For Those Looking For More Rate Hikes In Canada: A Lesson From The Past

During the latter part of the 1980s and early 1990s, the Bank of Canada steadily raised short term rates. This set off a series of major adjustments in consumer prices, in the value of Canadian dollar and, ultimately, in national income. Some observers have cast their eye back to that time period in order to glean insights on how to interpret the impact of recent policy decisions by the Bank of Canada. While history may not always repeat itself, it may serve as a useful guide to the future.

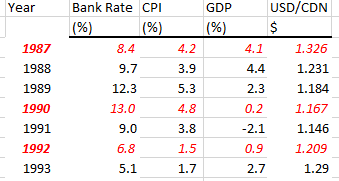

By 1987 the economy was well on its way to recovering from the devastation of a major recession in 1982-4. The bank rate had declined from its dizzy heights of 21% in 1982 to around 8%. Economic output responded and quickened to a healthy rate of just over 4%. Inflation, previously running around 10% in the earlier part of the decade, settled down to 4% . Housing prices had recovered remarkably from the 1982-4 recession and were moving up to new highs almost in lock step with the decline in interest rates. Economic conditions were favorable for continued growth.

However, the Bank of Canada was concerned that inflation was rearing its ugly head again and instituted a series of rate hikes starting from 8% in 1987 to a high of 13% in 1990. The Bank’s rate decisions set off a chain reaction that lasted for another five years as both economic growth and inflation decelerated at alarming rates.

These interest rate hikes attracted international capital and this ultimately led to the Canadian dollar soaring from 1.33 to 1.16 (USD/CDN). Exports hit the skids and this contributed to a decline in GDP. The double whammy of 500 bps on the cost of money and a 10% appreciation in the currency led to another recession. By 1991 the economy actually contracted and remained stagnant for at least another year. The only solace was that inflation fell below the 2% mark in 1992 and remained very low for the next few years.

One sector that suffered the most at this time was real estate. House prices in the major cities fell by as much as 25%. The value of commercial real estate collapsed to the point where some of the largest commercial real estate firms entered bankruptcy. The destruction of asset prices worsened the recessionary conditions.

What distinguishes today’s environment from the late 1980s is the absence of inflation. Wage growth remains very muted in both nominal and real terms. Commodity prices, especially for oil and gas, trade within a very narrow range. And asset prices, such as real estate, are coming off their recent highs. All in all, there is no compelling reason to embark upon a policy of continuing raising short term rates. The consequences are too great.

Disclosure: None.