Market Briefing For Monday, August 28

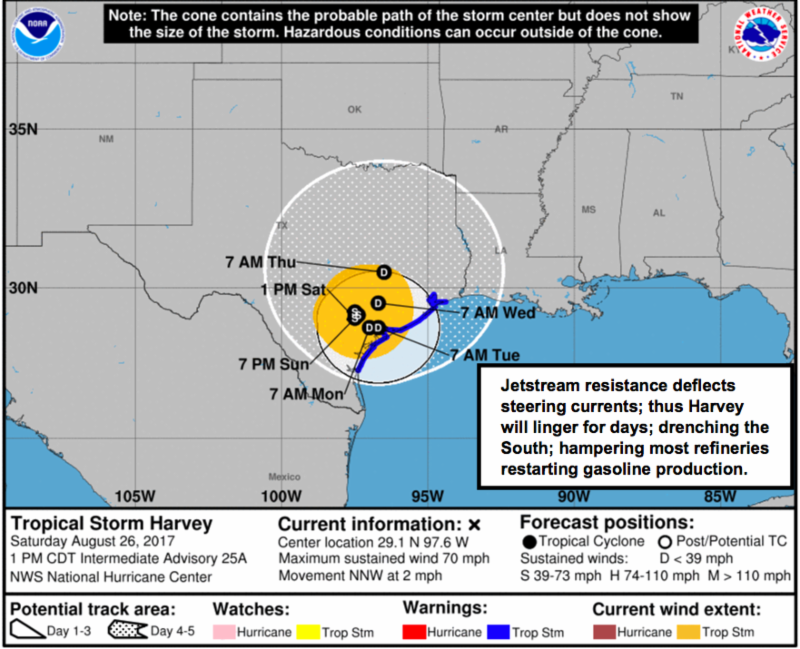

The market-related factors of Hurricane Harvey are impossible to estimate but construction and rebuilding will be major projects in the area for at least several years ahead. Fortunately the 'eye' of Harvey missed densely-populated cities, while much like its namesake (Harvey the Rabbit); the storm is bouncing around in such an odd manner, that NOAA radar has tracks taking it in every direction. That means it's oscillating and lingering basically and remains a flood threat for some days to come. Most of the damage will be from water, not wind as you know and that's where the long-term rebuilding aspects will occur.

More immediate will be concern for gasoline supplies. Texas and Louisiana are the bulk of the normal domestic refining capacity; and the duration of their full or partial shutdowns will determine not just prices but whether all the presumptions about the crack spread misses the economic point.

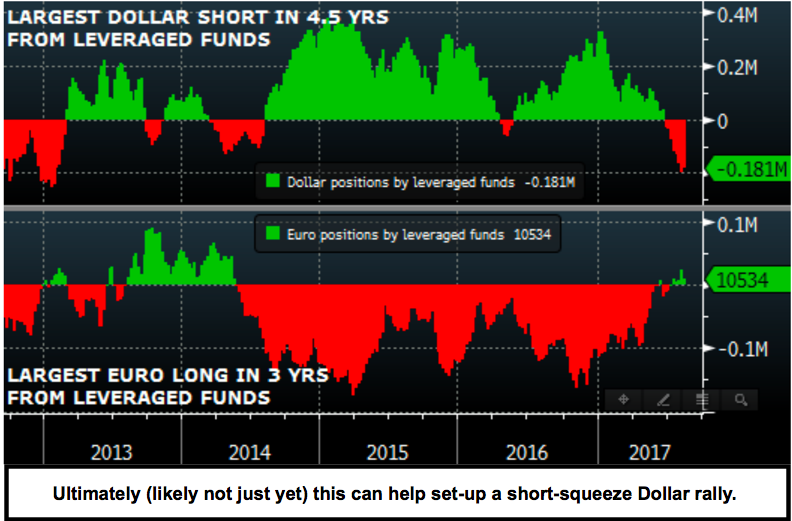

In sum, nothing has changed with respect to market patterns beyond that I have outlined for the S&P, and the overall market, in recent days. I explore the Fed remarks and ECB's Draghi comments a bit in the main video.

|

Daily action remains almost as erratic as the Hurricane's path; jumping around like a rabbit; but certainly not consuming everything in its path like Harvey continues doing. Nevertheless a fair number of stocks have sort of been 'rabbit food' for weeks or months; which is why so many are below not just their 100 Day Moving Averages; but often the 200 Day. Friday was very interesting not only as we had the relative non-event of the Yellen comments; but the widely-ignored (and market shaking) Draghi talk that hit during New York's final hour. That may impact Monday a bit. Yes, all the talk since has been about the actions the President took (clever timing) later Friday but those moves really aren't market impacting at all. In the market, sustainable rallies are unlikely to show up; and this imperfect range of the S&P may persist just a bit longer; but we suggest avoiding any tendency for complacency, as it can bust open really at any time.

That's why the uncommon projections for distribution under-cover of a firm DJIA and S&P; allowing the averages unsustainable rebounds sometimes to even higher levels, while many stocks simply tested previous peaks or sort of had (regression rebound) bounces. |

Disclosure: None.