Norges Bank To Remain On Hold Despite Low Inflation

Øystein Olsen, Governor of the Central Bank of Norway. Image via Norges Bank. Foto: Jørgen Kvam

Further Rate Cuts Unlikely

At their September meeting, Norges Bank signalled that further rate cuts were unlikely to materialise and the deposit rate would instead remain close to 0.5% over the coming years. This forecast was largely fuelled by the mainland’s (ex-oil) recovery and concerns linked to financial stability, particularly regarding the housing market.

However, the central bank does continue to see a subdued environment for growth in the total economy, having downgraded their growth and inflation forecasts at the December meeting. This pessimism has likely peaked now, and with data sets highlighting improvement and positive momentum in the economy, there are risks of an upward revision to forecasts over 2017.

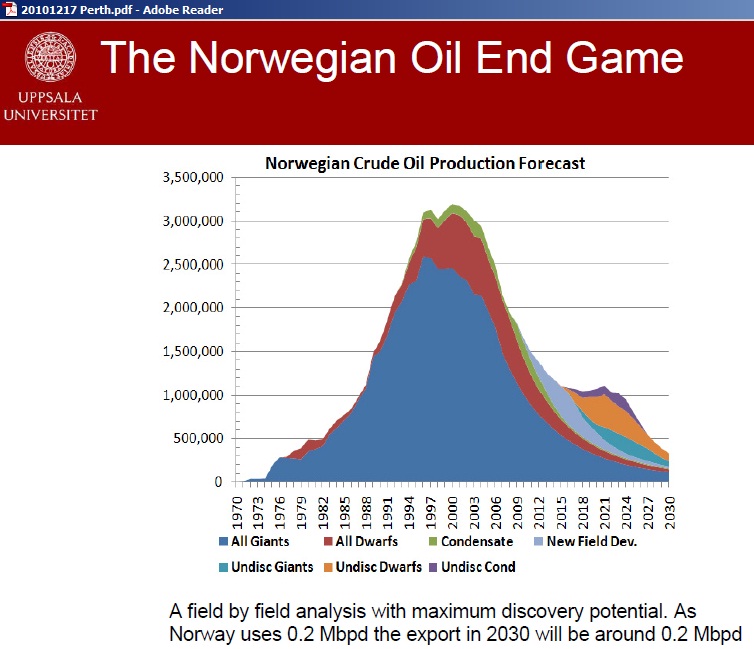

Oil Exports Increase + 80%

Norwegian Oil exports have significantly increased over recent months and are now up over 80% year on year. Consequently, and as a result of the rise of oil prices, the Norwegian trade balance has significantly improved following a slump since the oil price decline worsened in 2014.

Norwegian oil production has also increased, in volume terms, and there is scope for further improvement of the basic balance due to portfolio inflows driven by higher oil prices. Safe-haven flows fuelled by the upcoming election risks in the Eurozone could also spark an acceleration of inflows. With these elements in mind, the Norwegian flow picture continues to look promising and should provide further support for NOK.

(Click on image to enlarge)

Image via Crude Oil Peak

Norwegian oil production has also increased, in volume terms, and there is scope for further improvement of the basic balance due to portfolio inflows driven by higher oil prices. Safe-haven flows fuelled by the upcoming election risks in the Eurozone could also spark an acceleration of inflows. With these elements in mind, the Norwegian flow picture continues to look promising and should provide further support for NOK.

What will be of key importance to GDP growth is how the Oil sector responds to increased revenues. Norwegian Oil companies’ investment outlooks should further improve over 2017 due to a combination of lower breakeven costs and higher oil prices. The details of the 2016 Q4 total economy GDP print are positive. GDP rose to 1.9% year on year from -1% in Q3, and there was a significant contribution from

The details of the 2016 Q4 total economy GDP print are positive. GDP rose to 1.9% year on year from -1% in Q3, and there was a significant contribution from investment of 1.36% which is the highest contribution since Q2 2014. The next release, on 23rd February, is Statistics Norway’s oil investment survey which will be a key input for the March 16th Norges Bank meeting.

Risks to the positive outlook

Despite the positive signs in the Norwegian economy, there are risks to the outlook. In NOK terms, Oil prices are up almost 60% this year. One clear risk is that oil prices reverse their recent bullishness, possible as a consequence of increased US production. Another risk is the possibility of more limited fiscal stimulus from the government. The government recently proposed lower the real rate of return on the GPFG from 4% to 3% which would reduce the fiscal expenditure rule which states that a maximum of 4% (now 3%) of the government’s pension fund should be allocated to the government’s annual budget over time.

Another risk is the possibility of more limited fiscal stimulus from the government. The government recently proposed lower the real rate of return on the GPFG from 4% to 3% which would reduce the fiscal expenditure rule which states that a maximum of 4% (now 3%) of the government’s pension fund should be allocated to the government’s annual budget over time.

The government recently proposed lower the real rate of return on the GPFG from 4% to 3% which would reduce the fiscal expenditure rule which states that a maximum of 4% (now 3%) of the government’s pension fund should be allocated to the government’s annual budget over time.

Currently, the government expects the structural deficit in 2017 to be 3% of GDP in 2017 but could widen to around 3.3% in 2019. Consequently, there is a risk that fiscal stimulus expectations will be reduced after the spring budget on May 11th, which would factor into Norges Bank GDP growth forecasts. However, the government has also said that it will remain committed to supporting the domestic recovery which should see the limited impact.

Furthermore, Governor Olsen said in his annual address that he supported the recommendation from the government as it supports the long-run stability of the Norwegian economy. As a result, it is unlikely to be viewed as strongly negative by the bank as the policy positively shifts the longer-term balance of risks.

Weak Inflation Driven by temporary factors

Despite still low domestic inflation, the drivers behind the lack of upside price pressure are expected to be temporary. Norway’s core inflation rate significantly rose in mid-2015, mostly fuelled by higher import prices from NOK’s depreciation linked to the slump in oil prices. However, positive contributions to inflation from NOK’s weakness are now dissipating and have actually turned negative as NOK has strengthened. This dynamic has been weighing on the core inflation and at such a pace that not even Norges Bank has expected.

Norwegian inflation is likely to decline further over 2017 mostly driven by the currency. However, domestic factors continue to look promising. Capacity utilisation has put in a base as growth continues to recover. Importantly, in the same way, that the Norges Bank was willing to temporarily overlook high inflation as it eased, in response to lower oil prices, the bank is equally likely to be willing to look past low inflation caused by an unwinding of positive exchange rate effects.

Technical Perspective

(Click on image to enlarge)

For now, USDNOK remains firmly within a range between resistance around the 8.73 mark and support at the 7.96 level. The rising trend line from year’s lows provides immediate support while bearish trend line resistance overhead will be the first key objective for bulls.

Disclaimer: Orbex LIMITED is a fully licensed and Regulated Cyprus Investment Firm (CIF) governed and supervised by the Cyprus Securities and Exchange Commission ...

more

thanks for sharing