Hochschild Mining - Looks Interesting Now

Hochschild Mining (HCHDF) is a mid-tier silver/gold producer operating in South America (Peru and Argentina). The company has been under my radar for years but most recently my interest in this miner has dissipated a little bit. Why? Because Hochschild was one of a few mining companies that hedged their production against lower precious metals prices. What is more, this policy had a negative impact on the company's results. However, in the 1H 2017 report I have found this statement (page 23):

"In 2016, the realized loss on gold and silver swaps and zero cost collar forward sales contracts in the period recognized within revenue was US$3,116,000 (loss on gold: US$3,501,000, gain on silver: US$385,000). There were no forward contracts in the 2017 period"

The most important is the last part of it (bolded) - it looks like Hochschild does not hedge its production any longer (if somebody claims the opposite - please, let me know; maybe I overlooked something... ).

One issue has gone but 1H 2017 results were very disappointing and since middle August 2017 the company shares have been in their strong downward trend:

(Click on image to enlarge)

source: Stockcharts.com

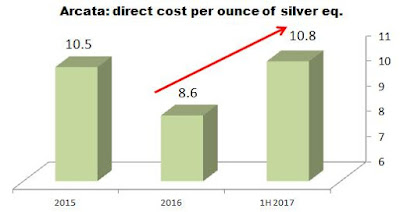

What happened? The first problem is called "Arcata" - now this mine is one of the highest-cost producers for Hochschild:

(Click on image to enlarge)

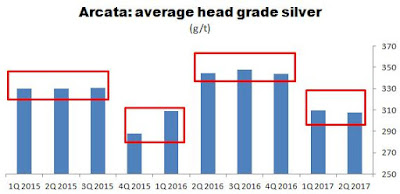

In 1H 2017 the direct cash cost of production went up by 25.%, compared to 2016 and head grades went significantly down:

(Click on image to enlarge)

Well, the chart shows Arcata's mining sequences (red blocks) and now it looks like the mine has entered another sequence - this time the company is mining in the low-grade zone. Hence, poor results.

Unfortunately, Hochschild does not disclose where it is going to mine silver / gold in the future. The company's comment is quite enigmatic:

"At Arcata, first half, production was 2.9 million silver equivalent ounces (H1 2016: 3.7 million ounces) with tonnage and silver grades adjusted following a revision of the mine plan to accommodate a reduced number of stopes and narrower veins. The focus at Arcata is to improve its cost position by increasing the quality of resources through the brownfield exploration programme as well as other efficiency and productivity measures in order to ensure the long term sustainability of the mine. The forecasts for Arcata’s output for the year have been revised to 5.5 million silver equivalent ounces in 2017"

And another piece:

"In H1 2017, as expected, Arcata’s all-in sustaining cost rose substantially versus H1 2016 to $17.6 per silver equivalent ounce (H1 2016: $13.0 per ounce) reflecting the reduced tonnage and grades resulting from the revised mine plan as well as the previously-announced increased investment in the mine’s brownfield exploration program"

Well, it looks like there is a problem: narrow veins (and probably higher dilution) and higher capital spending (brownfield exploration). In other words, despite the fact that Arcata has been a long-life operation (mining started in 1964), now it is facing troubles...

Another problem: the San Jose mine (shared with Mc Ewen Mining) located in Argentina. This mine, similarly to Arcata, substantially increased the direct cost of production (from $7.6 per ounce of silver equivalent in 1H 2016 to $9.1 per ounce in 1H 2017).

To be honest, it is not easy to explain this increase - head grades and the tonnage processed look alright (grades were even higher than in 1H 2016) so...

The company explains in this way:

"At San Jose, all-in sustaining costs increased to $14.4 per silver equivalent ounce (H1 2016: $11.7 per ounce) mainly due to the elimination of the Patagonian port rebate in the fourth quarter of 2016. In addition, lower than expected currency devaluation in Argentina only partially offset ongoing unit cost inflation. Overall 2017 all-in sustaining costs are now expected to be between $13.5 to $14.0 per silver equivalent ounce"

I am not able to comment on the Patagonian port rebate but as for inflation...yes, it can be a problem. Now the inflation rate in Argentina stands at 23.1% but in 1H 2017 the Peso was just 9.6% weaker against the US dollar, compared to 1H 2016. So inflation could be an explanation...

Of course there are positives - Pallancata, another Peruvian mine, was converted into an excellent operation (direct cost of production of $5.9 per ounce of silver eq.!) and the last mine, Inmaculada, keeps going smoothly.

However, 1H 2017 results were a negative surprise. For example:

- cash flow operations (excluding working capital issues and taxes) went down from $152M in 1H 2016 to $111M in 1H 2017

- free cash flow dropped from $89M to $29M

Hence, investors panicked and threw in the towel. As a result, now Hochschild shares are trading at quite depressed levels (EV / EBITDA of 6.1).

In my opinion, it is time to get interested in Hochschild once again...

Disclaimer: This article is not an investment advice. I am not a registered investment advisor. Under no circumstances should any content from here be used or interpreted as a recommendation for ...

more