The Fed Likely Won’t Raise Rates In 2017

As I mentioned in my last article, the reflation trade has stalled and is now starting to reverse. The country was relieved the election was over so survey results were off the charts in terms of optimism. I showed you how some surveys showed firms not claiming they saw any boost in sales, but they began expecting sales in the future to be excellent anyway. It’s baseless optimism in my opinion. We’ll see if the optimism wanes in the next few weeks as it has shown signs of doing with the reflation trade pulling back in the past 4 weeks. The basis for buying stocks because a Trump presidency will grow the economy is a logical fallacy because George W. Bush cut taxes and we still had a recession because of the tech bubble. Reagan cut taxes and promised deregulation and there was a deep recession in 1982 where the unemployment rate went above 10%. It’s not that tax cuts and deregulation are bad. It’s that the only thing that can cause a debt bubble to heal is a painful deleveraging.

I’ve seen chatter the Fed may decrease its balance sheet. I view this as an impossibility. Tax cuts and spending increases on infrastructure would need to be funded by the Fed because interest rates would rise, ballooning the deficit. On the other hand, if the economy weakens, the Fed will have to do QE to try to keep the economy afloat. The goldilocks scenario is if the government is able to cut taxes and cut regulations enough to boost growth. Trump would try to cut some spending and the growing economy would raise more tax revenue. In this case, the Fed wouldn’t have to backstop the deficits. In this scenario, inflation would remain stable so the Fed could unwind the balance sheet gingerly and raise rates a few times this year.

The reason why I say this goldilocks scenario is impossible is because the pro-growth measures don’t prevent recessions as I exemplified with the recessions in the early Reagan and Bush years. Secondly, the economy has been in recovery mode for 8 years and the Fed hasn’t begun unwinding the balance sheet. Maybe the Fed would sell some bonds if the GDP grew consistently at a 4% rate in 2017, but we have no evidence that this would be the action. I also don’t see a 4% growth year happening.

The one point I don’t have an update on is who Trump will pick to be his Fed chairperson or who he will pick to fill the two vacancies on the FOMC. Judging by some of his other picks, it seems like he will pick someone who is critical of the Fed’s role. He picked Rick Perry to be the Energy Secretary. Rick Perry had previously campaigned on ending this agency. Trump was deciding between John Allison and Steven Mnuchin among others for his Treasury Secretary. If you were to analogize that to the Fed, Trump would be picking between someone like Ron Paul and someone like Mitt Romney. You may say someone who wants to end the Fed like Ron Paul is an extreme choice, but John Allison espouses that viewpoint. Mitt Romney campaigned against QE 2. He’d want to bring the balance sheet down and have a Fed policy more like Paul Volcker than Bernanke/Yellen. This is my viewpoint of Trump’s Fed appointment if I use his previous appointments as a benchmark.

However, I have previously discussed the likelihood Trump will rely on the Fed to boost the economy just like Obama has for the past 8 years. It won’t be easy to have the economy stand on its own without extraordinary monetary policy holding it up. If the economy falters in the second half of the year, there will be temptation to re-appoint Yellen or appoint someone with a similar worldview. This would mean lower rates and more QE. One way which would foil this possibility is if early on in his administration Trump fills the vacancies with hawks. At that point, he’d have no choice but to stay the course with his Fed chair pick. He needs to appoint people who have the same worldview because if he doesn’t, the Fed would be disjointed. Yes, votes on rate changes don’t have to be unanimous, but it would hurt the Fed’s forward guidance ability because there would be several views being espoused simultaneously.

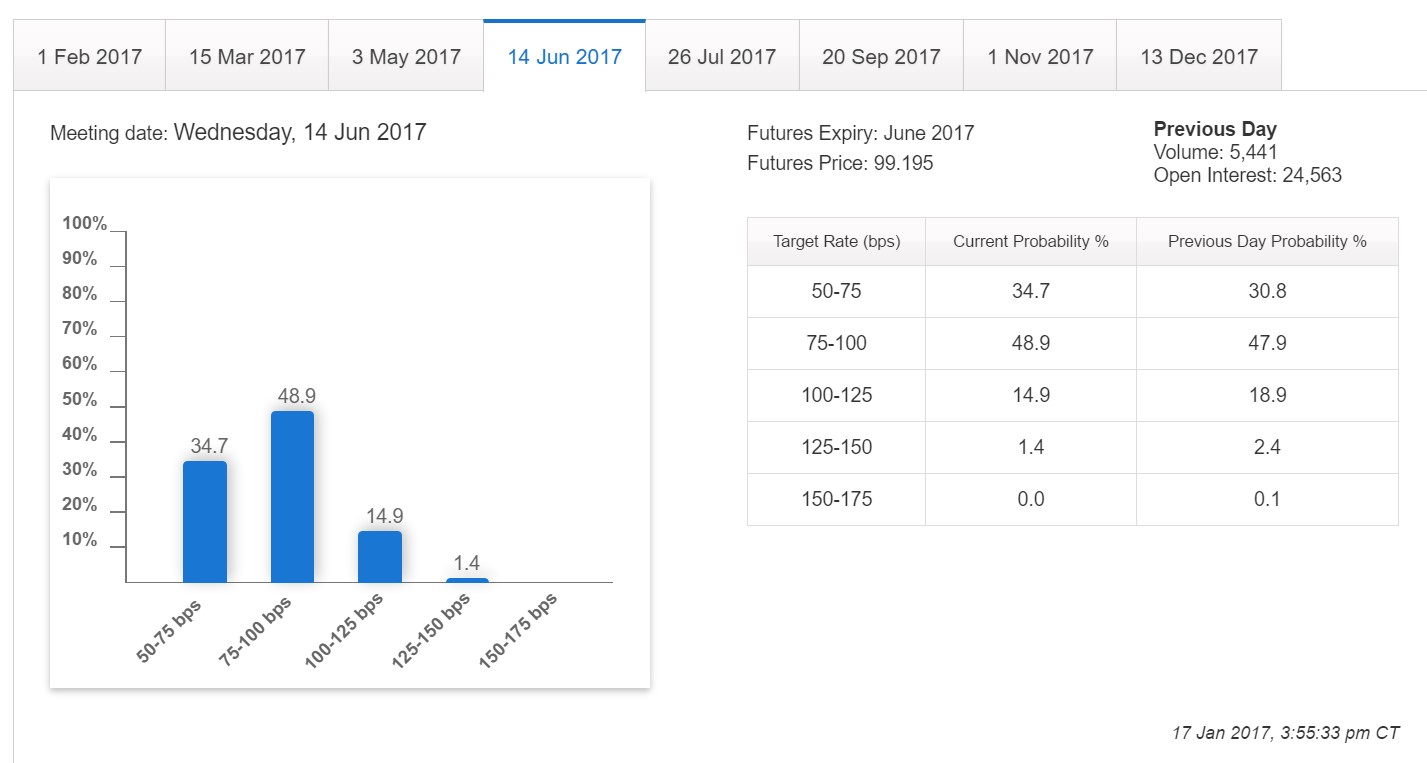

The chances of Fed hikes follow the market. When the Trump trade was in full force in mid-December, there was a consensus towards rates increasing at a faster clip than there is now that some of the moves have pulled back. The Fed follows these odds, so they’re worth paying close attention to. It’s not that the Fed has no power because Fed officials’ comments affect these odds as well. As of January 17th, the market is waiting until the June meeting to predict the Fed will raise rates for the first time this year. There is a 65.2% chance for a rate hike by June which would only be a rate of 2 hikes for the year which is already below the 3 hikes forecasted. Usually the Fed doesn’t raise rates unless there’s an 80% chance of a hike priced into the market. If you use that template, the Fed will wait until November to raise rates. That would be one rate hike for the year.

(Click on image to enlarge)

The Fed is in a ‘wait and see mode’ when it comes to policy. It got the one rate hike in before Trump takes office, but now it has to wait until we get some clarity on the fiscal policy front. It will look at how the market is reacting and decide what to do. The market can change quickly as the policy news is broken so the Fed will be cautious in the next two meetings. By the time the Fed starts reacting to the market, the year will be half over. Trump’s growth policies would have to be amazing to have the Fed reach its three rate hike forecast with that slow start. I’m maintaining my prediction for no rate hikes this year.

Disclaimer: Neither TheoTrade or any of its officers, directors, employees, other personnel, representatives, agents or independent contractors is, in such capacities, a licensed financial adviser, ...

more