Italy Approves 1.2% Of GDP To Save It's Troubled Banks... Again! Exactly As We Warned Last Year

I've been warning about Italy's troubled banks since 2010, and last year I pushed two very detailed reports about what was essentially Italy's Bear Stearns and Lehman Brothers. Italy is a mess and the IMF and EC have been too optimistic regarding its prospects for 7 years (not just lately), see Lies, Damn Lies, and Sovereign Truths: Why the Euro is Destined to Collapse! Fast forward to today and Bloomberg reports: Italy Approves $21 Billion Fund to Shore Up Its Troubled Banks

Italy’s parliament approved a law to plow as much as 20 billion euros ($21 billion) into Banca Monte dei Paschi di Siena SpA and other troubled lenders as part of the nation’s efforts to revamp its banking industry.

The lower house gave its final approval to the legislation Thursday, converting the decree law passed by Prime Minister Paolo Gentiloni’s cabinet in December. It includes emergency liquidity guarantees and capital injections for struggling lenders in compliance with state aid rules. Banks will be able to request precautionary recapitalizations that would see some bondholders take a hit.

... Italy’s banks are struggling under the weight of a 360 billion-euro mountain of bad loans, a plight that has eroded profitability and undermined investor confidence. Taking Monte Paschi into public ownership, which would be Italy’s biggest nationalization since the 1930s, could be followed by rescues of lenders including Veneto Banca SpA and Banca Popolare di Vicenza.

Keep in mind that Italy's GDP is only $1.8 trillion, meaning that it will put over 1% of its GDP into bailing failing banks, for the second time in 7 years!

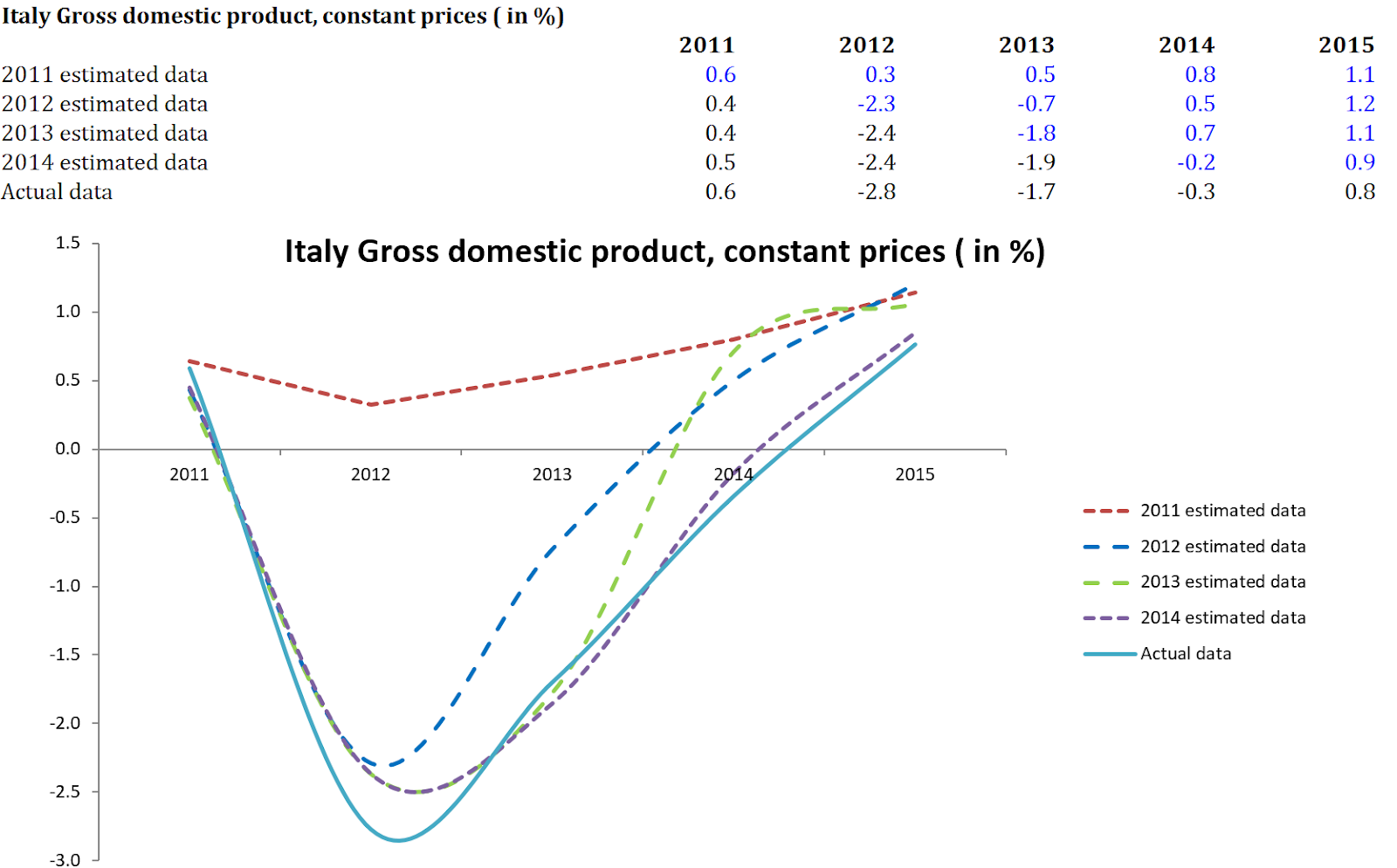

I have warned about Italian banks since 2010, but the IMF/EC said things were getting better. The IMF has always been overly optimistic when it comes to Italy.

As I've said, I've been warning about Italy's troubled banks since 2010. During the months of March and April of 2016 we released a series of proprietary research reports indicating significant weaknesses that we found in the European banking system and released it for sale through the blockchain (reference The First Bank Likely to Fall in the Great European Banking Crisis). This was performed by the same macro forensic and fundamental analysis team that first warned about the pan-European sovereign debt crisis in 2009 and 2010 (reference Pan-European sovereign debt crisis) as well as Bear Stearns and Lehman Brothers (Is this the Breaking of the Bear? January 2008).

Today, Reuters released news vindicating our position in spades, leading any institution that took a position via our blockchain-based Veritaseum trading platform or today's legacy system with 14% cash gains or 50% to 100+% leveraged gains in the short time period in question, to wit: Tumbling Banco Popolare leads Italian bank shares lower

- Banco Popolare shares fall 14 pct to record low

- Bank booked writedowns ahead of merger with Popolare Milano

- Italian banking shares dogged by concerns over bad loans (Recasts with details)

MILAN, May 11 Shares in Banco Popolare plunged 14 percent on Wednesday after a surprise first-quarter loss driven by loan writedowns -- the main focus of investor concerns over Italian banks.

Banco Popolare booked loan writedowns requested by the European Central Bank as a condition for approving a planned merger with Banca Popolare di Milano that will create Italy's third-biggest banking group.

To improve its loan loss provisions Banco Popolare must raise 1 billion euros in a share issue slated for early June.

Investors are expected to be more supportive of the move than was the case when Banca Popolare di Vicenza IPO-BPVS.MI tried to raise cash last month and had to be supported by a new bank rescue fund.

Shares in Banco Popolare lost 14 percent by 1040 GMT, hitting a record low of 4.14 euros.

Popolare Milano lost 10 percent to 0.50 euros, against a 3 percent drop in Italy's banking index.

Italian banks have lost nearly 40 percent of their market value so far this year, weighed down by concerns they could need additional capital to shoulder losses from sales of bad loans that rose to 360 billion euros ($410 billion) during a long recession.

A share rebound triggered by the hasty creation last month of the fund intended to inject capital into weaker lenders and buy their bad loans proved short-lived.

Banco Popolare said late on Tuesday that it had written down loans for 684 million euros in the first quarter, nearly four times more than in the same period of 2015, posting a net loss of 314 million euros for the first three months.

CEO Pier Francesco Saviotti told an analyst call that the loan writedowns were the first step towards selling chunks of bad loans and that it would book further provisions this year."

Let's take a look at what the Macrotechnology, fintech and blockchain research experts at Veritaseum had to say about Banco Popular. Keep in mind that although we are now a technology firm, we specialize in Fintech and Macrotech, hence keeping our finger on the pulse of the global banking system is paramount. We mush be aware of what it is that we are disintermediating! On that note, we will happily create a distributed blockchain solution using our realistic approach to isolate these risks in a zero trust confine, essentially bullet proofing parts of this bank or any other from catastrophic loss. Ping me for more.

Income from operations declined every year from 2011 due to lower interest margin and higher operating expense. The declining trend was stopped in 2015 as the bank recorded a rise of 13% in income from operations. The pop was due to sale of equity investments held in ICBPI (13.88%) and Arca SGR (19.9%) amounting to Euro172.6 and Euro68.7 million, respectively, and higher other operating income including fees and commission earned. However, the notable aspect is the core income from operations has been on constant decline (even in 2015) over the last few years

The quality of loans has been deteriorating with percentage of non-performing and bad loans showing signs of increase due to adverse macro-economic environment. Of the total loan portfolio, the bank’s performing loans decreased to 82.1% in 2015 from 83.7% in 2013. Furthermore, BP stopped reporting restructured loans for at least two years. That looks quite suspicious given that loan credit quality has been tumbling. The numbers offered add up, but they shouldn't unless the restructured loans have been somehow reclassified as performing loans (quite possibly). If so, that's quite misleading and should be duly noted.

A significant percentage of the loan portfolio comprises mortgage loans and loans on current accounts. Distressed residential real estate sector and subdued business environment are likely to take toll on % of performing loans in these categories. As can be seen below, Italy as a nation, has high NPLs and it is not materially improving, YoY.

Since the hyperlinks are not active in these report jpg snapshots, I'll past the text here so you can access the live links, reference Reggie Middleton vs Rating Agencies.

Parallels to Bear Stearns Before it Popped

In January of 2008, we warned (in exquisite detail) of the collapse of Bear Stearns. It was 2 months before Bear Stearns actually fell, while it was trading in the $100s and still had buy ratings and investment grade AA or better from the ratings agencies. See for yourself: Is this the Breaking of the Bear? As part of the analysis, we did a counterparty risk profile, see below:

Counterparty Risk

| In $million | OTC Derivative credit exposure ($ million) | ||||||

| TThe table summarizes the counterparty credit quality of the company's exposure with respect to OTC derivatives | |||||||

| Rating(2) | Exposure | Collateral (3) | Exposure, Net of Collateral (4) | Percentage of Exposure, Net of Collateral | Total exposure a % of Total assets | Net exposure as a % of Total assets | Net exposure as a % of equity |

| AAA | 3,369 | 56 | 3,333 | 42% | 0.8% | 0.8% | 25.6% |

| AA | 6,981 | 4,939 | 2,153 | 27% | 1.8% | 0.5% | 16.6% |

| A | 3,869 | 2,230 | 1,784 | 23% | 1.0% | 0.4% | 13.7% |

| BBB | 354 | 239 | 203 | 3% | 0.1% | 0.1% | 1.6% |

| BB and lower | 1,571 | 3,162 | 322 | 4% | 0.4% | 0.1% | 2.5% |

| Non-rated | 152 | 223 | 94 | 1% | 0.0% | 0.0% | 0.7% |

| 16,296 | 10,849 | 7,889 | 100% | 4.1% | 2.0% | 60.7% | |

| (1) Excluded are covered transactions structured to ensure that the market values of collateral will at all times equal or exceed the | |||||||

| related exposures. The net exposure for these transactions will, under all circumstances, be zero. How this is accomplished is beyond our ken, and likely not at true in the event of a liquidity crisis. | |||||||

| (2) Internal counterparty credit ratings, as assigned by the Company’s Credit Department, converted to rating agency equivalents. (3) Includes foreign exchange and forward-settling mortgage transactions) as of August 31, 2007 | |||||||

Banco Popular is slated to merge with Banco Popular Milano. We have performed a deep dive analysis on this bank as a standalone entity and assessed the synergistic benefits of a newly formed combined entity.

Disclosure: None.