5 Of The Worst Stocks To Invest In – February 2017

The market is filled with companies with a lot of hype which are touted as great investments, but Benjamin Graham taught that intelligent investors must look past the hype and avoid speculating about a company’s future. By using the ModernGraham Valuation Model, I’ve selected five of the most overvalued companies reviewed by ModernGraham.

Each company has been determined to not be suitable for either the Defensive Investor or the Enterprising Investor according to the ModernGraham approach. Defensive Investors are defined as investors who are not able or willing to do substantial research into individual investments, and therefore need to select only the companies that present the least amount of risk. Enterprising Investors, on the other hand, are able to do substantial research and can select companies that present a moderate (though still low) amount of risk. Each company suitable for the Defensive Investor is also suitable for Enterprising Investors.

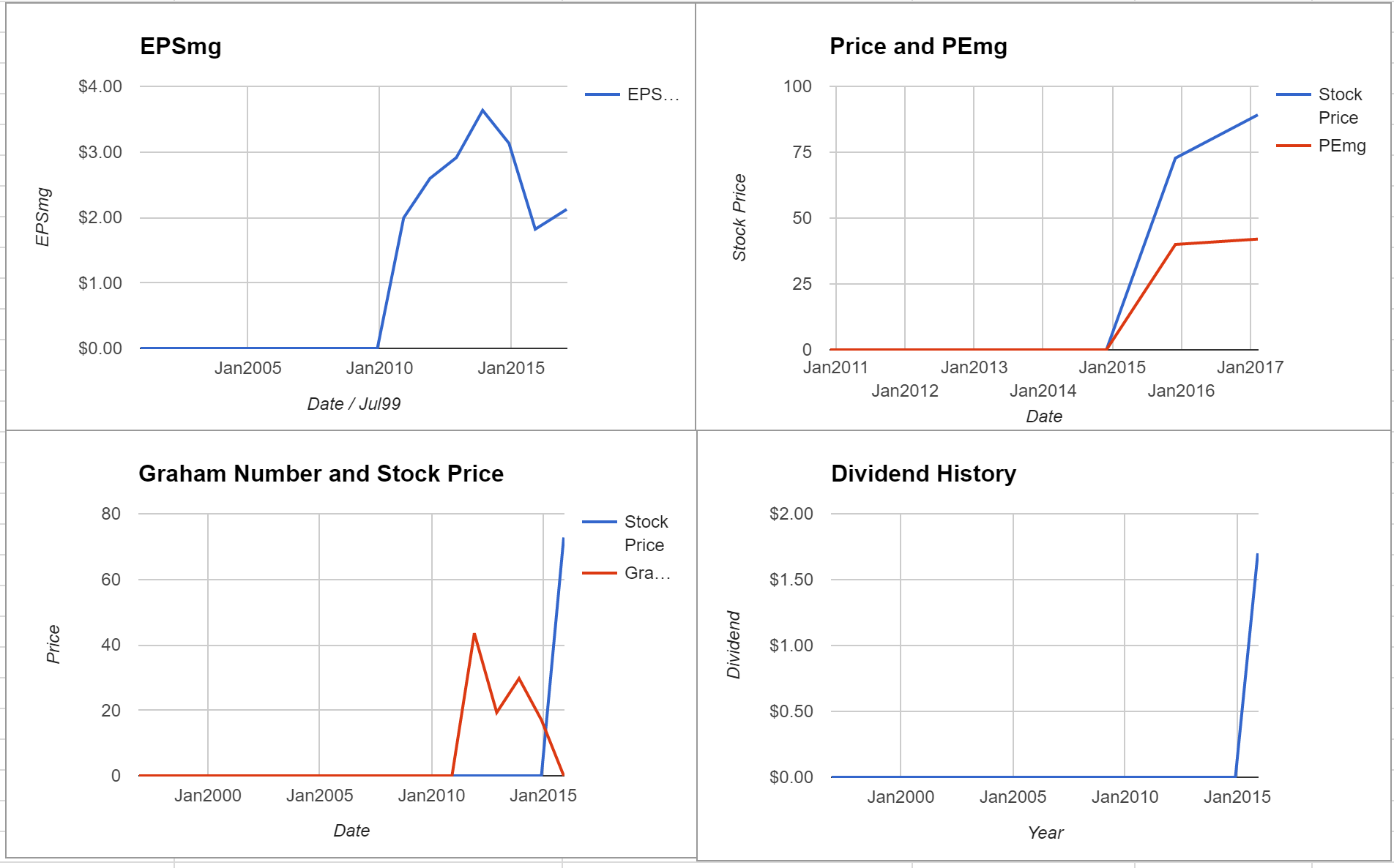

Kraft Heinz Co (KHC)

Kraft Heinz Co does not satisfy the requirements of either the Enterprising Investor or the more conservative Defensive Investor. The Defensive Investor is concerned with the low current ratio, insufficient earnings stability over the last ten years, the poor dividend history, and the high PEmg ratio. The Enterprising Investor has concerns regarding the level of debt relative to the current assets, and the lack of earnings stability or growth over the last five years. As a result, all value investors following the ModernGraham approach should explore other opportunities at this time or proceed cautiously with a speculative attitude.

As for a valuation, the company appears to be Overvalued after seeing its EPSmg (normalized earnings) decline from $2.91 in 2012 to an estimated $2.12 for 2016. This level of demonstrated earnings growth does not support the market’s implied estimate of 16.77% annual earnings growth over the next 7-10 years. As a result, the ModernGraham valuation model, based on the Benjamin Graham value investing formula, returns an estimate of intrinsic value below the price.

At the time of valuation, further research into Kraft Heinz Co revealed the company was trading above its Graham Number of $58.75. The company pays a dividend of $2.9 per share, for a yield of 3.3%, putting it among the best dividend paying stocks today. Its PEmg (price over earnings per share – ModernGraham) was 42.03, which was above the industry average of 24.74. Finally, the company was trading above its Net Current Asset Value (NCAV) of $-44.38. (See the full valuation)

(Click on image to enlarge)

Semtech Corporation (SMTC)

Semtech Corporation does not satisfy the requirements of either the Enterprising Investor or the more conservative Defensive Investor. The Defensive Investor is concerned with the insufficient earnings stability or growth over the last ten years, the poor dividend history, and the high PEmg and PB ratios. The Enterprising Investor has concerns regarding the lack of earnings stability or growth over the last five years, and the lack of dividends. As a result, all value investors following the ModernGraham approach should explore other opportunities at this time or proceed cautiously with a speculative attitude.

As for a valuation, the company appears to be Overvalued after seeing its EPSmg (normalized earnings) decline from $0.83 in 2013 to an estimated $0.2 for 2017. This level of demonstrated earnings growth does not support the market’s implied estimate of 81.3% annual earnings growth over the next 7-10 years. As a result, the ModernGraham valuation model, based on the Benjamin Graham value investing formula, returns an estimate of intrinsic value below the price.

At the time of valuation, further research into Semtech Corporation revealed the company was trading above its Graham Number of $14.59. The company does not pay a dividend. Its PEmg (price over earnings per share – ModernGraham) was 171.1, which was above the industry average of 28.12. Finally, the company was trading above its Net Current Asset Value (NCAV) of $0.36. (See the full valuation)

(Click on image to enlarge)

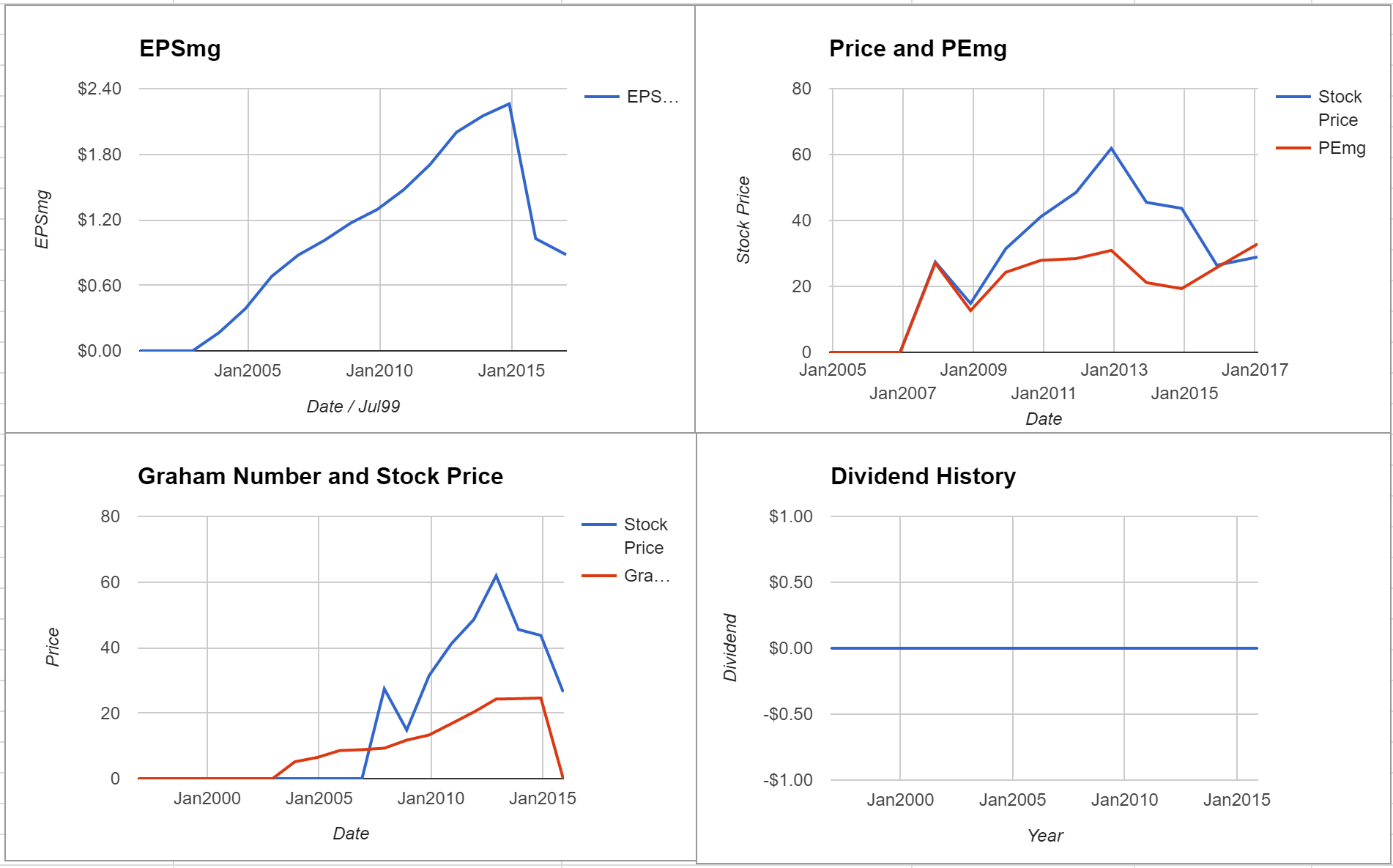

Semtech Corporation (TDC)

Teradata Corporation does not satisfy the requirements of either the Enterprising Investor or the more conservative Defensive Investor. The Defensive Investor is concerned with the insufficient earnings stability or growth over the last ten years, the poor dividend history, and the high PEmg and PB ratios. The Enterprising Investor has concerns regarding the lack of earnings stability or growth over the last five years, and the lack of dividends. As a result, all value investors following the ModernGraham approach should explore other opportunities at this time or proceed cautiously with a speculative attitude.

As for a valuation, the company appears to be Overvalued after seeing its EPSmg (normalized earnings) decline from $2 in 2012 to an estimated $0.88 for 2016. This level of demonstrated earnings growth does not support the market’s implied estimate of 12.18% annual earnings growth over the next 7-10 years. As a result, the ModernGraham valuation model, based on the Benjamin Graham value investing formula, returns an estimate of intrinsic value below the price.

At the time of valuation, further research into Teradata Corporation revealed the company was trading above its Graham Number of $13.15. The company does not pay a dividend. Its PEmg (price over earnings per share – ModernGraham) was 32.86, which was below the industry average of 38.13, which by some methods of valuation makes it one of the most undervalued stocks in its industry. Finally, the company was trading above its Net Current Asset Value (NCAV) of $1.03. (See the full valuation)

(Click on image to enlarge)

Silicon Laboratories (SLAB)

Silicon Laboratories does not satisfy the requirements of either the Enterprising Investor or the more conservative Defensive Investor. The Defensive Investor is concerned with the insufficient earnings growth over the last ten years, the poor dividend history, and the high PEmg and PB ratios. The Enterprising Investor has concerns regarding the lack of earnings growth over the last five years, and the lack of dividends. As a result, all value investors following the ModernGraham approach should explore other opportunities at this time or proceed cautiously with a speculative attitude.

As for a valuation, the company appears to be Overvalued after seeing its EPSmg (normalized earnings) decline from $1.27 in 2012 to an estimated $1.15 for 2016. This level of demonstrated earnings growth does not support the market’s implied estimate of 25.39% annual earnings growth over the next 7-10 years. As a result, the ModernGraham valuation model, based on the Benjamin Graham value investing formula, returns an estimate of intrinsic value below the price.

At the time of valuation, further research into Silicon Laboratories revealed the company was trading above its Graham Number of $26.34. The company does not pay a dividend. Its PEmg (price over earnings per share – ModernGraham) was 59.28, which was above the industry average of 28.12. Finally, the company was trading above its Net Current Asset Value (NCAV) of $5.34. (See the full valuation)

(Click on image to enlarge)

Staples, Inc. (SPLS)

Staples, Inc. does not satisfy the requirements of either the Enterprising Investor or the more conservative Defensive Investor. The Defensive Investor is concerned with the low current ratio, insufficient earnings stability or growth over the last ten years, and the high PEmg ratio. The Enterprising Investor has concerns regarding the lack of earnings stability or growth over the last five years. As a result, all value investors following the ModernGraham approach should explore other opportunities at this time or proceed cautiously with a speculative attitude.

As for a valuation, the company appears to be Overvalued after seeing its EPSmg (normalized earnings) decline from $0.72 in 2013 to an estimated $0.1 for 2017. This level of demonstrated earnings growth does not support the market’s implied estimate of 40.3% annual earnings growth over the next 7-10 years. As a result, the ModernGraham valuation model, based on the Benjamin Graham value investing formula, returns an estimate of intrinsic value below the price.

At the time of valuation, further research into Staples, Inc. revealed the company was trading above its Graham Number of $0. The company pays a dividend of $0.48 per share, for a yield of 5.4%, putting it among the best dividend paying stocks today. Its PEmg (price over earnings per share – ModernGraham) was 89.11, which was above the industry average of 50.09. Finally, the company was trading above its Net Current Asset Value (NCAV) of $0.91. (See the full valuation)

(Click on image to enlarge)

Disclaimer: The author did not hold a position in any company mentioned in this article at the time of publication and had no intention of changing that position within the next 72 ...

more