Cabot Oil And Gas: Buy The Weakness

Cabot Oil & Gas (COG) is a stock we have been covering for quite some time. Recently, the company posted its Q4 results, which was impacted heavily by movements in gas and oil prices. In this column, movements in the price of natural gas and oil, the performance of the company in Q4 and for year 2017, and offer our projections for 2018.

Movement in natural gas and oil prices

Take a look at the movement at oil and natural gas prices, respectively, for 2017:

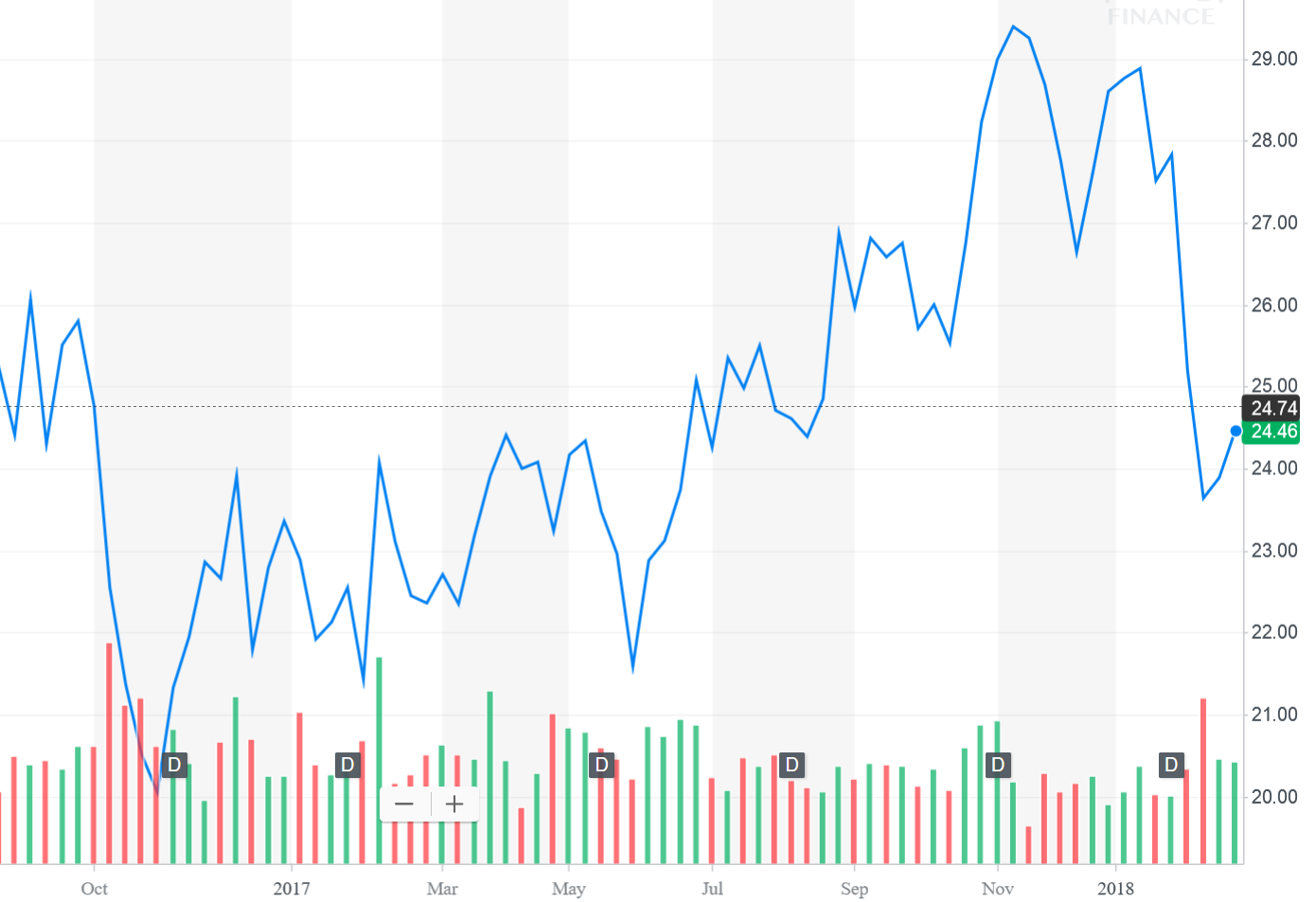

Oil price in the last 18 months

Source: NASDAQ

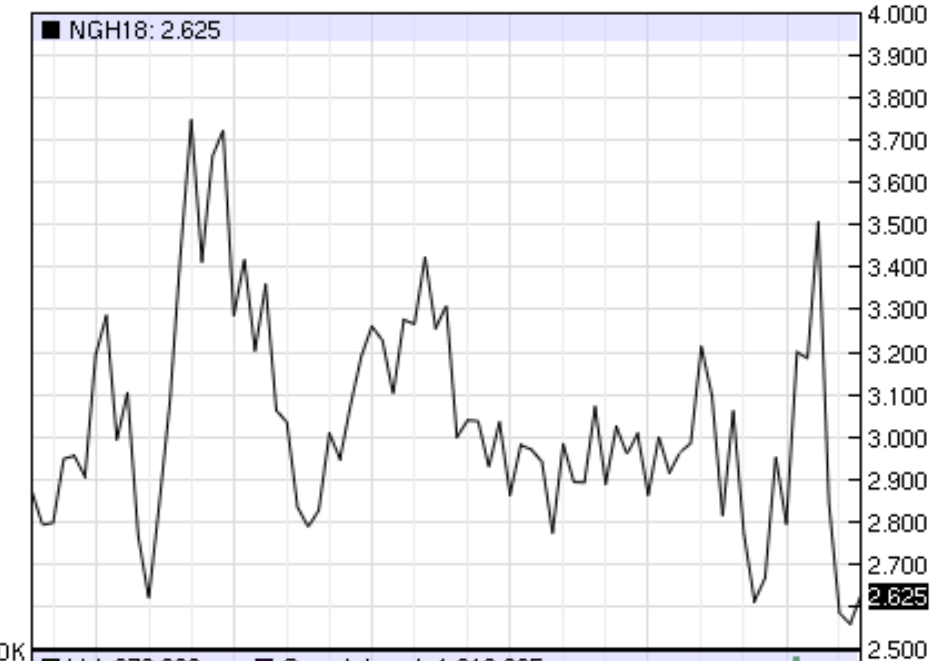

Natural gas-

As you can see, the volatility in the prices of these commodities had moved the stock as well in 2017:

Source: Yahoo Finance

As you can see there is a correlation in the share price movement and that of oil and natural gas. Keep the movement in oil and gas prices in mind as we discuss performance of the company.

Q4 2017 performance

Let us first start with performance in Q4. Production matters. Fourth-quarter 2017 equivalent production was 172.6 billion cubic feet equivalents or Bcfe, consisting of 164.4 billion cubic feet (Bcf) of natural gas, 1,238.0 thousand barrels (Mbbls) of crude oil and condensate, and 131.5 Mbbls of natural gas liquids (NGLs). Cabot's equivalent production increased four percent sequentially compared to the third-quarter. Natural gas production however disappointed us. It came in at the lower end of our expectations because of delayed in-service dates for two new third-party compressor stations. This less than expected production weighed slightly on our expectations for earnings, although price realizations were strong.

Fourth-quarter 2017 natural gas price realizations, including the impact of derivatives, were $2.18 per Mcf, a 12 percent improvement compared to the prior-year period. Excluding the impact of derivatives, fourth-quarter 2017 natural gas price realizations were $2.15 per Mcf, representing a $0.78 discount to NYMEX settlement prices. Fourth-quarter 2017 oil price realizations, including the impact of derivatives, were $54.54 per Bbl, an increase of 27 percent compared to the prior-year period. NGL price realizations were $23.51 per Bbl, an increase of 70 percent compared to the prior-year period. Fourth-quarter 2017 operating expenses (including financing) decreased to $2.01 per Mcfe, a two percent improvement compared to the prior-year period. This led to a strong financial result when combined with production.

Fourth-quarter 2017 net loss was $44.4 million, or $0.10 per share, compared to net loss of $292.8 million, or $0.63 per share, in the prior-year period. Fourth-quarter 2017 adjusted net income was $59.5 million, or $0.13 per share, rising quite nicely compared to adjusted net income of $5.1 million, or $0.01 per share, in the prior-year period. This helped cap a nice year.

2017 results

Full-year 2017 equivalent production was 685.3 billion cubic feet equivalent (Bcfe), consisting of 655.6 billion cubic feet (Bcf) of natural gas, 4,440.9 thousand barrels (Mbbls) of crude oil and condensate, and 512.1 Mbbls of natural gas liquids (NGLs).

Full-year 2017 net income was $100.4 million, or $0.22 per share, compared to a net loss of $417.1 million, or $0.91 per share, in the prior-year period. Full-year 2017 adjusted net income (non-GAAP) was $244.5 million, or $0.53 per share, compared to an adjusted net loss of $97.3 million, or $0.21 per share, in the prior-year period.

These earnings represent a nice turn around from 2016. The question is, what are we looking for in 2018?

2018 projections

We will be quite clear here. We have high expectations for the year. Understand of course that we are levered to oil and natural gas prices. While oil prices have rebounded nicely, natural gas prices have continued to be weighed down by a strong supply. If prices rise, the stock will as well. It is as simple as that. What we can predict is production, while hoping for the best on commodity pricing.

For the first quarter, we are looking for natural gas production of 1,800 to 1,825 million cubic feet (Mmcf) per day for natural gas. We also expect that oil production will come in around 7,500 to 7,800 Bbls per day for crude oil and condensate, along with 700 to 800 Bbls per day for NGLs. Bear in mind that this factors in the Eagle Ford divestiture which is scheduled to close at the end of this month.

For the year, we see production growth of 12-16% as reported. If we adjust for the impacts of divestitures and closures, production growth is expected to be 20%. Management has indicated that is operating expenses will be below $1.60 per Mcfe, representing over a 20 percent improvement relative to 2017. Folks, this is an industry leading cash cost for production, which is why the company is able to remain this profitable especially with natural gas under $3.00. We think the company can generate up to $200 million of free cash flow at an average NYMEX price of $2.75, and can still generated growth with prices as low as $2.50.

Our take on the stock

All things considered, the company is weathering depressed natural gas prices well. It has gotten help from oil prices of late, but keep in mind that if the commodities rise in price it is a direct benefit to the bottom line. Considering that our expectations are for natural gas to eventually settle out around $3.00 and oil at $70 in the mid-term, we think the stock is a buy at present levels.

Quad 7 Capital has been a leading contributor with various financial outlets since early 2012. If you like the material and want to see more, scroll to the top of the article and hit ...

more