Market Briefing For Monday, April 9

Repercussions - Fed Chairman Powell's realistic and balanced assessment on credit and rate plans, along with Treasury Secretary Mnuchin's very diplomatic way of handling gotcha-type questions in an extended interview; only briefly swayed the market to rebound; before succumbing and moving to newer lows for the session. Do know that the market did NOT hold the 200-Day Moving Average either; especially when viewed in an all-stocks basis as opposed to a capitalization-weighted basis (lead by a handful of stocks).

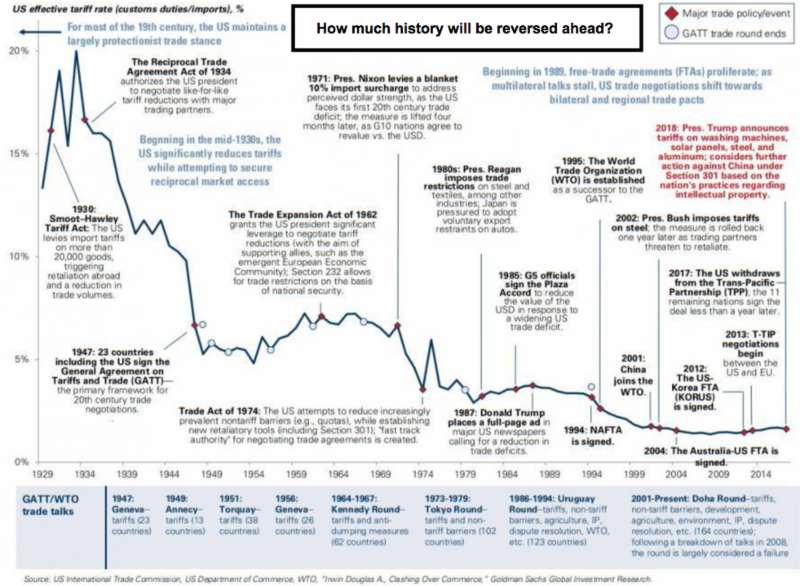

Our overall forecast anticipated not just the Friday pattern; but realized a couple days ago; that President Trump would have to double-down so as to get China's attention, after both Kudlow and Trump inferred it was just a bluff. That the market received that well (Wednesday's turnaround), for sure was why I anticipated Trump would have to feel emboldened (with the Chinese immediately declaring 'victory' Thursday morning). Hence it became essential the United States move to reassert its determination.

So sure, trade and tariff issues move the market; and we've identified the likely rebound failures. Plus the moves (in our view) are a larger strategy to extract better deals from China (and that goes for other countries too), without getting into trade wars. Mnuchin did the best job of balancing this while acknowledging we're 'not' in a trade war, but the 'potential' exists of course. Although I remind we already heard from members that a series of steel and component price increases are already filtering through; it's too soon to reach the inflation (or perhaps stagflation) conclusion, which leaves markets with ongoing outlined uncertainty and diving financials.

Now we have a market breakdown (techs and even financials should do well on the downside in the beginning of the new week); right in front of 'earnings season' starting. I have already forewarned that 'earnings' are not the key here (maybe minor responses); especially if managements of major multinational companies reflect the truth: uncertain guidance for at least the next Quarter.

Now the very big stocks getting killed (or about to), for sure can become interesting at lower levels, 'if' we make a satisfactory deal with China. At the moment that's apparently way-off in the future. The President himself has warned of what I've said for weeks with regards to 'trade': short-term (perhaps intermediate) pain for longer-term gain. That's gain for the U.S.; not just the major multinationals that already got a nice tax break.

So: many 'repercussions' that continue to 'Bear' the market, per forecast for 2018; ultimately can become a cloud with a silver lining for business; those that focus on enriching American workers first and foremost. That is also the best way to enhance consumption too; and will be good for a slew of nations; if they play ball, and this is handled without 'lost face' on both sides of the Pacific, not to mention derailing China's effort to woo the EU to take-on the U.S. We don't have many allies in this struggle but there are reasons for them to calm down; work on this together; as at the same time stocks proceed to lower levels where they're attractive.