A Confusing End To Q2

The second quarter finished with a tricky question for markets. Did last week’s price action signal a significant change in tune or was it just insignificant noise in an unchanged trend of lower global long-term interest rates? One the one hand, it’s tempting for me to run a victory lap. Here I was musing about a steeper U.S. yield curve and outperformance in financials and energy. On that background the most recent price action has been a slam-dunk. On the other hand, I also said that I thought yields would fall over the summer, and that the reflation trade wouldn’t re-rear its head until Q3. So perhaps I shouldn’t raise my arms in celebration just yet. Bloomberg’s Guy Johnson probably was partly right when he said that:

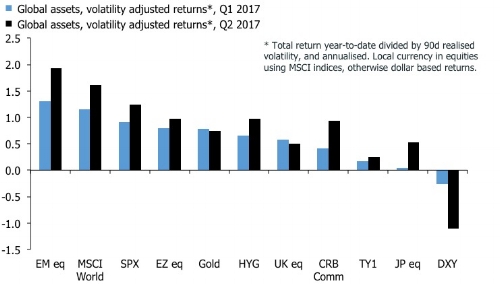

Last week's swoon in bond yields and stock markets didn't really change much in terms of the main stories. The chart below compares the volatility adjusted, and annualized, total returns of the main global assets markets in Q2, compared with their performance in Q1. Global equities continued to punch it in Q2, led by emerging markets but good ole' Spoos and Eurozone benchmarks also did well. The annualized performance of Japanese equities also jumped, but it dipped in the U.K. Overall, the strong equity market performance in Q2 mainly was a result of a strong start to the quarter. Performance tailed off ominously in June.

Gold stayed in the top half of the distribution, but momentum—on an annualiZed basis—weakened. Elsewhere, the performance of US high yield and the headline CRB commodities index improved, although many commodity investors probably haven't felt it given their overweight exposure to oil. In short, the headline CRB index rose because the dollar weakened. Speaking of which, the USD was once again stuck with the old maid, providing support for the contrarian axiom. Six months ago, everyone agreed that the dollar would be the star performer in 2017, but it's fair to say that it hasn't really worked out. Finally, despite all the talk about a flatter yield curve in the US, the long bond hasn't exactly smashed it on a volatility-adjusted basis. The annualized total return of US bond futures improved in the second quarter, but it continues to trail most other asset classes.

Despite the fact that markets in Q2 appear to have been singing to the same hymn sheet as in Q1, I think it is fair to say that the latter part of the quarter confused investors. In times like these, I think it is useful to write out the questions that I find most difficult to answer.

WHERE GOES "KING" DOLLAR?

The dollar will rebound eventually, but the interesting question is whether this could happen alongside a further rally in the long bond—lower yields—which seems to be the true contrarian bet at the moment. Arguably, the consensus got the underlying indicator right this year. Short-term interest rate differentials between the U.S. and the other major currencies have widened as the Fed has raised rates, but it hasn't worked as an indicator for currencies. Why not? I see three possible explanations.

Firstly, the widening interest rate differential was already priced in at the start of the year, and investors were complacently positioned for USD strength. It's normal for the market to do the exact opposite of informed wisdom in such situations, especially in FX markets.

Secondly, US economic data have disappointed. Seasonality issues notoriously plague the Q1 GDP numbers, but other data also have been poor. In particular, the decline in core inflation has been alarming to investors. It has alerted the market's attention to a potential "policy mistake" by the Fed. This, of course, is why everyone has been talking about the flattening yield curve. This is at least a little bit surprising given the uninterrupted decline in U.S. unemployment, which has historically been one of the best indicators of where the Fed is going.

Thirdly, the economic story elsewhere has changed in favor of other currencies. In the Eurozone, the economy is going from strength to strength, which has forced markets to at least contemplate the idea of the ECB will not keep the pedal to the metal forever. Meanwhile in the UK, investors have been shocked by the idea that the BOE could actually raise rates to protect the currency despite a slowing economy—EM style—to avoid an inflationary spiral. I think a good dose of skepticism is warranted on both of these stories, but markets love narratives.

You don't have to be a technical guru to see that if the GBPUSD and EURUSD consolidate above 1.30 and 1.15 respectively, it would constitute a significant change compared to where expectations were just six-to-nine months ago. In my neck of the woods, though, I am pretty sure that a EURUSD persistently above 1.15 would create problems all over the place in Frankfurt. After all, the current ECB staff projections are running with an assumption of 1.07 for their 2018 and 2019 CPI forecasts, so 1.15-to-1.20 would translate into a significant reduction in their already precariously low inflation forecasts.

HAS THE LONG BOND IN THE U.S. PEAKED FOR THE YEAR?

Last week was a reminder to U.S. bond bulls that nothing goes up in a straight line, but it seems to me that the move wasn't driven by news in the U.S. Rather, bund traders threw a tantrum following Mr. Draghi's speech in Portugal, which was interpreted—oddly in my view—as hawkish. This in turn pulled US 10-year yields higher. Maybe the story is simply that the Fed won't get any traction on long rates until something changes in the Eurozone and in Japan. If that's the case, the "lower-for-longer" narrative is unlikely to go away just yet.

I am not completely convinced that the long bond in the U.S. is about to roll over just yet. We haven't yet seen that deep dive in yields, and subsequent capitulation by the shorts, marking previous reversals in yields. I concede that this is a risky statement light of just flat the yield curve in the U.S. is, not to speak of how deeply negative the macroeconomic surprise index is. If U.S. economic data improve relative to the consensus in Q3 and Q4—and the Fed continues to push rates higher—bond markets will have to take a stand on the state of the world. Whatever they choose, I suspect will tell us a lot about what happens next.

CAN EQUITIES KEEP IT UP?

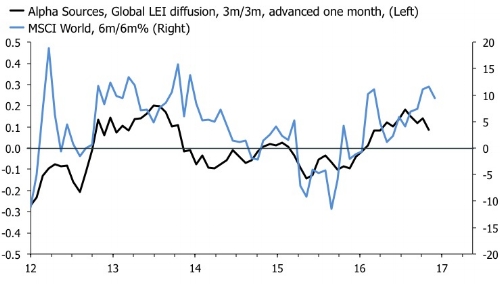

Currencies and bonds have got most of the attention in the first half of the year, mainly because the idea that benchmark equity indices could ever do anything but go up has appeared far fetched. My first chart above bears witness to just how strong these markets have been this year. The MSCI EM, for example, was up a cool 36% annualized in the first six months of the year; the MSCI EU ex-UK and Spoos have been trailing with a "paltry" 18%. June, however, was altogether more difficult for equity longs. Spoos crept higher by 0.3%, but the MSCI EM and MSCI EU ex-UK fell by 0.6% and 2.8%. Are we finally at the point where equities take a step back? I have shown a plethora of charts and indicators in the past six-to-nine months to show that equities are running on fumes. But none of it has stuck, so I have opted to stand back and just let the market run. I suspect we will know quickly if and when the trend turns. One thing which has changed slightly recently—headline valuation scores are still very negative—is that momentum of global macroeconomic leading indicators have rolled over.

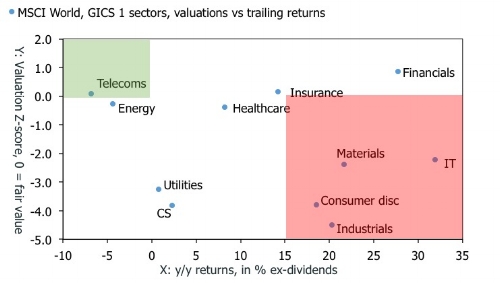

Assuming that trailing six-month returns of the MSCI World dwindles further to 4%-to-5% in July would imply a 2.2% month-to-month decline. That's shouldn't be life threatening, but even if everything ends well for equity investors in 2017—and I think it probably will—a hot summer could still ruffle a few feathers. Looking beyond the will-she-won't-she discussion about global equities, the sector story remains more interesting. Last week, I mused that the distinction between growth and value—effectively tech vs financials/energy—could be an interesting pivot in the second half of the year. This idea is somewhat supported if we look at valuation and returns of the GICS 1 sectors in the MSCI World.

Energy and financials are attractive based on valuations compared to most other industries, and telecoms also come out favourably. In the U.S., Verizon and AT&T look a bit like falling knives, and the long-term chart of the MSCI World Telecoms look poised for a break lower. But surely, Joe Sixpack still needs to call his girlfriend and surf the internet going forward, right?

Elsewhere, I would love to buy back the position in Wells Fargo that did so well for the portfolio earlier this year, but I am loathe to hit the bid before we enter Q3. I am also looking fondly at General Electric following its recent dive as well as a number of other single names such as XPER, TNH, GNTX and a smash-and-grab in camera land for GoPro and Ambarella. I have exchanged the broad position in global healthcare—IXJ us equity—for a position in UTHR. Basically, I like the sector, but I am a little worried that JNJ is about to edge lower, so I would rather rotate back into the broad index later. Finally, I have also added some selective EM exposure via RDY us equity. Select European financials could also be interesting soon, especially if the big boys are able to get assets virtually for free as the ECB moves to restructure the turds of the industry.

Overall though, the portfolio had another difficult month in June, partly due to the weaker US dollar and the fact that Vodafone went ex-div and decided, annoyingly, to not close the gap. The dividend will come in, though, lifting the cash position in July. Many of the other core positions didn't perform either, however, with Vectura in particular still languishing. Adding insult to injury, one of my penny stock bets deteriorated disastrously close to bankruptcy. I hope they scrape through, but they need equity it seems, and fast. All in all then, Q2 was a quarter to forget after a great start to the year. I am hoping Q3 will be better, but I confess that I enter it more confused than when it started.

Disclosure: None