Market Briefing For Monday, August 7

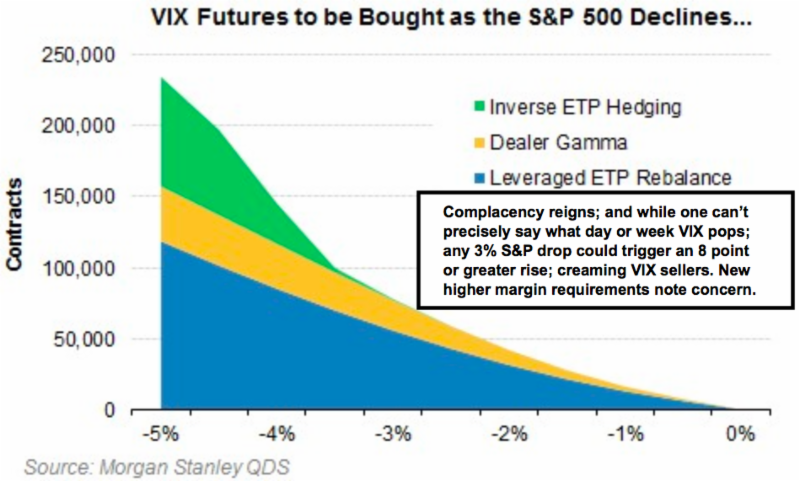

Irrational complacency has dominated the market for several weeks. It's an historical record as I recently noted. That's no assurance of an enormous bullish capitulation coming; much less an upward extension. But be wary.

While we've very studiously observed notably frantic (especially the bearish) perspectives coming from participants that are typically one-way (bullish) oriented towards the market; and actually have resisted temptations to short (fade) the market because we thought things could sort of stumble on in a rangebound way longer than their 'expirations' (for the most part they were playing Puts or bearish strategies that degrade significantly with time and in actuality evaporate into worthlessness); we're nevertheless more on guard going forward from here. There's even an internal reason for this concern.

That fact, that nobody wants to contemplate: higher margin requirements on volatility products, not speaking about just the VIX, but generally the ETF's. Now that's because volatility is a 'fulcrum' of today's reflexive market nature.

In that respect it's generally ridiculous to hear debates as to whether having a surge in volatility sends stocks lower, or whether market declines (much less a crash) could lead to a volatility surge. There is a more basic concern I am driving at (or postulating since nobody knows 'yet'), that that is simply a potential (again emphasis on the word 'potential' not assured) response by a market 'if' it finally moves off dead-center, when it contemplates the reality of volatility-linked leverage about to be cut.

Higher margin requirements first by one, then by more, if not all, the dealers and/or exchanges, would be a significant 'potential' catalyst forthcoming. As the first move (by Interactive Brokers) takes place 'after' Expiration August 19 (yes, a Saturday for settlement of trades ending the prior Friday which is the 3rd in August), we presume others will take notice. Since they've stated their intent (generally unreported but perhaps very significant to players not only interested in volatility, but the market in general), others will take note.

Bottom line

You know my overall views about North Korea (censored this Saturday at the United Nations Security Council again); and about politics in DC (where a divisive political situation must move toward the center before it alone becomes a 'black swan' impacting the Nation's future), we focus this report on an internal market factor coming-up in the next couple weeks that indeed could be the 'catalyst' (or one of them) that won't break a market just itself, but will matter when (presumably not 'if') a suspected correction gets going in August and/or September.

In sum

This is more technical and internal than some discussions; however it does not mean that an actual catalyst can't come from domestic politics or a geopolitical development. It means that the leverage changes will impede the ability of the institutions and one-way oriented bulls to hold this together.

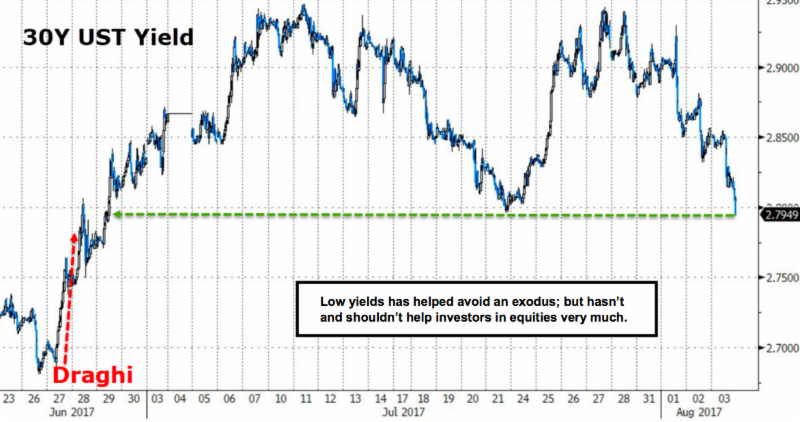

Overall: while some call markets 'exuberant'; it's actually been anything but...unless one has been referring to the Euro rally or near-low record interest rates yet again. Keeping in mind the contribution credit markets are making to suppressing asset-class shifting, or the knowledge that reflects sluggish, not robust, economic activity; one has to ponder what happens when a new meaningful bounce in rates occurs, whether central bank induced or not. At this point in time I note these areas but suspect it's not 'the' crucial issue.

|

Disclosure: None.