The market is once again approaching fairly valued, however, some stocks still trade at compelling levels while others are overvalued and should be sold. Where you invest your funds and, even more importantly, where you do not will be critical to beating the market in 2016.

The S&P 500 is approaching 52-week highs again and the deep losses to begin 2016 are starting to feel like a distant memory. However, with four straight quarters now of declining year-over-year earnings and a global economy that continues to be anemic, my view is there is not much upside in the overall market until we start to see some earnings growth. This will not happen until the second half of the year at the earliest.

That does not mean there are not still good places to invest, but, as the cliché goes, this is a true stock pickers market. I expect the overall market to be flat or slightly down when 2016 comes to a close. Where to invest and, just as critically, where not to put your funds will be critical to beating the market this year and producing a positive return within your portfolio in 2016. Let’s start with what sectors to avoid at the moment.

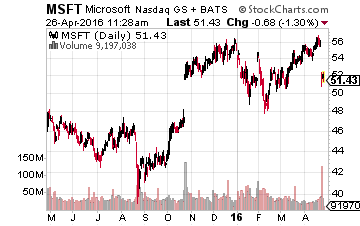

Technology is struggling right now thanks to a strong dollar and tepid overseas demand. Both Alphabet (Nasdaq: GOOGL) and Microsoft (Nasdaq: MSFT) sold off last week after delivering their quarterly results and disappointing investors. In addition, demand for new issues has dried up completely pointing to the negative sentiment on the sector. There has only been one tech IPO so far in 2016. That was Dell cyber security unit SecureWorks (Nasdaq: SCWX) which posted a flat debut even after downsizing its offering last week. I would underweight the sector at the moment.

Consumer Staples (XLP) stocks have drawn a lot of money from the “safety” crowd in 2016 and have easily outperformed the market. However, with an average price to earnings ratio north of 22, little expected growth, and an average dividend yield a little above two percent right now, it is hard to see much in the way of value here at the moment. The same could be said of the Consumer Discretionary sector that has seen some of the same money flows and sports a slightly lower price earnings ratio but a much lower average dividend yield as well. I also have both of these sectors listed as an “Underweight”.

Central banks flooding the market with liquidity is causing banks and insurers to have a tough time growing profits with the yield on the ten-year treasury stubbornly below two percent. This is especially true as regulators and legislators continue to demand their pound of flesh this election year. I have the Financials as an “Underweight” for these reasons as well.

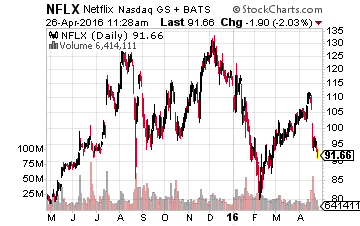

Finally, I would avoid any stocks that have sky-high multiples not supported by fundamentals such as cash flow growth. They are highly vulnerable to any disappointment. One only has to look at what happened to the shares of Netflix (Nasdaq: NFLX) recently when it reported earnings that beat the consensus but did not deliver the robust guidance about international growth investors wanted to hear.

So, what looks good in the current market? Well, the biotech sector has been surging recently and has been one of the strongest performing areas of the market so far in the second quarter of 2016. The sector is up some 20% now from its lows in February. I think we can safely say the longest and deepest bear market for the sector since the financial crisis is officially over.

Helping the sector is M&A chatter picking up again. The rally in crude oil, which has helped stabilize the high-yield credit markets, is a tailwind to any small or mid-cap biotech concern that may need to access additional funding for developmental needs at some point in the foreseeable future. Large biotech stocks have benefited from investors coming to the realization this space is one of the few in the market that can deliver both earnings and revenue growth as the overall market is locked in a profit recession.

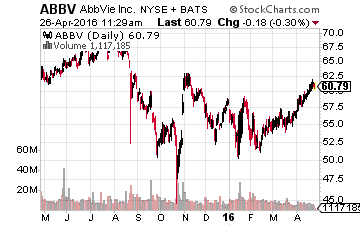

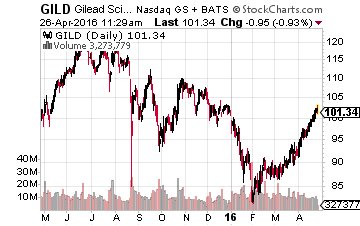

This week we get quarterly reports from industry stalwarts like AbbVie (Nasdaq: ABBV), Amgen (Nasdaq: AMGN), Celgene (Nasdaq: CELG), and Gilead Sciences (Nasdaq: GILD). Both Amgen and Gilead have beaten the consensus for eight straight quarters. If results are strong once again, this may power the next leg of the recent rally as the sector is still more than 25% below its peak levels last July. I own all the names listed above and they are still good values in what feels like a slightly overbought market at the moment.

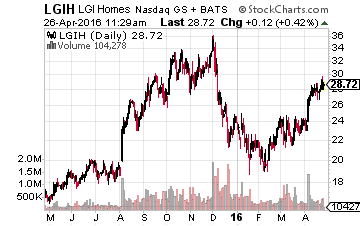

Although the housing market continues to recover in a two steps forward one step back fashion, there is value in the home builders. Mortgage rates remain near historical lows, job creation continues to be solid, and household formation is back above pre-recession levels. All this bodes well for a continued acceleration of housing activity. 2015 was the best year for housing starts since 2007 but even that year was more than 20% below the 30-year average. In many markets, the biggest obstacle for home sales is a lack of inventory.

I continue to like all the home builders I have profiled on these pages this year including LGI Homes (Nasdaq: LGIH), Taylor Morrison (Nasdaq: TMHC) and TRI Pointe Homes (NYSE: TPH). For those wanting broader exposure to the sector, the SPDR Homebuilders ETF (NYSE: XHB) can easily be tucked into one’s portfolio.

That is my take on the current market.

Comments

Log in or sign up to join the conversation.