At The Centre Of The Inflation Debate: Slow Wage Growth Explained

At the heart of setting monetary policy is the debate as to why wage growth has been so slow. Central bankers have been struggling with hitting their inflation targets. They constantly point to their disappointment that wages continue to stagnate, despite significant improvements in the unemployment rates. Without a steady upward movement in wages, it is very unlikely that these inflation targets will be met, frustrating bankers who are itching to raise short-term rates. Yet, month after month, labor force data deny the policy makers justification for raising rates.

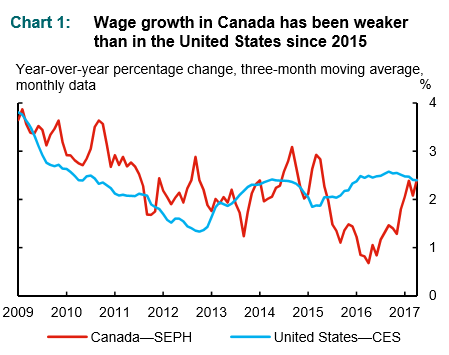

Recent research by the Bank of Canada offers some interesting insights into the factors behind the weakness in wage growth [1].To begin with, wage growth in Canada has been relatively more subdued since 2014 when oil prices collapsed. While it has picked up somewhat since it continues to remain below historical averages. U.S. wage growth has performed relatively better, although it continues to remain weak in spite of an unemployment rate near or at full employment. This has been a continuous headache for the Fed in setting its rate policy.

The major findings of the study are summarized below:

- Slack labor markets. The overriding factor in both countries is the continued presence of slack in the labor market. No surprise there. Both central banks argue that as their respective economies close in on full utilization, wages growth will accelerate. In the case of Canada, the output gap continues to weigh on wage growth more than in the United States. Policymakers anxiously anticipate that once the economy reaches and maintains it potential growth path, inflation of 2 % will be achieved.

- Weak labor productivity growth. Canada’s productivity performance was seriously damaged by the decline in commodity prices. U.S. productivity performance also has been subpar over a similar time period.

- Changes in the labor force composition. As more highly paid mature workers retire, they are replaced with younger, lower paid workers. This depresses the average wage rate throughout the economy.

- Sectoral impact. In Canada, wage growth in the goods-producing sector fell dramatically after the oil shock of 2014, depressing wages throughout. US wage growth was not affected by any specific industry developments.

What can we conclude from this analysis? Aggregate demand must be expanded so that the output gap is closed. The closer we are to operating at full capacity, the more likely wage levels will pick up. We seem to be still well short of potential growth in both countries. With interest rates at relatively low levels, fiscal policy expansion remains the only vehicle for stimulating overall demand. Yet, governments are constrained by existing budget deficits and feel compelled to hold the line on fiscal expansion. Moreover, the demographic forces working against higher wages will continue to operate as a drag on wage performance indefinitely. Thus, it is mostly likely that the world of slow wage growth will be with us for some time to come.

[1] Wage Growth in Canada and the United States: Factors Behind Recent Weakness, Dany Brouillette, James Ketcheon, Olena Kostyshyna, and Jonathan Lachaine, Staff Analytical Note 2017‐8

Disclosure: None.