Market Briefing For Friday, September 30, 2016

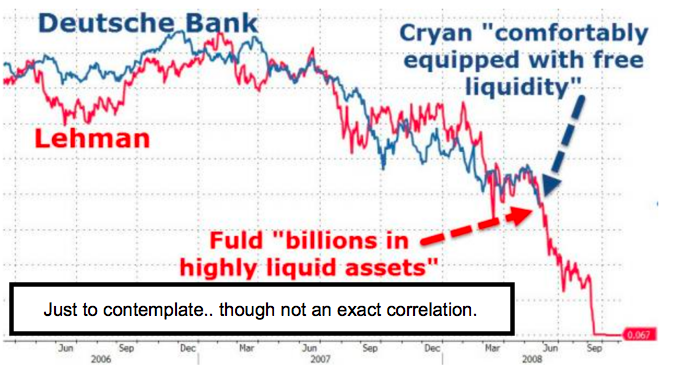

Thin 'capital cushions' are not new although they seemingly surprise lots of analysts and hedge fund managers. Many 'must' pull money out of Deutsche Bank and even related financials (because as I've noted all week Deutsche Bank was the lead syndicator of lots of funding efforts in Eastern Europe and the former East Germany), which gave them a noble but riskier loan portfolio well before the recent U.S. 'fine' or other new worries 'as if' this hadn't been brewing for several years as we periodically noted.

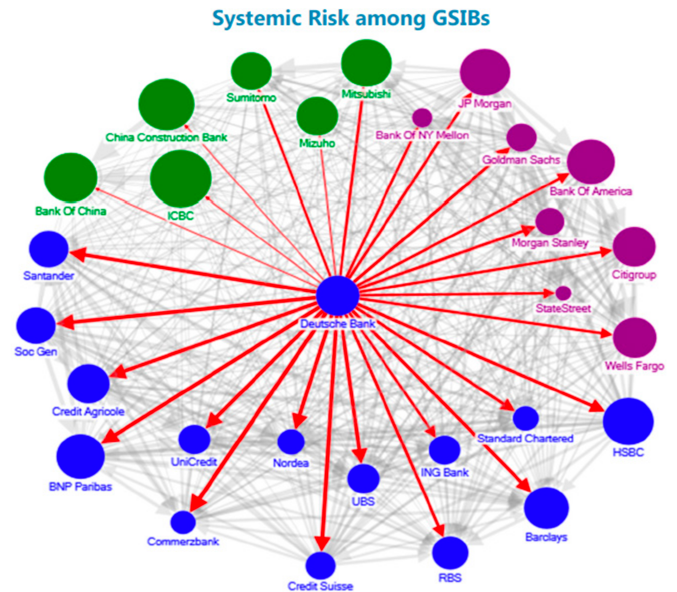

Deutsche Bank holds the world's largest derivatives portfolio; that's the risk. Note most major global banks are involved (to lesser degrees) with their lead. This (like other bank issues) is not news; though the world seemingly figures it all out only now. I've warned of the lack of unwound derivatives for years now.

It's a big bank that's been massively leveraged for years; with the largest derivatives book in the world. While Chancellor Merkel 'said' they won't bail it out; ultimately the managers may press the situation until there's question about their long-term secure paper, at which point the 'bet' would be that Berlin blinks, similarly to the U.S. moves in 2007-2008. A move that inches towards a 'bail-in' increases the dilemma facing a beleaguered Berlin and Deutsche Bank. The U.S. 'fine' is almost irrelevant for now; it did however provide (a service?) by highlighting the leveraged and systemic issues, as analysts finally started looking at it anew. Why hedge guys stayed aboard shares for far too long since we've warned about this for at least two years; I have no idea.

Now, I discussed this last week and this week; and long ago noted the overwhelming derivatives and loan-portfolio issues with Deutsche Bank relative to others; but not the palliative the analysts and pundits are trying to make it out to be. There is one thing not predictable in terms of time, but in a sense it's a probability: that's the intervention by Berlin (a bail-in essentially) to stem the tide.

For Germany it's sort of a too-big-to-fail situation. In the U.S., Wells Fargo (also discussed below) is shocking given its history and prominence. But presuming cross-selling wasn't as egregious at other banks, the Feds might not be reluctant to seriously pursue punishment (one of course can look back and suggest that too many missed prosecution or even heavy persecution resulting from the inappropriate derivatives holdings as net capital back in 2007, which is why we forewarned of an 'Epic Debacle' coming then). And while I don't need to suggest I'm concerned; I will say most of that paper can't be unwound, because if you 'mark to the market', one finds there's not much of a market. Perhaps a reason we don't hear Congressmen or bank analysts being candid about the topic.

Oil's well that ends well

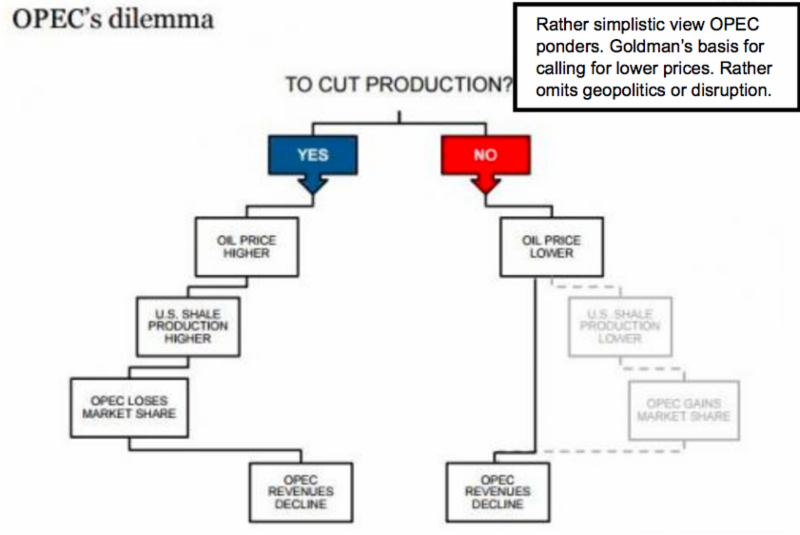

Or so the Bulls think given a 'qualified' delayed production cut deal hit the newswires, breaking from Algiers. There is a catch (even if the final communique fails to note it); by which certain 'exempt' countries can exceed the new lower quotas where limits had constrained production for certain reasons). Among those are Nigeria and Libya as of course might be expected, but also Iran, which could make this a non-starter. l

Since the 'limitations' aren't set to kick-in for over a month; there's time for markets (and oil trading desks) to play with the price of Brent and WTI several times, along with post-OPEC-meeting rumors and speculation that will enhance oil's volatility. At the same time all this fit perfectly with my remarks a day ago for a rebound in Crude; knowing that the heavy-lifting (if any) of this week's intraweek rally really depended on oil, certainly not Financials, triggering the move.

The idea of the cutback being for just a month (funny how that detail was left out of news reports or mentioned in sort of hushed tones) pending re-evaluation by OPEC members, suggests they want to get the price up shorter term (fine by me; it's what I called for after the recent shakeout), and then increase production again next year.

I suspect (regardless what they do down the road) that's a message designed mostly to 'deter' revival of America and Canada's oil industries, which have been badly hurt by the oil war's latest incarnation. Washington won't be upset, as they don't desire a focus on petroleum, so quietly mostly welcome OPEC's approach causing hesitation, as far as expanding shale activities, or bringing pricey-risk taken-out of service back.

There is also talk of OPEC requiring 'support' from non-OPEC members; and that's a non-starter too; as neither Russia nor the United States are likely to comply with that. Anything's possible but note they won't even finalize the 'Plan' until November; which we suspect takes the edge off the short-covering spree that took place on Thursday. Besides the short-covering this provoked (along with taking us flat the balance of any S&P activity); we should be mindful of upcoming end-of-month and quarter activity.

In sum

The idea was ideally for the intraweek rally (although choppy and irresolute) to last until perhaps Thursday. And we believed oil had to lead any upside. We were hoping oil would rally; rather clearly yesterday indicating the prior drop was past, not starting (to wit our alternative moves first expecting 50; then looking for a pullback as we got; but declaring it was done yesterday). We viewed Goldman's warning of lower price ahead, in fact was after-the-event; not anticipating. So I leaned opposite calling for a lift. Now we have that but watch it be tempered by the actual OPEC 'specifics'.

Daily action

The correlation (of oil and banking) with the S&P chart pattern (failure to make new highs) may not be causation; however there is little doubt that the market is being knocked on its tail by precisely the market's failure in the midst of an oil rally that obscured behind-the-scenes selling on light volume rebounds.

Disclosure: None.