Market Briefing For Monday, February 27

Obsessive focus on 'Trumpism' beyond the economic prospects and of course tax plans that are still pending; now has the press doing more than dropping the context (as he alleges as we know, not always, often the case for some time); but focusing incessantly on this topic, avoiding others.

For instance, one of the concerns is what happens after a formal withdrawal of Brexit; fixed-income; margin calls on highly-levered traders (not just bond but equity markets); and of course the 'Black Swan' we've mentioned; odds of an ultimate deconstruction of the European Union.

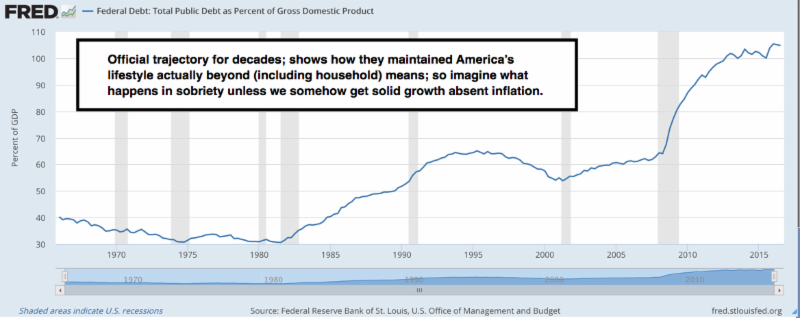

That contrasts with worries about whether the US can ever proportionately deal with rising debt service; if you look at Europe. Some countries there, at the moment, such as France, are soft defaulting (a term you won't hear for now; which really is what ultimate QE can turn into). For instance, the base rate in France is -0.26% last I checked; so essentially creditors are actually paying interest on the money that they are lending.

The seemingly obvious future scenario of escalating debt that can escalate faster than rising tax revenues (from an eventual revenue-neutral tax policy) is overlooked given the focus on social, immigrant and migrant issues. For that matter one might ponder whether the White House 'intentionally' shifts their focus so that there's not too much debate about paying for tax cuts and infrastructure, which really will encounter more opposition in Congress likely than anticipated; so could become an issue for the market in weeks ahead.

With near zero interest rates the Fed can still kick the can a long time. But a long time is not forever, as debt continues to spiral out of control, I suspect a period of rapid inflation will be needed to wipe it out, eventually. This also will help many heavily indebted folks, but it will be disruptive. Unlike many nations, the US borrows in its own currency, so inflation is a way of solving or rather deferring confronting debt when necessary. Doable but not good.

One reason this is not a huge 'present' problem is the nature of the creditor. If the crashing of a debtor economy would do more damage to the creditor nation than giving the debtor nation additional near-0% interest rate loans or interest forgiveness, or there are sociopolitical reasons to continue allowing debts without the expectation of repayment, a country could potentially keep going into debt way above this point. Japan's debt-to-GDP has been above 100% for decades now with no indication of decreasing and it has the fourth highest GDP PPP in the world. But 'they' have a 'trade surplus' we don't. At the same time, The United States is the third most interconnected economy in the world. A lot of countries have a huge vested interest in the stability of the US economy. Hence we can get away with this longer, than others.

These are all ongoing risks that are perhaps exacerbated by new policies as well as 'nationalistic' or 'populist' political trends within Europe; inspired only to a degree by trends in the USA or UK (we'll get blamed while much really is home-grown in countries like France, Germany and Holland, and actually predates the UK or US political shifts). Nevertheless, while I do not see this as an imminent concern (contrary to a couple credit guys who are worried it is upon us), I do see hints that things could become unglued.

When it's visible how things can become unglued, they often do not do so. I have pointed that out before; using Mexico and China as examples where a popular tendency in media is to suggest the worst (like trade wars), while it is a bias in the White House to simply say they'll make 'great deals' with us. What you'll likely get is what you see this week: rancor that results in meets; and then and period of time to digest the opposing views; then reconciliation of an adequate level to keep business going, and not rock boats too much.

This matters; because like a bank you might owe a billion dollars to versus a paltry million (just teasing in a way); at a certain level it becomes their issue, not just the borrower's. In this case it matters to both sides so extensively in this world, that in order not to 'crash' markets and economies, it requires the thought out process that seems to already be underway.

So ironically this is 'good news' that issues like a 'Border Adjustment Tax' or any other bilateral issues (aside from the major multilateral challenges) don't lend themselves to a simple solution. For instance, 'retailers' living or dying on every headline (negative or not) about the 'border tax', may be overriding for those stocks at the moment; when in reality the retail sector has been in a transitioning phase for several years. So the rallies in those stocks might very well tend to be temporary, as painful times will persist for many stocks in that sector, almost regardless of mixed responses to mixed tax signals.

Bottom line

Persisting upside regardless of European and/or credit market issues; and not because 'credit derivative spreads' are widening or not.

The way to justify these equity markets is just 'faith' that you'll have stronger growth a year forward; and eventually something concrete on healthcare, on tax plans, and on fiscal stimulus. The idea is not that the stock market does not care; but rather that the stock market envisions this with a passion; while ignoring some aspects of the credit market that suggests it's not 'for real'.

I have repeatedly pointed out that there is: proposal, enactment, and then a period of implementation; long before you'll get revenue and earnings higher in a way that (after-the-fact of this share price advance) validates the thrusts in equity prices.

That's exactly why we've pushed fundamental and even the technical 'facts' into the background, because unlike the previous two years (where you had most gains derived from Fed stimulus policy and corporate stock buybacks).

In sum

The market is stretched for sure; values are not bargains generally; and as I've said this is a huge 'faith-based' rally on expectations. Failure to deliver has big risks; which is why I've said they have to keep their eyes on the ball. The offbeat 'stuff' is primarily what the media has focused on, in what continues to be 'Trump-based' rallies based on economic policy. In my thinking there's no real reason for the market to be persistently bullish in these last four months than this 'realm', and that's what I anticipated before the vote, if Republicans got both the White House and Congress.

Now, this perspective also means the market will rise and/or fall overall on a focus on the economy as you can't justify current PE's (though there are a few more bullish arguments, but those too depend on policy carrythroughs).

Unless you believe we are actually going to get tax cuts, you'll set up some sort of (minimum one standard deviation, or correction) market setback, and if you do get them (such as almost immediately in terms of specific plans); it is conceivable to extend this with a truly awestruck blow-off upside spike.

It's not impossible we're in that now. The VIX was stable-to-firm even as we have had S&P rallies (warning that traders are paying up for protection); the liquidity levels are drying up, helped mostly by appreciation by what's on the books already; and there's no help coming from consumers overall aside from a nice jump in optimism. So if they're let down, the market will be let down.

It's also not inconceivable that if there's a delay in tax reform; the market at that point corrects.

Disclosure: None.