5 Stocks To Watch This Week 1/30 - XOM, UA, AAPL, FB, AMZN

Tuesday, January 31

![]()

![]()

Wednesday, February 1

![]()

Thursday, February 2

![]()

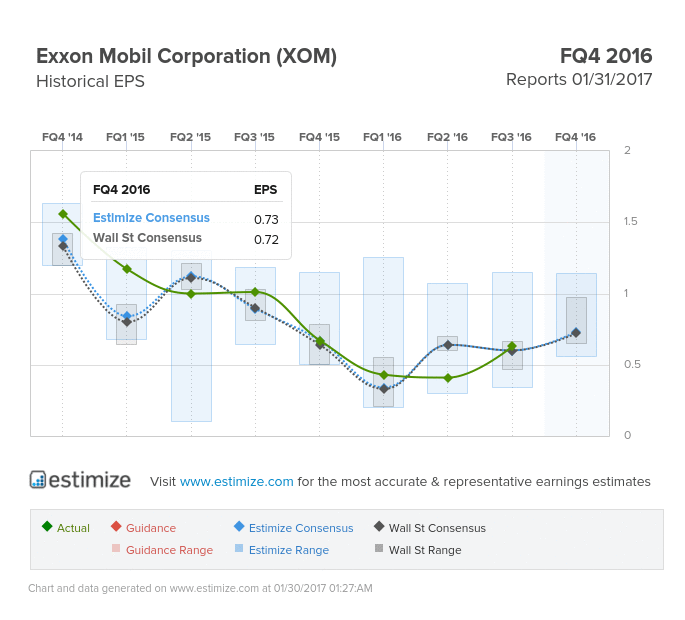

Exxon Mobil (XOM)

Energy - Oil, Gas & Consumable Fuels | Reports January 31, before the open.

The Estimize consensus is looking for earnings per share of $0.73, one cent above the sell-side consensus and 13% higher than the same period a year earlier. That estimate has decreased 4% since XOM’s last quarterly report. Revenue is anticipated to increase 5% to $62.45 billion, $1.1B below Wall Street.

What to Watch: After recording negative YoY EPS growth for the last 8 consecutive quarters, XOM is expected to post triple digit growth figures in 2017. Energy is finally starting to make a comeback, staying above the $50 mark so far this year. Promises from OPEC, and non-OPEC countries such as Russia to keep production low have given investors hope that prices could continue to improve throughout 2017, with many analysts targeting a range of $60 - $70/barrel. However, OPEC’s spotty record of adhering to such production quotas still has many skeptical about whether or not it will be carried out.

Oil & Gas companies couldn’t have a better advocates than former XOM CEO, Rex Tillerson, as the newly appointed Secretary of State (if confirmed), and President-elect Trump who supports the removal of EPA regulations which have hampered the industry.

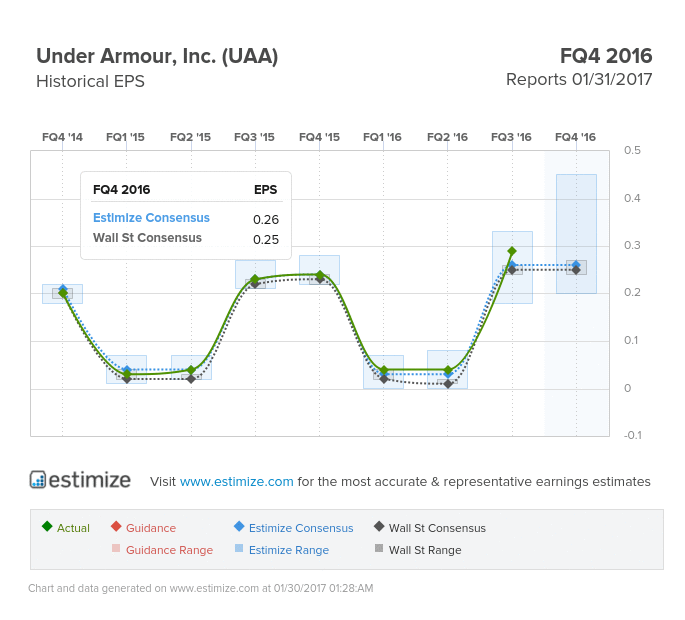

Under Armour (UA)

Consumer Discretionary - Textiles, Apparel & Luxury Goods | Reports January 31, before the open.

The Estimize consensus is looking for earnings of $0.26 per share on $1.42 billion in revenue, 1 cent higher than Wall Street on the bottom line and in-line on the top. Compared to a year earlier, earnings are expected to increase 11% with revenue jumping 21%. EPS estimates have been pushed down by 5% since the last quarterly report, and revenue estimates have come down 1%.

What to Watch: Once thought of as a viable threat to Nike’s (NKE) dominance, Under Armour has fallen victim to a recent rough patch. Unseasonably warm weather has affected sales of items such as coats and winter hats. On the heels of a poor holiday season, shares of Under Armour plunged 25% in the past three months. In a competitive footwear and apparel industry, Under Armour has positioned itself as a premium brand against Nike and Lululemon (LULU). Typically, the fourth quarter is peak season for retailers, however accumulating inventory and decelerating demand for Under Armour’s key products is expected to put a damper on Q4 earnings. On the bright side, Under Armour will benefit from the fast growing athletic footwear industry, new product offerings, a strong portfolio of athlete endorsements, and expansion of its direct to consumer strategy.

Unusually warmer weather dragged down sales of the company’s winter apparel and footwear segment. Winter clothing typically entails higher margins and as these products go on sale, this will prove to be a drag on margins. That said, Under Armour’s strong FY 2015, which reported its first quarter of over $1 billion in revenue, has set a promising tone for 2016. The company’s fastest growing sector, footwear, continues to outpace the overall business led by the launch of NBA champion, Stephen Curry’s exclusive shoe line.

Under Armour has also announced a line of connected footwear and apparel which track key fitness metrics while you exercise. It is anticipated that Health Box will stimulate revenue growth, but also attract new customers to the Under Armour ecosystem. Though the company generates a majority of its revenue from the United States, it intends to expand operations globally in an effort to reach a broader customer base.

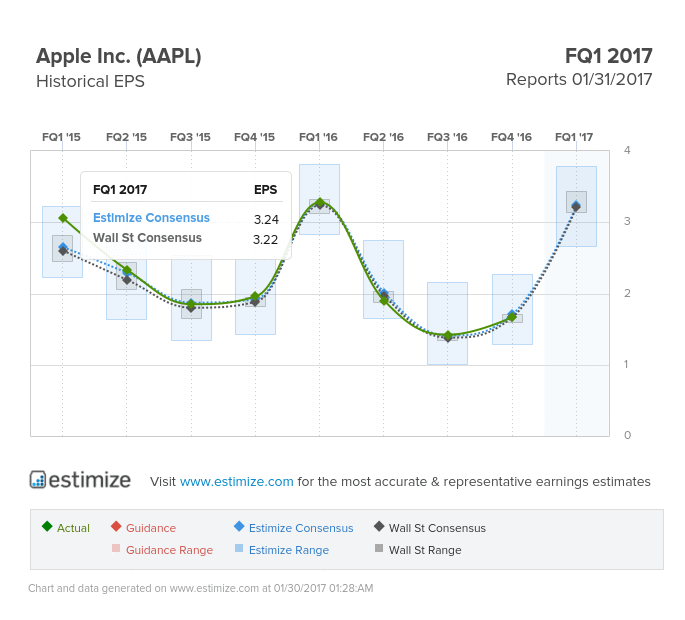

Apple (AAPL)

Information Technology - Computers & Peripherals | Reports January 31, after the close.

The Estimize consensus is looking for earnings per share of $3.24, 2 cents above the Wall Street consensus and down 2% from the same period last year. That estimate has increased 2% since Apple’s most recent report. Revenue is anticipated to increase 1% YoY to $76.99 billion, as compared to the sell-side’s consensus of $76.93 billion.

What to Watch: How many iPhones were sold in the fourth quarter? That’s what everyone wants to know come Tuesday afternoon. Overall sentiment is that the iPhone 7 has not performed as well as its preceding models, which doesn’t bode well for Apple as it relies heavily on sales of its smartphone as the engine of its overall business. Currently, many analysts are not seeing any new products on the horizon that could be a catalyst for forward growth, even the iPhone 8 may not do it. Apple hasn’t shown much progress on some of their bigger long-shot projects such as AI, as competitors such as Google have. This is an issue considering Apple’s very high valuation relative to expected growth.

It’s even difficult to predict Apple’s report by looking at the chip suppliers that have reported thus far. Current supplier Skyworks blew away Q4 results on the both the top and bottom-line, while former Apple supplier, Qualcomm missed expectations and new Apple supplier Intel met estimates.

The stock, which had been stuck at $120 mark for a couple of weeks, finally pushed above that level last week after news that Apple was close to striking a tax and incentives deal with Indian government officials to manufacture products in India.

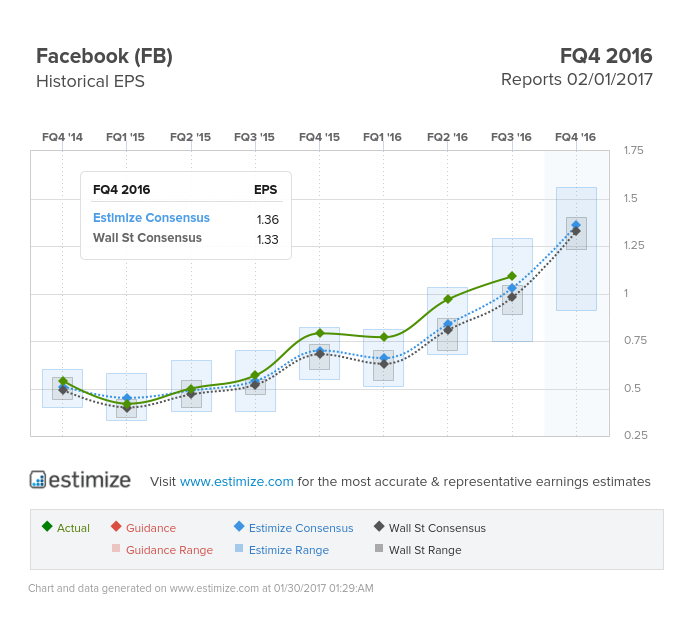

Facebook (FB)

Information Technology - Internet Software & Services | Reports February 1, after the close.

The Estimize consensus calls for EPS of $1.36, 3 cents above the Wall Street consensus. Revenue expectations of $8.495 billion are $53M above the sell-side consensus. Expectations have increased 6% since last quarter, putting YoY growth expectations at 68% for EPS and 45% for sales.

What to watch: Once again this quarter, the focus will be on user growth for Facebook, a number that has been stagnating. For the last two quarters Daily Active Users (DAUs) have been stuck at 17% growth, but that has slightly outpaced Monthly Active User (MAUs) growth of only 15 - 16% growth in that time, a positive that shows users are engaged more frequently. The breakdown after last quarter in Facebook’s stock highlights investor fears of slowing growth. The big deceleration this quarter may be priced in already, but their could be another shoe to drop on the multiple which is at 25x forward earnings. With the Snapchat IPO imminent the Instagram numbers are going to be important as its closest competitor.

Amazon (AMZN)

Consumer Discretionary - Internet Retail | Reports February 2, after the close.

The Estimize consensus is looking for earnings per share of $1.50 on $44.495 billion in revenue, above Wall Street by 8 cents on the bottom-line and $104M on the top. Compared to a year earlier, this reflects a 62% increase in earnings and a 22% increase on sales. Earnings estimates have decreased by 32% since the last quarter, while revenues have increased 1%.

What to Watch: Amazon is taking on retail and so much more, between Prime, Echo, Amazon Web Services and the Amazon Go, the internet company has it’s hands in everything. The Estimize community is expecting a return to triple digit earnings growth by the second half of the year.

Amazon reached a number of milestones last year and there’s no doubt it will reach so many more in 2017, but that doesn’t mask some of the glaring issues that caused earnings estimates to edge lower for Q4. Analysts have been entirely too optimistic that the retailer will grow at a rapid clip and last quarter’s earnings miss just made that more evident. Amazon kicked off fiscal 2016 with two consecutive quarters of nearly 1000% growth on the bottom line, leading analysts to believe a similar outcome would be seen in the third quarter. Therefore, a 206% increase in Q3 fell well below the market’s expectations and caused shares the inch lower.

Amazon Web Services (AWS) growth still looks incredibly strong which is what’s pushing the bottom line right now. The company is also expected to put up some big numbers associated with holiday sales as Amazon stole a lot of market share from its peers in Q4. We’re looking for comments on Amazon Go and the book store concept. With a stable multiple, and a CEO that seems to be able to deal with anything thrown their way, forward estimates are on their way up.

(Photo Credit: Gonzalo Baeza)

Disclosure: None.

Thanks for sharing