Japanese Yen Braces For Volatility As Trump Stirs The Pot

Fundamental forecast: Bearish

- Japanese Yen in position to fall even further versus the resurgent US Dollar on ‘Trump rally’

- Talk from Fed Chair Yellen sinks the JPY to fresh lows, puts upward pressure on USD/JPY

The Japanese Yen plummeted for the second-consecutive week as the US Dollar surged to 13-year highs, and a continuation of the so-called US President Elect ‘Trump Rally’ could push it to further lows. A holiday-shortened week for North American markets will shift focus to Japan. Barring any surprises, recent price action suggests the Yen is likely to trade lower until we see a substantive shift in market sentiment.

The key question for the Yen is straightforward: has the recent surge in US Treasury Yields and US interest rate expectations run its course? Investors have long made the Japanese Yen one of the most interest rate-sensitive currencies in the world, and the fact that US Dollar yields have risen helps explain why the USD/JPY exchange rate is suddenly at six month highs. US President-Elect Trump has promised to boost infrastructure spending and cut taxes—the combination of which would almost certainly increase government borrowing and hence the issuance of Treasury debt. Or in short: greater supply of debt would require higher yields such that investors will absorb the supply.

In that sense we need to watch rhetoric out of the President Elect to gauge how much of this is pre-election campaign talk and how much will be actual fiscal policy. Any indications to the contrary—that US government spending will not surge and/or tax revenues will not plummet—would force a significant correction in US Treasury markets. And given that the sudden jump in yields has ignited fears of inflation, it is little surprise to note the odds of US Federal Reserve interest rate hikes have likewise jumped following the US Presidential election.

Japanese Yen traders will otherwise look to the Bank of Japan to guide near-term moves in the Yen, and this is especially true as the recent global bond market sell-off has pushed Japanese Government Bond yields to the BoJ’s stated ceilings. In September BoJ Governor Haruhiko Kuroda and his staff announced the bank would purchase unlimited amounts of JGB’s in order to control rates. At the time yields were well-below these targets, but the recent market moves have forced the BoJ’s hand and it stands ready to put through its unlimited purchases. As things stand this artificial intervention seems achievable as one might argue the “true” JGB yield is not significantly beyond current levels. But at a certain point this quickly becomes untenable, and that will be a critical risk to watch for the Japanese Yen and the domestic financial system.

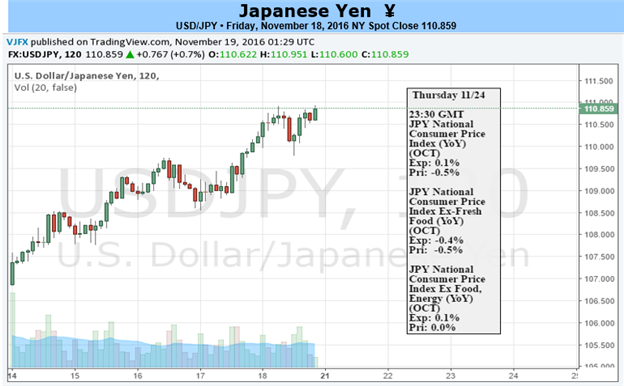

In the week ahead we’ll watch any especially-large surprises out of the coming week’s release of Japanese Consumer Price Inflation figures will otherwise drive JPY volatility. Traders have shown relatively little sensitivity to Japanese economic data, however; rhetoric from the BoJ matters far more than a single economic print.

Markets are entering extremely uncertain territory, and further Japanese Yen volatility seems almost guaranteed. Whether the JPY continues lower (USD/JPY higher) depends on whether the post-US election sell-off in US Treasury Yields continues. And in that sense all eyes are on the US President-Elect.

Continue tracking these setups and more throughout the week- Subscribe to more