Big-Dividend Healthcare REITs, Ranking The Best And Worst

If you are an income-investor, you may have noticed that dividend yields just jumped for many healthcare REITs, especially over the last quarter. The reason yields jumped is because many fearful investors rotated out of the industry due to macroeconomic headwinds and regulatory uncertainties. As contrarian investors, this article highlights the best and worst performers, and shares our views on several specific investment opportunities.

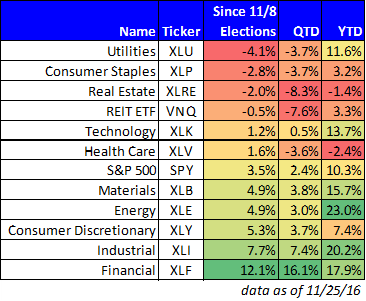

This first chart shows the recent performance across various market sectors, as measured by sector exchange traded funds.

Source: Yahoo FInance

The first thing that stands out about this chart is that the safer, bigger-dividend, sectors have under-performed over the last quarter, and particularly since the November 8th elections in the US. And over the last quarter, two particularly poor performers have been REITS and Health Care as measured by VNQ and XLV, respectively.

REITs have underperformed due to a sector-rotation caused mainly by macroeconomic headwinds. Specifically, as the prospects of stronger economic growth have risen, investors have sold safe, low-volatility, big-dividend REITs in favor of “growthier” sectors such as financials and industrials. Further, the prospects of increasing interest rates puts more pressure on REITs as their yields will become relatively not-as-attractive compared to increasing rates on fixed income securities. Plus, REITs rely on a fair amount of debt to fund their businesses, and rising rates will make it more challenging for REITs to fund growth. And all of these growth concerns were increased following the November 8th US elections whereby the unexpected president-elect appears to be pushing a very pro-growth pro-spending agenda. And on top of that, there was a bit of euphoria leading up to the recent carve-out of a new REIT sector which has since subsided and added downward pressure to the sector. In a nutshell, if you are a contrarian, REITs are worth a closer look (more on specific REITs later).

Regarding the Healthcare sector, uncertainty has weighed heavily. For example, leading up to the recent presidential election (whereby Hillary Clinton was largely expected to win) there was uncertainty about the extent to which the federal government would expand healthcare entitlements, and how that would impact the healthcare sector (i.e. how costly would it be?). And then following the unexpected presidential election results, that uncertainty grew greater consider a soon-to-be Republican controlled House, Senate and Oval Office that seem determined to repeal (or at least modify) the Affordable Care Act.

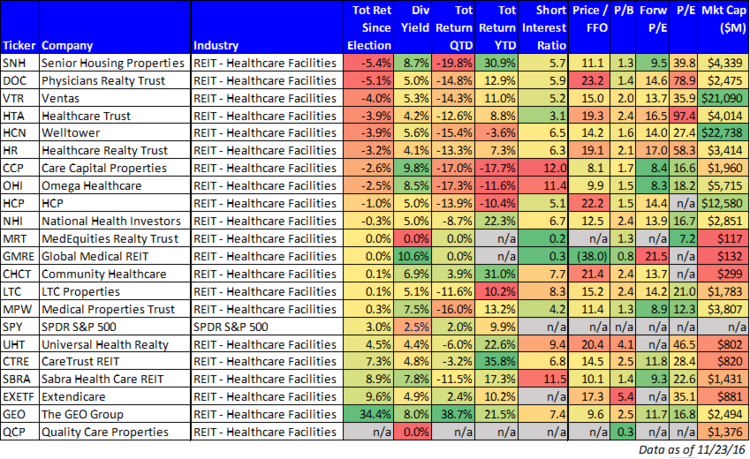

The recent selloff in the REIT and healthcare sectors has been somewhat of a double whammy to healthcare REITs. They have sold off particularly hard, as shown in the following table.

A few general comments about this table:

1) Healthcare REITs in general have significantly underperformed the market (as measured by the S&P 500) since the election.

2) A noticeable exception is The Geo Group (GEO) which is basically a for-profit-prison that has been in the cross-hairs of democratic lawmakers for years, especially recently.

3) If you like ETFs, and you want to make a contrarian play on this underperforming industry, Janus offers a Long-Term Care ETF (OLD) that holds many of the largest healthcare REITs in our table above (e.g. Welltower, Ventas, Omega, Senior Housing, and HCP, to name a few of the largest). However, the volume on this very new ETF (launched this past June) is still very low which can cause dangerously wide bid-ask spreads and trading prices that deviate significantly from its Net Asset Value (NAV). Plus, we’d much prefer to keep the somewhat high 50bps management fee in our own pocket instead of sending it off to Bill Gross et al at Janus. Here are a couple of the healthcare REITs that we consider a more attractive way to take the contrarian-view of this recently underperforming industry..

Omega Healthcare Investors (OHI)

Omega Healthcare Investors (OHI) is an attractive, big-dividend (8.5%), real estate investment trust (REIT). Omega has delivered poor performance so far this year not only because of macroeconomic headwinds that caused REITs to pullback, but also because of heightened Affordable Care Act (ACA) uncertainty (especially following the recent U.S. elections), and because of the market’s overly pessimistic view of skilled nursing facilities (for example, short-interest is significantly high). We believe these three big risks (i.e. macroeconomic headwinds for REITs, ACA uncertainty, and overly pessimistic sentiment) have created an attractive opportunity for diversified long-term investors. You can read our recent writeup on Omega here…

Welltower (HCN)

Welltower is another attractive big-dividend (5.6%) healthcare REIT. We wrote about its attractiveness back in August, but we were hesitant to own it based on valuation concerns. Since that time, the price has fallen more than 15%, and it now trades at a more attractive price. If you are a long-term income focused investor, Welltower is worth considering. For your reference, you can read more about Welltower (including specific risks) in our previous report, here…

Conclusion:

Big-dividend healthcare REITs have taken a beating as fearful investors rotated to other sectors considering macroeconomic headwinds and regulatory uncertainties. If you are a contrarian, value-focused, income-investor, we believe big-dividend healthcare REITs present a significantly more attractive investment opportunity now than they did just a few short weeks and months ago.

Disclosure: None.