Lots More Than Aspirin: What You Should Know About Bayer

Bayer (BAYRY) is a conglomerate combining various businesses under one umbrella. If its acquisition of Monsanto (MON) were to close, its seed business would become a very important component. It has a large medical device business and a major pharma business and a large animal health business. It also owns a major equity stake in Covestro which it reduced yesterday by 10%. The equity stake went from ~40% to ~30% percent. Bayer got $1.4 billion in return. Which values the remaining stake at $4.2 billion.

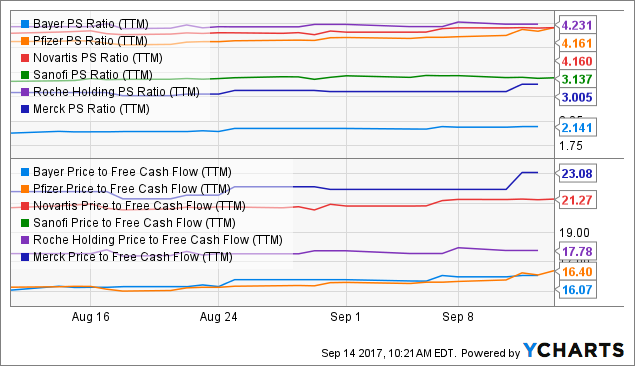

The conglomerate is attractive because it is not very expensive at 16x free cash flow, 15x EV/EBIT and 2.14x. If we took out the Covestro stake it would look even more attractive.

Bayer is paying a steep premium for Monsanto and if the market doesn’t rerate Bayer afterward it is going to be a value destructive transaction. There is however a good chance it will not happen as the EU launched a thorough investigation.

The conglomerate is mostly like a pharma but it trades at a large discount to big pharma peers. I’ve taken these two metrics but it’s also true for enterprise value metrics.

It acquired Monsanto at a huge premium to these multiples. The EU is looking at it closely which means its existing seed business is a strong complement or even highly comparable. Meaning that by treating Bayer as a pharma we aren’t doing it a huge favor.

Bayer doesn’t even have a bad pharma portfolio either. Many of its competitors struggle with patent portfolios that are getting long in the tooth. With many of the big diseases covered and the cures that were easier to find all picked off, pharma is facing the problem it needs to invest ever more money to treat smaller patient groups.

Bayer’s biggest sellers are Xarelto and Eylea. These have quite a bit of life left which positions Bayer favorably. A problem for Bayer is that it gets a lot of bad press on the widely prescribed Xarelto in addition to litigation costs dealing with the scourge of the class action lawsuit.

Xarelto is a Warfarin substitute, which was first introduced in 1948 as a rat poison. It is very easy to make a mistake dosing Warfarin which can kill and an overdose isn’t easy to detect early because internal bleeding can occur in the brain. With Xarelto dosing is much easier, resulting in less mistakes. But Xarelto can be deadly as well and unfortunately, it does not have an antidote which Warfarin does.

Bayer also owns big OTC pharma brands which are generally very attractive. Well known examples are Alka Seltzer, A+D, Aspirin and Aleve.

Source: Bayercare

Conclusion

The market is generally trading at highly elevated multiples. I’m interested in defensive and cheap businesses that are found off the beaten path. Bayer is one that piqued my interest. They don’t always get the best press and if they do get Monsanto that will not improve matters. However, hated stocks sometimes offer the opportunity to buy secure cash flows at the lowest of multiples. Bayer trades at what appears to be an indefensible discount to peers while both its seed and pharma business are defensive in nature. Something I value highly in the current environment.

Disclosure: no positions in any stock mentioned