The Warren Buffett Economy—Why Its Days Are Numbered, Part 2

<< Read The Warren Buffett Economy—-Why Its Days Are Numbered, Part 1

There is no reason whatsoever to believe that the financial carrying capacity of the US economy—or any other DM economy—has improved since the 1980s. In fact, it has gone the other direction in recent years due to aging demographics, declining competitiveness versus the surging EM economies, dwindling rates of productivity growth and a dramatic increase in the leverage ratio against both public and private incomes.

All of these adverse macro-trends mean that the US economy’s ability to generate growth, incomes and profits has been significantly lessened. Accordingly, since its ability to service debt and equity capital at an honest market rate of return has diminished, the logical expectation would be that the finance ratio to national income would fall.

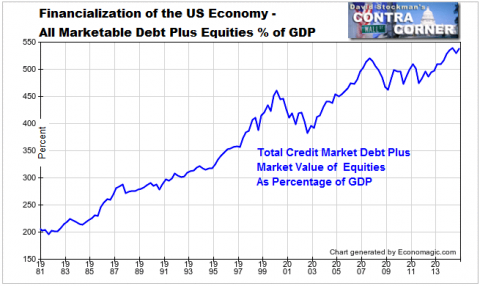

In fact, once Greenspan took the helm and his apparently atavistic embrace of gold standard money melted-down under the Wall Street furies of October 1987, the finance ratio erupted. As shown below, it has never looked back and at 5.5X national income has reached a point that would have been unimaginable on the morning of Black Monday.

Stated differently, under a regime of honest money and market determined financial prices, the combined value of corporate equities and credit market debt would not have mushroomed by 8X—- from $11 trillion to $93 trillion—- during the past 27 years. For crying out loud, the nominal GDP grew by only 3.5X during the identical span. In effect, the US economy has been capitalized at higher and higher rates for no ascertainable reason of fundamental economics.

Indeed, there is no reason why the 260% ratio of equity and credit market debt to GDP that was recorded in 1986 should have risen at all. At that point Paul Volcker had completed his historic task of extinguishing runaway commodity and CPI inflation and had superintended a solid recovery of real economic growth.

Arguably, therefore, the US economy was carrying about the right amount of finance. And, at that healthy ratio, today’s $17.7 trillion economy would be carrying about $43 trillion of combined market equity and credit market debt.

In a word, the Greenspan era of central bank driven price falsification and monetization of trillions of existing assets with credits conjured from thin air has generated a $50 trillion overhang of excess financialization. And that’s just for the US economy. In fact, the central bank error is global and the worldwide excess financialization is orders of magnitude larger.

Total Marketable Securities % of GDP – Click to enlarge

To be sure, the Keynesian economists and power-seeking apparatchik who run the Fed do not openly admit to a massive falsification of financial prices and to responsibility for generating what amounts to a $50 trillion bubble in the US alone.

That’s because they are narrowly and mechanically focused on an altogether different, but impossible task. Namely, guiding the $18 trillion US economy to its full-employment potential. So doing, it pursues its so-called Humphrey-Hawkins “dual mandate” in a manner consistent with the strictures of its Keynesian DSGE (dynamic stochastic general equilibrium) model representation of the US economy.

Moreover, this particular iteration of god’s work is viewed by the monetary central planners and their academic and journalistic proponents as not being merely discretionary. That is, its not just an exercise in making the good, better.

Instead, by relentless and plenary interventions in the financial markets designed to smooth and optimize the business cycle, the Greenspan era central planners came to believe that they were actually saving capitalism from its own purported death wish. That is, an endogenous tendency toward instability, underperformance and depressionary collapse.

This whole story is a crock. Cutting to the chase, the Humphrey-Hawkins Act is one of the stupidest and most dangerous laws ever enacted.

It amounts to a plenary delegation of power to a tiny unelected and unaccountable posse of monetary bureaucrats who are free to define the key goals—maximum employment and stable prices—anyway they wish; and are then further empowered to manipulate—without standards or limits—any and all financial prices in whatever arbitrary manner they choose in hot pursuit of the arbitrary quantitative metrics, whether efficacious or not, that they have slotted into the Act’s rubbery, content-free aspirations for societal betterment.

In plain English, 5.2% unemployment on the U-3 measure and 2% inflation on the core PCE deflator are economically meaningless targets. They are impossible to achieve through interest rate manipulation and the rest of the fed’s tool-kit, especially its wealth effects “put” under the stock market.

Likewise, the so-called Humphrey-Hawkins targets have no discernible relationship to societal betterment—since there is not a shred of evidence, for example, that wage workers are better off with 2% inflation as opposed to 1% or any other arbitrarily chosen value of a flawed price index over completely arbitrary, and usually unspecified, time frames and prices cycles. And, most crucially, forcing the macro-economy into adherence to these policy targets is utterly unnecessary because the predicate that capitalism has a death wish and is prone to depressionary collapse is dead wrong.

In truth, it’s a self-serving scary story peddled by the monetary central planners and their grateful Wall Street beneficiaries. I have addressed the myth of the foundation events—the Great Depression of the 1930s—elsewhere. Suffice it to say that the modern Keynesian narrative has it precisely upside down.

The Great Depression did not stem from a fatal flaw of capitalism or the failure of the 1930-1933 Fed to crank up the printing presses or even Hoover’s allegedly benighted dedication to fiscal rectitude and honest gold standard money. Just the opposite. The Great Depression was owning to the excesses of state action—the massive indebtedness and inflation of the Great War and the easy money credit bubbles of the Roaring Twenties—not to its supposed deficiencies.

Likewise, the post-war business cycles prior to Greenspan’s accession were short-lived, well-contained and self-correcting; they were owing to the errors of state actions, not the inherent flaws of capitalism or an alleged business cycle instability that threatened an unstoppable downward spiral.

Specifically, two of these recessions were the temporary consequence of cooling-down red hot war economies in 1953-1954 (Korea) and 1969-1970 (Vietnam). The first one of these was self-cured by the inherent resilience of market capitalism and involved virtually no fiscal or monetary stimulus under the orthodox strictures of President Eisenhower and William McChesney Martin at the Fed.

Likewise, the post-Vietnam so-called recession hardly registered in the economic statistics—save for a 70-day auto strike. That wasn’t even a business cycle, but a random shock from the complete shutdown of GM and its massive supplier base in the fall of 1970 at a time when GM was at its peak and occupied 45% of the entire US auto market.

Needless to say, that strike was eventually resolved by the parties involved, triggering a sold rebound immediately thereafter. There was no business cycle failure or threatened tumble into an economic black hole—nor did the fiscal and monetary authorities of the day do much to “stimulate” the natural forces of recovery.

By contrast, the two deepest recessions of the pre-Greenspan period—the 1974-1975 downturn and the 1981-1982 recession—were caused by a very evident villain. In those cases, you can pin the tail squarely on the donkey at the Federal Reserve itself.

As I demonstrated in the Great Deformation, the mid-1970s cycle was not caused by the 1973 post-embargo oil price surge; it was the result of Fed Chairman’s Arthur Burns abject submission to Nixon’s demand for a 1972 pre-election surge of the US economy.

As to the deep plunge of the early Reagan era, the Mighty Volcker was at the helm, of course, only because Arthur Burns and his successor, the hapless golf cart manufacturer, William Miller, had fueled a massive domestic credit expansion during the second half of the 1970s. The double-digit inflation that Volcker brought to heal was manufactured by the central bank, not by the OPEC cartel, silver and copper speculators or greedy consumers, as Jimmy Carter had it at the time.

As of Volcker’s turn at bat, there was at least a possibility that state policy might escape from the thrall of Keynesian economics. It had been installed on the fiscal side during the Kennedy-Johnson era, and embraced by Nixon himself when his itinerant policy groupie, George Schulz, professor of labor economics, persuaded him to adopt the full-employment budget concept.

That was pure Keynesian claptrap. It was predicated on the idea of a closed domestic economy that resembled a giant economic bathtub—which needed to be filled to the brim with GDP for maximum societal welfare; and that the job of the state through the coordinated action of its fiscal and central banking branches was to pump aggregate demand into the tub until the economic experts averred that potential GDP and full employment had been achieved.

Mercifully, the primitive experiments with this during Johnson’s “guns and butter” policies after 1965, and the Nixon-Burns money printing spree of 1972-1974 resulted in the 1970s catastrophe of stagflation. Accordingly, bathtub-based Keynesianism was at death's door when Ronald Reagan arrived at the White House in 1981.

And the giant Reagan deficits notwithstanding, it was further buried by the roaring success of Volcker’s hard money policy and the Reagan administration's resolute refusal to consider anything that smacked of proactive fiscal or monetary stimulus during the dark days of 1982.

The giant Reagan deficits were owing to an explosion of defense spending and a tax-cut bidding war that got totally out of hand in the summer of 1981, not any notion at all that capitalism needed the helping hand of the state in order to get back on its feet after a state sponsored credit inflation had set it on its heels.

Then came the 1984 election campaign about morning in America, which was mainly harmless political bloviating. But the White House politicians could not leave well enough alone. Soon followed the disaster of the Plaza agreement of 1985 designed to trash the dollar and artificially stimulate domestic economic activity, and then trasnpired the real calamity.

To wit, Ronald Reagan was tricked by Jim Baker and the Republican elders on Capitol Hill into forcing Volcker out of his job as chairman of the Fed. In Part 3 it will be shown that the double-talking, power-seeking, lapsed gold bug named to replace him brought Keynesian bathtub economics right back into the center of policy.

Yet in the world after Mr. Deng’s pronouncement that it is glorious to be rich, the idea of a full bathtub policy in a single country is absurd. It embodies the spurious notion that the primitive measures of labor and business capacity utilization published by the rickety statistical mills of government measure anything that is accurate or economically meaningful.

In fact, the U-3 unemployment rate and the Fed’s industrial capacity utilization figures amount to nothing but noise. The utilization rate of the auto industry, for example, might have been remotely relevant before 1980. Today it measures the same cycle over and over, but means nothing, as will be demonstrated in Part 3.

![]()

>>Continue to The Warren Buffett Economy—Why Its Days Are Numbered, Part 3

>> Continue to The Warren Buffett Economy—Why Its Days Are Numbered, Part 4

>> Continue to The Warren Buffett Economy—Why Its Days Are Numbered, Part 5

Disclosure: None.