|

The 'trap door' was sprung immediately after pre-opening futures shifted from up to down, continuing the alternating series of reversals seen this week. It recovered some after President Trump focused on 'Energy Dominance'; just the term I hoped he'd use to describe a key part of America's recovery effort.

S&P is exacerbated by thin pre-holiday activity, although there is an emphasis on what central banks are saying; what the implications of policies are; and on the negative aspect of new buybacks, which suggest not just sensitivity to rates (hardly, and might do better if they were higher); but various central bank heads misinterpreting or spinning recent Fed-head remarks.

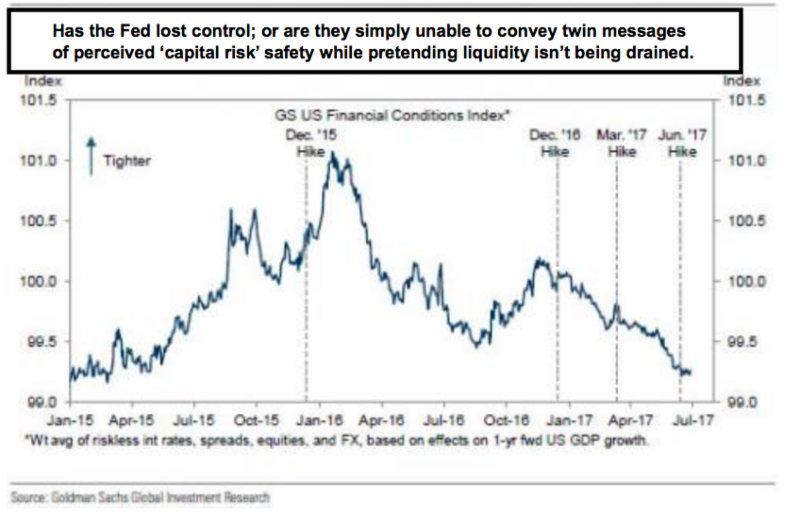

For instance, I suspect St. Louis Fed President Bullard's remark suggesting the 'Fed has lost control' was a contributing factor to midsession washout, of course triggering some intraday short-covering after that. My own view has not embraced the view that Yellen's statement was intended to 'really' mean there won't be a financial crisis in her lifetime (if she means it; delusional is a knee-jerk response). I suspect it was 'meant' to suggest a pathway exists for both public and private sector 'capital investment' rather than the further sequestering of funds, which (for instance) buybacks are symptomatic of.

Nevertheless, I have embraced 'Don't Fight The Fed' during this. However 'rates' are not going to firm at such a pace that it inhibits business, perhaps it does the opposite. But business growth has already been 'discounted' by a robust forecast market advance from Election Day last year to the internal market high we identified in early March; leading to a subsequent S&P high more or less at the 2450 area.

The more recent struggle between 2430-40 (that's now resistance as usual after an established trading-range breaks down), was actually distribution in many sectors (such as the FANG stocks) on rebounds from prior slides. Of course one had to allow for quarter-end stabilization; or that tendency being used to sell into, in a belated process to build cash for future positioning.

In sum, I've believed that the market was under distribution from March and emphasized selling of rallies persistently and rotationally (as far as sectors) ever since. That's why there was the combined belief about how portfolio managers were rearranging the deck chairs, so to speak; allowing the S&P to generally mask the distribution throughout this 2nd Quarter.

While most pundits are debating what's going on or when the market really cracks (some even think soars, but there's been no basis for that lately. It's just efforts to pop; most of which flopped; as nothing has been sustainable).

The reality is most of the stocks that did the 'heavy lifting' earlier in the heart of our projected move from Trump's win forward, was done from November through January, by the FANG stocks and a small handful that impacted the averages. With realistic investments in big stocks not warranted for months now, they broadened-out buy-side interest into relatively mundane stocks, in an effort to obscure the distribution while some pandered to public buying in the latter stages of the move. We argued against chasing strength.

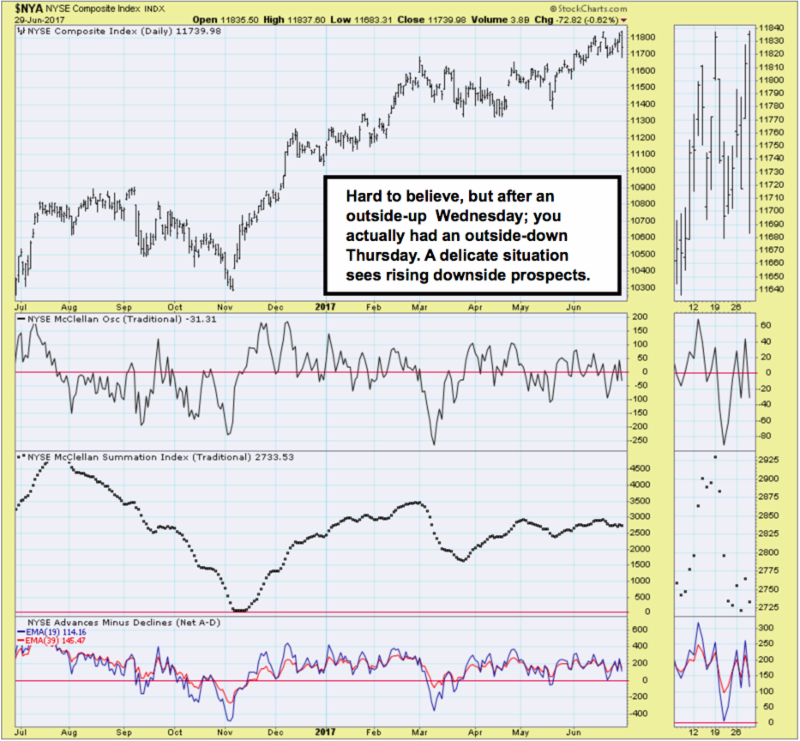

Daily action for sure was extraordinary. It doesn't matter that we didn't get a pop-and-flop (though it was seen if you include pre-opening action led by the banks of course); all the action of the quarter now ending has been 'sell the rallies' rather than 'buy the dips'; because it's all a huge distribution.

Whether this stabilizes more or not on Friday, the last day of the quarter, is really academic. That's why I described, 'at best', a period of stability into the early parts of July after which (barring some real good economic news) a further slide into negative territory for the major indexes should be logical.

Throughout the 'heavy lifting' period we were bullish (still will conceivably be 'after' adequate corrective action, which will vary depending on events) and throughout the FANG distribution we've described it as masked selling, not a re-accumulation for new rallies. It has been painstakingly long but history tells us that sometimes the heaviest declines follow a prolonged distribution.

I know there are arguments about how much cash is floating around and will prevent decline... even the Fed sounds that way at face-value. Nope;,it won't avoid it. Actually, so much money moved into equities that a gargantuan shift isn't out of the question. It won't be just because of rates either. However, it doesn't matter too much as the time for selling rallies began in March, surely not only now. But the majority of money managers are heavily long, so you'll get serious liquidations (today was actually not much relatively speaking) in the intermediate future.

We'll try our best to navigate these but the guidelines for buying a Trump win; then stopping buying in the first quarter and start selling in the early part of the second quarter; and all rallies thereafter to build buying power.. well that's been the strategy. So we'll enjoy watching the crowd jockey and fight about every little swing. Again while we try to call them, the point still is that there's far more downside risk than upside potential.

Ultimately, today was a preview of coming attractions.

2 o'clock balloon (intraday) MarketCast

|