Broken Employment

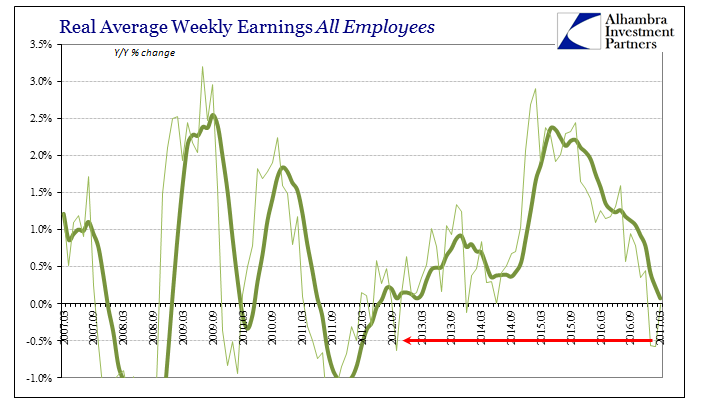

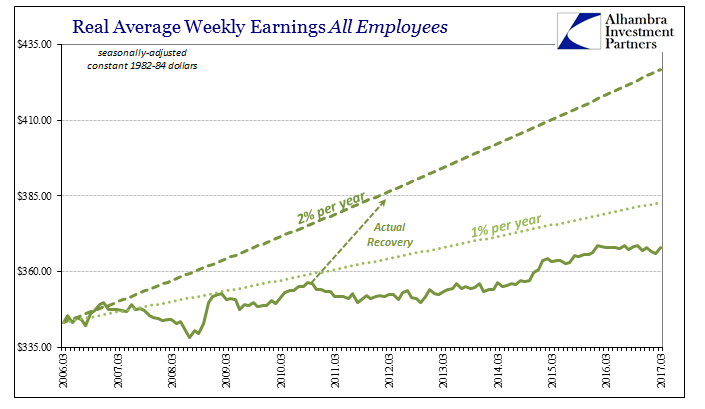

For the third consecutive month real average weekly earnings fell year-over-year. In March, at least, with the CPI starting its downward leg the decline was by the smallest amount; essentially flat but fractionally less than zero. It was the first time real wages have fallen three in a row since early 2012. The six-month average is just about zero, too, unsurprisingly also the lowest since mid-2012.

Despite the unemployment rate falling well-below 5%, there isn’t the first sign of wage acceleration in nominal terms. That has left real wages to the whims of oil prices, first as their biggest boost in years as oil prices, like early 2009, collapsed and now on the wrong end of them as they partially rebound. The overall negative effects aren’t so much the decline in real terms as the unstable and highly volatile nature of it all that never really gets better.

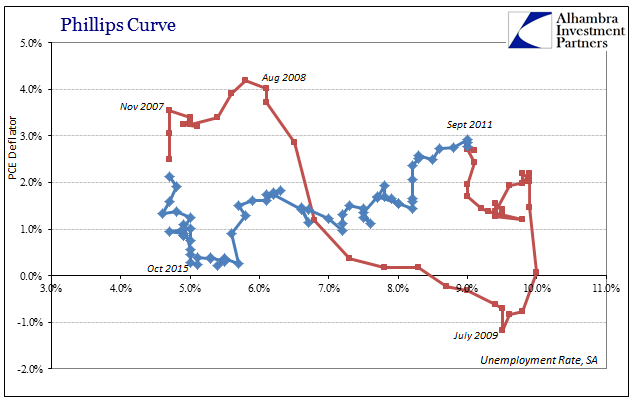

In early 2014, right at the start of her tenure, Janet Yellen claimed that nominal wage growth of 3% to 4% “would be normal.” The official and academic literature of the time also concluded that a 5% unemployment rate reflected full employment. Earlier this month, Yellen confirmed as much for the first time at the University of Michigan’s Ford School (fiasco), saying:

With an unemployment rate that stands at 4.5 percent, that’s even a little bit below what most of my colleagues and I would take as a marker of where full employment is.

She then added for good measure, “I’d say we’re doing pretty well.” So where are the wages? If the unemployment rate is an accurate depiction and it is significantly (not a bit) less than the full employment mark, nominal wages should be accelerating quickly and more so all the time. The base effects of oil prices should not be a matter for any consideration but a small footnote on economic completion.

Yellen may refuse to admit it, but “something” is not only missing but has to be missing. From her comments she is either being disingenuous or she has bought into R*, either option leads nowhere good. If it’s the latter, and I’m sure it is, then the once-perpetually optimistic Federal Reserve has joined the club of doom and gloom. The only difference is that the current thinking on R* places the gloom at someone else’s doorstep (yours).

At any other point in history, the labor market rendezvous with full employment was met with significant and welcome economic improvement. In common sense terms, how could it be any other way? If the labor market is truly robust, jobs overly plentiful, then labor demand as well as the fruits of that exchange can only be the righteous combination everyone understands as recovery.

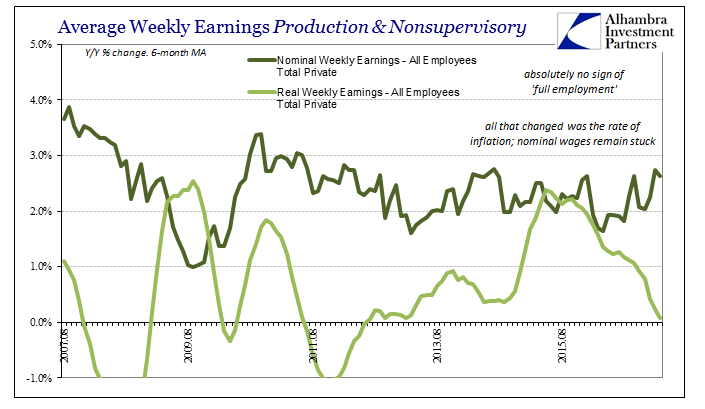

With an unemployment rate at 4.5%, nominal wages at 2.5%, and real wages down near and below zero, it cannot be recovery or even growth. Furthermore, there isn’t the slightest hint that any of that is about to change (including the unemployment rate). It’s not as if the unemployment rate was 6% just a few months ago and the labor market just now is adjusting to a welcome burst of activity, it has been at or very close to “full employment” for two years already.

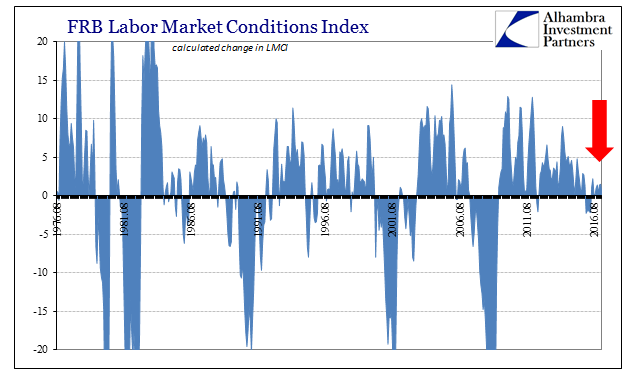

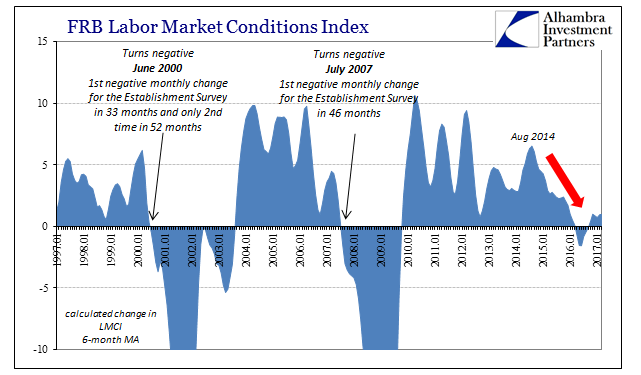

Yet, the BLS payroll numbers defy it and continue to suggest slowing or at best sluggishness, while other data confirms that condition. The Fed’s Labor Market Conditions Index (LMCI) for example, turned negative at the start of 2016, a result that in the past was consistent with recessionary effects bleeding into the labor market. It turned positive again five months later, in June 2016, but rather than shoot upward as every other time in the past the index remains unusually and conspicuously subdued.

It has been stuck at (a monthly change) less than 2 for the past eight months, and increased by just 0.4 in March 2017, the latest estimate. Like the rest of the economy, the most that can be said of this view of the jobs market is that it isn’t getting worse; but it isn’t getting any better, either. This is surely a conundrum given the unemployment rate’s already extended stay at and now below “full employment.” One of those things is certainly wrong.

Breakdowns of this kind, however, are nothing new for the 2010’s. The world economy is a very different place, a fact that R* is statistically trying, at long last, to recognize and make sense of. In truth, the growing consensus about this low or even negative “natural” rate of interest is really that economists just now figured out something is very wrong, as if the contradiction of wages and the unemployment rate weren’t enough years ago. They claim they keep seeing signs of wage growth, but after three plus years of only signs of it common sense knows better.

The US needs wage growth. There is none to be had. “Reflation” or not, this is an impasse that is far beyond “full employment.” It speaks instead the idea of broken employment.

Disclosure: This material has been distributed fo or informational purposes only. It is the opinion of the author and should not be considered as investment advice or a recommendation of any ...

more