Market Briefing For Monday, Oct. 16

Crippling concerns proliferate but have not crushed this market's rather tenacious ability to maintain its reliance in the face of uncertainty. One real irony is that despite the geopolitical concerns and even peaking 'confidence' among consumers and investors, you don't see equivalent economic gains.

The sanctions that exist could be said almost lesser toward Iran, and more toward those resisting the global market advance, unjustified by real growth, but buttressed by 'fear' of central banks (in the US and abroad) to normalize rates as they put it. Sure it's because of reasons other than growth; and we have argued why they've also perpetuated the long-run low rate policies.

On Friday, outgoing Vice Chairman of the Federal Reserve, Stan Fischer (a mentor to central banks and bankers globally for years) actually affirmed my view of these policies. He glibly noted (in a CNBC interview) that 'low rates in pace do allow keeping a bit higher Debt than otherwise could be done'.

I'm presuming that means than 'could be done' without really pointing out a real problem being 'debt service' costs if you have both high debt and high interest rates. To me that's been an inhibitor of snugging-up policy for years and it's got them in a corner, given the impossible debt service levels 'were' rates to go meaningfully higher. That's why they are so 'moderate' in there oft-proclaimed desire for growth or inflation to justify raising rates.

There is a also-debated topic of growth not triggering inflation; but it requires going back to another era (like the 1950's and in some ways this is similar), for hopes to see that persist. It would also require energy prices staying low. And there you have today's (also bandied-about) story that Saudi Arabia is considering 'shelving' the Aramco IPO coming next year. That's denied but it is an interesting consideration.

Clearly I have contended the Saudis need a higher Oil price for the IPO to be well-received; and the Russians need high Oil price to simply function; hence the unlikely frenemy deal last week. It was (in my view) ludicrous for OPEC to then expect the USA to go along with their proposed pleas for US producers to lower exploration and production of Shale Oil; so prices will stay high. As I said last week; after what OPEC did to us, not for us, why in the world would recovered US Oil producers cooperate with that. Hell no, as anyone who lived thru the Saudi-driven destruction of the oil and real estate markets in Texas, Louisiana, along with most independent oil producers all over the United States, would concur with. They are not really our friends.

Technically the market persists churning at a high overbought level by any reasonable assessment. This has frustrated bull and bear alike; because at this stage the bulls are rationalizing buying big caps and actually moving to a degree into smaller stocks. That's not insane because better values exist, but at the same time it reflects a hesitancy to chase overpriced stocks.

In essence that's the genus of why I call this an 'exhaustion phase' and also this era's variation on the Greater Fool Theory. Back in 1998-99; the theory was something I talked about as going a bit higher, but too risky to chase. It was, as it didn't mean you couldn't move higher; just that somebody would be caught holding the bag at the end of the line (reminds me of the long ago tune an old contemporary named Joe Granville liked to sing at seminars, as he played piano: he entitled it 'The Bagholder Blues').

Of course, I am reminded of my 1998 view because it was late 1999 in the bubble (mostly in tech) that I warned of a market crash coming, ideally in the Spring of 2000, perhaps April. Well, indeed it was April. Here that could mean highs in 2018 or even 2019 instead of well right now but there are many variables not the least of which will be tax-reform and/or geopolitics. However there is little argument that we're due for a correction (at minimum), especially with a slew of recently skeptical bulls-turned-bears, now back to being 'optimistic'.

|

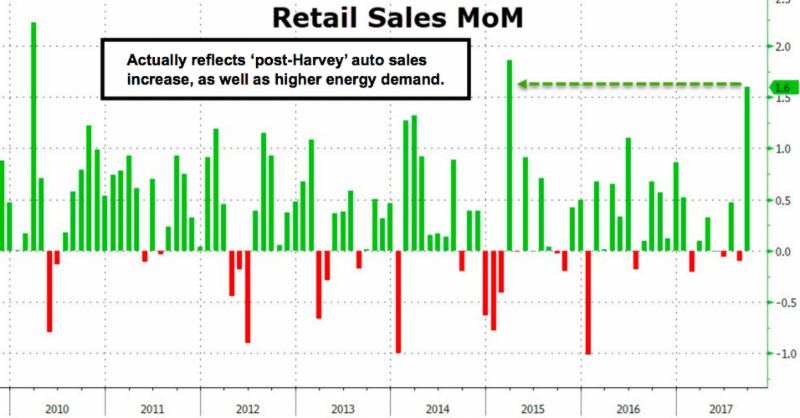

Insum The 'Goldilocks on Steroids' monetary policies are being strained. A large amount of emerging markets have issued securities in Dollar terms, so are nervous about snugging-up policies. Cleaner inflation numbers (versus distortions during the hurricane-related impacts on energy and retail just as a for instance) and realities about handicapping tax and other policies are not productive. We'll probably get higher inflation in terms of healthcare and other sectors over time and that's part of 'stagflation' especially with income levels remaining rather flat for the average American household. |

|

Weekend (final) MarketCast |

Disclosure: None.