Gilead Is Sending A Sell Signal Ahead Of Its Earnings Report

Photo Credit: Jamie

Gilead Sciences, Inc. (GILD) Healthcare - Biotechnology | Reports November 1, After Market Closes.

Key Takeaway

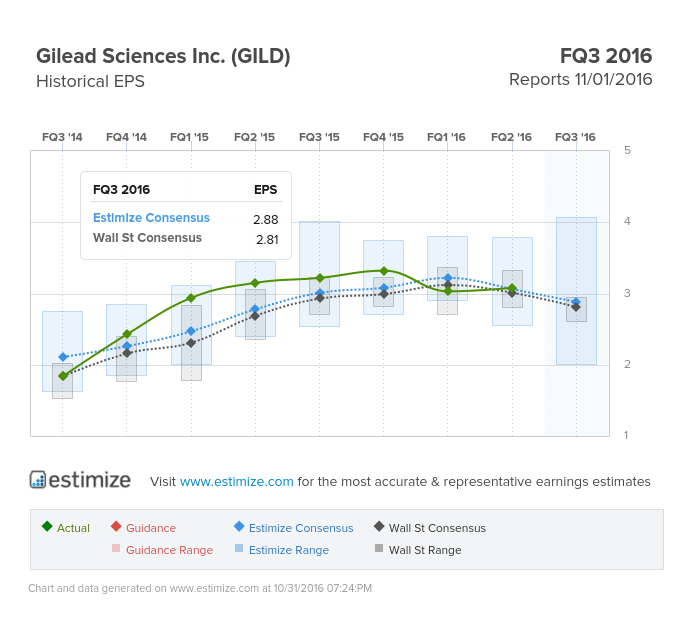

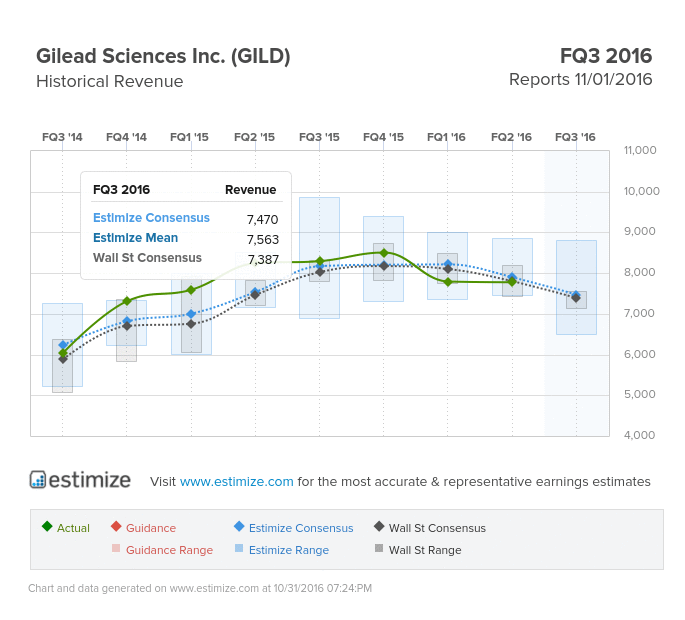

- The Estimize consensus is calling for earnings per share of $2.88 on $7.47 billion in revenue, 7 cents higher than Wall Street on the bottom and almost $100 million on the top

- GIlead has faced setbacks in recent quarters due to weaker sales from its key Hepatitis C franchise

- Gilead’s robust pipeline bodes well moving forward but don’t expect them to turn the corner this quarter

- What are you expecting for GILD?

Gilead Sciences has turned a fruitful 2015 into a troublesome 2016 after a string of weaker than expected earnings reports. Shares are down 27% year to date as investors jump ship to better performing companies. A large portion of this draw-down has been driven by weaker sales of its flagship Hep C products; Harvoni, Sovaldi and the recently launched Epculsa. Its widely expected that this trend will take its tolls on third quarter results. In fact, analysts are taking down estimates feverishly leading into the report.

Analysts surveyed by Estimize are calling for earnings per share of $2.88, 9% lower than the same period last year. That estimate has been revised down nearly 10% since Gilead’s most recent report at the end of July. Revenue for the period is forecasted to fall 9% as well, to $7.47 billion, marking a second consecutive quarter of negative growth. Historically this was a name that consistently topped expectations but those days are behind the drugmaker with all signs pointing to a miss tomorrow.

Gilead’s rise and now fall have come at the hands of its hepatitis C franchise, which includes Harvoni, Sovaldi and the recently launched Epclusa. The treatments were primarily credited with its double digit gains in 2014-15 and are now being blamed for negative growth in fiscal 2016. In the second quarter, the group of drugs recorded a 18.5% decline primarily due to lower sales of Harvoni. Harvoni sales were down a resounding 29% as new competition, mainly from Merck, seize its market share. Weak performance from the Hep C franchise was not only disappointing in the U.S. but Europe as well.

This sharp downturn caused management to cuts its outlook for the year in the range of $29.5 to $30.5 billion from $30-31 billion. Nevertheless some of these losses should be somewhat offset by its growing HIV business, which includes a handful of already established treatments. Also, a robust pipeline positions Gilead for an easy bounce back in the near future. Setbacks from HCV will nonetheless be the primary talking point from this quarterly report.

Disclosure: Each week, Forcerank runs a variety of games covering different industries. What we have found, is that the highest ranked companies in their ...

more