Macro Mondays: Jensen's 'Alpha'

It's no coincidence that many investment publications refer to alpha as the end all be all for investors. The reason? It's an easy way to determine if the investment (namely a mutual fund) is earning the kinds of returns you would expect given a certain level of risk. Risk-adjusted returns are very important to consider when investing, especially if you're the kind of investor whose very concerned at the potential of losing money. If this sounds like you, then you had better learn a thing or two about Jensen's alpha.

For more information about Alpha and other evaluation metrics, visit Investopedia and learn more!

What is Jensen's 'Alpha'

Jensen's Alpha is used in finance to represent two things:

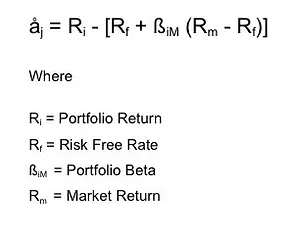

1. A measure of performance on a risk-adjusted basis, and is represented by the following formula:

Alpha, often considered the active return on an investment, gauges the performance of an investment against a market index used as a benchmark, since they are often considered to represent the market’s movement as a whole. The excess returns of a fund relative to the return of a benchmark index is the fund's alpha.

Alpha is most often used for mutual funds and other similar investment types. It is often represented as a single number (like 3 or -5), but this refers to a percentage measuring how the portfolio or fund performed compared to the benchmark index (i.e. 3% better or 5% worse).

Alpha is often used with beta, which measures volatility or risk, and is also often referred to as “excess return” or “abnormal rate of return.”

2. The abnormal rate of return on a security or portfolio in excess of what would be predicted by an equilibrium model like the capital asset pricing model (CAPM).

In this context, alpha is often known as the “Jensen index.”

What Are the Usual Limitations of 'Alpha'

While alpha has been called the “holy grail” of investing and, as such, receives a lot of attention from investors and advisors alike, there are a couple of important considerations that one should take into account before attempting to use alpha.

One such consideration is that alpha is used in the analysis of a wide variety of fund and portfolio types. Because the same term can apply to investments of such differing natures, there is a tendency for people to attempt to use alpha values to compare different kinds funds or portfolios with one another. Because of the intricacies of large funds and portfolios, as well as of these forms of investing in general, comparing alpha values is only useful when the investments contain assets in the same asset class.

Additionally, because alpha is calculated relative to a benchmark deemed appropriate for the fund or portfolio, when calculating alpha it is imperative that an appropriate benchmark is chosen. Because funds and portfolios vary, it is possible that there is no suitable pre-existing index, in which case advisors will often use algorithms and other models to simulate an index for comparative purposes.despite the considerable desirability of alpha in a portfolio, index benchmarks manage to beat asset managers the vast majority of the time.

So how accurate and is the use of alpha in evaluating mutual funds?

Due in part to a growing lack of faith in traditional financial advising brought about by this trend, more and more investors are switching to low-cost passive online advisors (often called robo-advisors ) who exclusively or almost exclusively invest clients’ capital into index-tracking funds, the thought being that if they cannot beat the market they may as well join it.

Moreover, because most “traditional” financial advisors charge a fee, when one manages a portfolio and nets an alpha of 0, it actually represents a slight net loss for the investor. For example, suppose that Jim, a financial advisor, charges 1% of a portfolio’s value for his services and that during a 12-month period Jim managed to produce an alpha of 0.75 for portfolio of one of his clients, Frank. While Jim has indeed helped the performance of Frank’s portfolio, the fee that Jim charges is in excess of the alpha he has generated, so Frank’s portfolio has experienced a net loss. Because of these developments, managers face more pressure than ever to produce results.

Evidence shows that active managers’ rates of achieving alpha in funds and portfolios have been shrinking substantially, with about 20% of managers producing statistically significant alpha in 1995 and only 2% in 2015. Experts attribute this trend to many causes, including:

-

The growing expertise of financial advisors

-

Advancements in financial technology and software that advisors have at their disposal

-

Increasing opportunity for would-be investors to engage in the market due to the growth of the internet

-

A shrinking proportion of investors taking on risk in their portfolios and

-

The growing amount of money being invested in pursuit of alpha.

Disclosure: None.

Disclaimer:

All data and information provided on this site is strictly the author’s opinion and does not constitute any financial, legal or other type ...

more