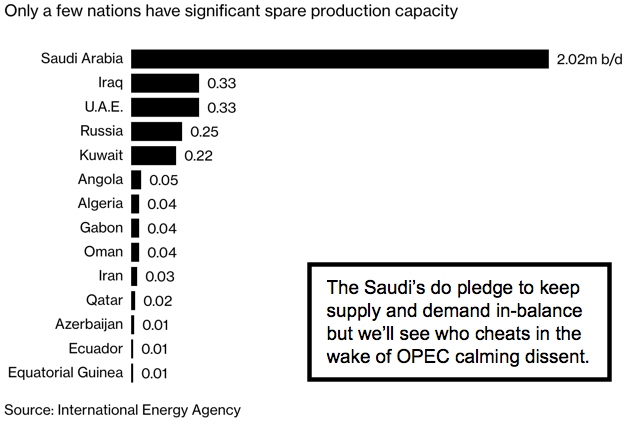

Pervasive 'data collection' really overshadows OPEC's limited move to increase production levels (constrained below their aspirations, much as I suggested would be the likely outcome from the Vienna conference). What OPEC really did was reduce the previously agreed production cutbacks and basically it was lower when 'guesstimated'; hence the Oil rally we had suspected would ensue. That definitely helped Friday's market rebound.

Those issues plus the President's latest 'tweet' threatening 'broad tariffs', of 20%, on ALL cars exported to the USA from the EU, swung markets on Friday; with our suspected Oil and Oil stock strength after OPEC, masking a lot of the otherwise-heavy (and rightfully jittery) markets. FANG stocks, for the most part, rebounded for prior slightly heavy selling on 'sales tax' news earlier; and then faded later in the day (only a short-squeeze).

Certainly there's was a tendency not to press the upside (absence of bids) into a political weekend too; as here you have Sunday's Turkish elections (probably rigged as best dictator Erdogan can), and continued turmoil that isn't really news in Italy; but nevertheless no incentive for traders to extend risks on such a Friday. (Erdogran ordered 'no' opposition candidates could be on TV or purchase advertising in the final week... how balanced.)

Overall we've felt rallies were interim anyway and that a sequence of lateral and then declining tops (more so in the DJIA than the S&P) were hinting at an inability to move equity prices forward for a couple weeks. In a sense a vast majority of stocks are barely changed for the year overall.

The 'data aggregation' issue itself threatens to emerge anew from Friday's Supreme Court decision, which superficially touches only on police crime suspicion warrant-less tracking of a cellphone but we think goes further at least in potential implication. The implications should be far wider and as I have mentioned before, there's now pushback on the Googles, Amazons and Facebooks of the world being so intrusive in tracking our lives.

For one, both AT&T and Verizon anticipated this earlier in the past week. I noted they were abandoning 'location tracking' in some ways and that's a big deal. I related it at the time to respecting privacy and not inundating a consumer with ads when they go into a mall or a store; or trying to lure for that matter, a customer to a different place of business.

Now with the SCOTUS decision; you have the 4th Amendment aspect just a bit clearer, though it was a 'narrow' 5-4 Decision by the Court. Actually a lot of citizens (outside of technology of course) believe it's late in coming; of course not to protect criminals (and by the way police can still use cell location data to pursue fleeing suspects or with a warrant) but to protect our privacy.

There is some chatter that this will now extend to our automobiles, which probably will be welcomed with respect to eventually not getting badgered by commercials while driving (remember almost all future vehicles will be essentially on-line most times as part of semi-autonomous driving systems and safety devices). Practically, this likely means when you use 'intended' services like entertainment or importantly 'Navigation'; you'll be tracked as you desire, but NOT be marketed to along the way. So I'd say it's a plus.

Bottom line, the near-term fundamentally now hinges on 'trade resolution' or alternatively what's being threatened, which is failure. A number of tariff impositions (such as with the UK) actually began on Friday. The biggest of all stories impacting the market is the SCOTUS decision on getting rid of a long-overdue removal of 'temporary targeted assistance'. Just like helping China and others recover decades ago, the internet sales tax 'holiday' sort of became permanent. That's why it's so hard to reverse these things.

In my view the 'sales tax' issue is allowing States to 'take charge' and say to online marketers that they have to stand on their own marketing, as the sales tax gradually return state-by-state; and that's going to eliminate what in essence has been a subsidy (by not collecting taxes) for many years. I know some are rationalizing Amazon's position; saying they collect tax while others don't. The reality is only 'partially'; and depends on the State.

So I think it's a buy-side hand-holding effort regarding AMZN and the like. I also believe tamping-down 'location-finding' and indirect marketing, will be a problem for others; such as Google and even Facebook. It's notable to see one company, that advocates 'for' privacy and does not use collection of data for targeted-marketing purposes, and that's Apple. If they'd revisit Siri's inherent limitations (accessing a broader database), perhaps even a sales spike would occur for their slightly languishing (but great audio for a single unit) HomePod, which prompts debates from audiophiles.

Technically the market isn't safe just because the S&P is above the 50 or 200 Day Moving Averages. I understand the argument to trade mostly the long-side, so long as those levels hold. But I also believed the S&P's last two week's actions have shown an 'inability' to advance above recent highs and I viewed that as a negative. Furthermore; many stocks can be notably off their highs or breaking patterns, before support points are neared.

Conclusion:

Discretion remains the better part of valor and even if we get a trade deal I suspect the market's favorable response would only be temporary. With a continued failure, and actual imposition of serious tariffs, this gets messy, with the breach of support points underlying the markets virtually a given. So we'd stay nimble with a bias toward fading rallies.

|

The market is 'heavy' and volatility squalls remain anticipated this summer as we've outlined. Oil generally led the 'Averages' back up, along with the short-squeeze we looked for. Remain wary and suspicious of upcoming as well as even 'trade-based' rallying, which may be tried next week. Weekend (final) MarketCast

|

Thanks for sharing