3 Soaring Oil Stocks To Ride The Energy Surge

Oil prices are rallying- and energy stocks are looking particularly compelling right now. Brent crude, the international benchmark, peaked at over $75 a barrel for the first time in four years. Multiple catalysts are pushing prices higher from robust demand, supply challenges and increasing geopolitical tensions across the Middle East.

Analysts highlight the chance of renewed U.S. sanctions on Iran as a key factor driving prices. “If Trump abandons the deal [to lift sanctions], he risks a spike in global oil prices… A reintroduction of sanctions without seeing other OPEC-members increase production could remove an estimated 300,000-500,000 bpd of Iranian barrels,” says Ole Hansen, head of commodity strategy at Saxo Bank.

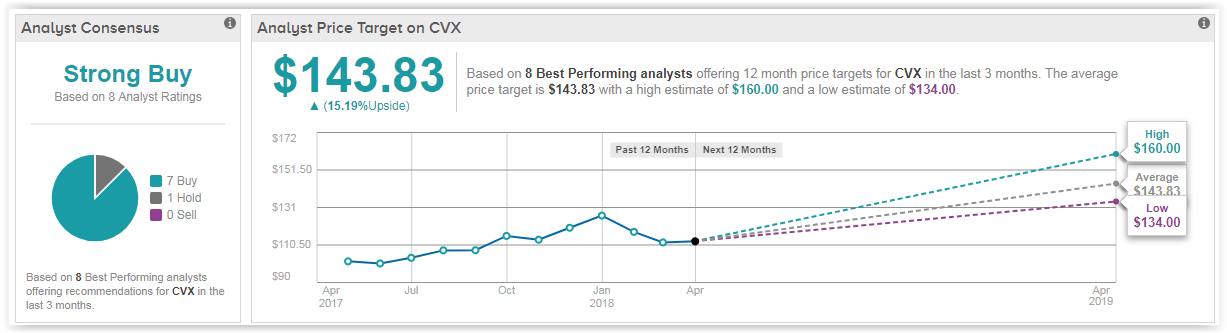

Chevron Corporation (NYSE:CVX)

Shares in California-based oil giant Chevron are spiking right now. In the last month shares are up 11%. Crucially, Chevron stands to benefit the most from greater upside to oil prices. RBC Capital’s Biraj Borkhataria explains: “Higher commodity prices are obviously a catalyst for any commodity producer, but Chevron would likely benefit more than peers given its high operating leverage, especially with its liquids-heavy exposure.” In 2017, for example, Chevron produced 2.728 million net oil-equivalent barrels per day from its operations around the world.

At the same time, Chevron’s 1Q earning results “will have positive impact on its near-term share performance,” with results strong across the board “in stark contrast to an uninspiring print by Exxon,” according to Barclays’ Paul Cheng.

“(Chevron’s) positive first-quarter result was an encouraging sign that Chevron is executing well and we remain constructive on the company’s long-term, shareholder-friendly plan,” the analyst said. Indeed, Chevron is one of the best dividend stocks out there with a highly lucrative 3.6% dividend yield. This translates into a quarterly dividend payment of $1.12.

Cheng ramped up his price target to $145 (16% upside potential). Overall, Chevron boasts seven buy ratings and only one hold rating from top-performing analysts. These analysts see Chevron shares rising a further 15% to hit $144. You can click on the screenshot below for further insights into these ratings:

(Click on image to enlarge)

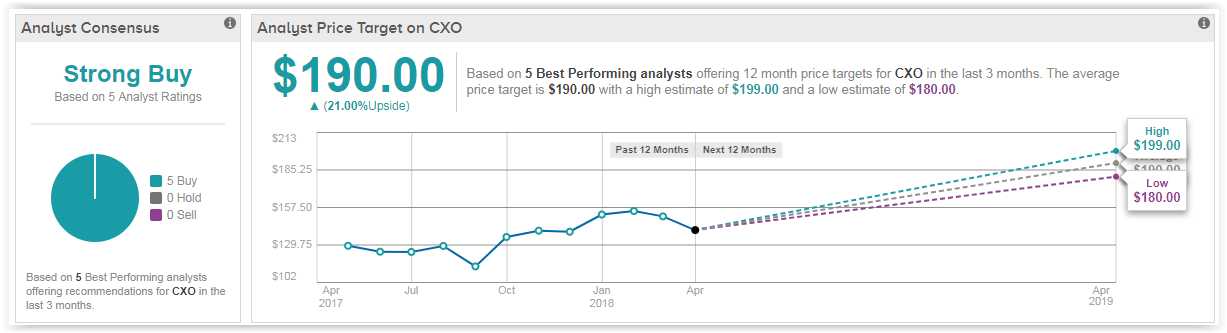

Concho Resources (NYSE:CXO)

Now is the ‘Time to Flex Your Muscles’ writes RBC Capital’s Scott Hanold on our second energy stock. This is because Concho Resources is now poised to become the biggest player in the Permian Basin. Earlier in April, Concho announced a massive $9.5 billion deal to snap up fellow Permian fracker RSP Permian.

Hanold tells clients he is impressed by the ‘complimentary’ deal. He notes: “our well data shows RSP Permian wells are among the most prolific, portending to improving returns.” And the icing on the cake: management is modelling for an impressive $2 billion in acquisition synergies. After the deal closes in the third quarter, these efficiencies should materialize quickly, says management.

As for Concho itself: “Core activity should generate industry-leading returns, margins, and growth. CXO has a well-established asset base and is one of the largest producers and the most active operator in the Permian Basin. We think this scale provides significant advantages over its peers”.

Shares in Concho have popped 12% in the last month, and according to the Street there is still big growth potential ahead. Indeed, the average analyst price target of $190 indicates 21% upside from current levels. Plus, our data shows that in the last three months, 5 out of 5 top analysts have rated this stock a ‘Buy’.

(Click on image to enlarge)

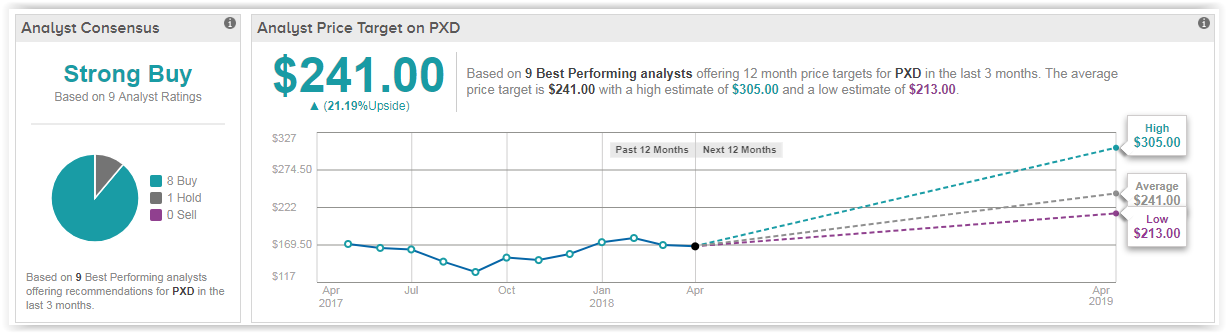

Pioneer Natural Resources (NYSE:PXD)

Oil and gas stock Pioneer Natural also has a strategy to become a pure-play on the Permian Basin. According to the company, in the Permian Basin alone, Pioneer’s acreage could contain 20,000 drilling locations and a whopping 11 BBOE (billion barrels of oil equivalent). And by divesting assets outside the Permian Basin (including Eagleford, Raton (CO), South Texas, and West Panhandle (TX), Pioneer stands to raise funds of between $600-$900 million.

Most encouragingly, top Goldman Sachs analyst Brian Singer has just added Pioneer to his exclusive ‘Conviction Buy’ stock list. Encouragingly, tapping Singer’s name into TipRanks reveals he has a strong track record with his stock recommendations- hence his four-star ranking:

While upgrading the stock, Singer hiked up his price target to $231. PXD scores highly on a number of metrics says Singer, including debt-adjusted growth, free-cash-flow, and balance sheet fundamentals. And the best part for shareholders is that this excess free cash flow is widely expected to fund strong stock buybacks and higher dividend payouts.

Our data reveals that this ‘Strong Buy’ stock has received 8 recent buy ratings vs just 1 hold rating. In the last month shares are up 19% and looking forward, and analysts are predicting (on average) further upside potential of 21% to $241.

(Click on image to enlarge)

Disclaimer: TipRanks is an independent cloud based service that measures and ranks digitally published financial advice. TipRanks' natural language processing (NLP) algorithms aggregate and ...

more