Cash Makes A Comeback

Our outlook for real interest rates is 30-40 bp higher across fixed income sectors relative to the end of 2017. But the key change to the fixed-income markets is not the level of rates, but the fact that the yield curve is now essentially flat. Of note, our outlook for longer-dated bonds is little changed from the middle of 2017.

This argues for more ultra-short bonds and money market instruments in client portfolios. Each of our model portfolios has more cash equivalents than a month ago (by cash equivalents we mean interest paying obligations that mature in less than 1 year), with the sharpest increases occurring in our moderate risk tolerance portfolios (the most conservative portfolios had a lot of cash to begin with and the most aggressive portfolios have much smaller total fixed income exposure).

Amazingly, our long-term outlook for global equity market returns is practically unchanged from the start of the year. Strong price gains in January were followed by a sharp correction in early February that gave way to a modest rebound in recent days. The net result of all that price movement is stock valuations that are at a level consistent with continued improvement in the outlook for corporate earnings.

Long-Term Equity Market Return Outlook:

Projected Long-Run Annual Real Returns

Source: arcpointadvisor.com

Despite a brief correction to global equity prices earlier this month and a return to more normal levels of volatility, our outlook for future equity returns is little changed from the beginning of the year. In effect, the modest net gains across equity markets YTD (through February 21st) have kept pace with continuing improvements in the outlook for corporate earnings and the benefits of a slightly weaker U.S. dollar.

Our forecast for U.S. large-cap equity returns implies average annual mid-cycle earnings of $128 for the S&P 500 index companies, up $2 from our prior estimate. This earnings outlook compares to the consensus bottoms-up forecast of $158 over the next four quarters for S&P 500 earnings.

The fact that consensus earnings are now 23% above our mid-cycle forecast typically would be a negative signal. However, much of the recent upward revisions are attributable to the new U.S. tax law. In aggregate, it does not appear that investors are (completely) taking the bait and assuming that every tax dollar saved will end up in the pockets of shareholders. In short, we believe that investors are displaying greater wisdom than the brokerage firms publishing earnings forecasts.

We still continue to favor non-cyclical equity in our model portfolios as there is no return benefit for U.S. cyclical equity and only a modest one for foreign-developed cyclical equity. And much of the remaining premium for foreign-developed cyclical equity is attributable to that sector’s heavier exposure to financials (which adds to the sector’s risk profile).

The roughly 100 bp premium offered by foreign-developed cyclical equity over U.S. cyclical equity is above the average of 85 bp over the past five years. Our model portfolios continue to modestly favor foreign developed over U.S. cyclical equity.

The premium return offered by emerging market equity has shrunk in recent months but remains at a level that recommends emerging markets inclusion in each of our model portfolios.

Difference Between Projected Cyclical and Non-cyclical Equity Returns

Source: arcpointadvisor.com

Cyclical Large-Cap Equity Premia

Source: arcpointadvisor.com

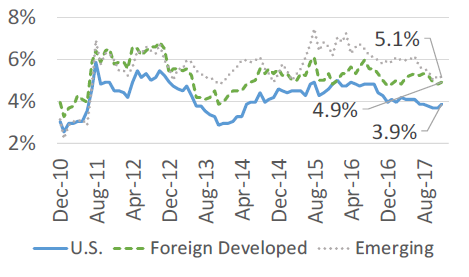

Long-Term Fixed Income Market Return Outlook:

Projected Long-Run Annual Real Returns

Source: arcpointadvisor.com

Projected real fixed-income returns are higher across maturities due to an increase in real interest rates, with greater increases at the front end of the maturity curve.

The estimated real term premium offered for 10-year U.S. Treasury (UST) bonds is down 9 bp m/m. A 10-year UST note purchased in five years offers 9 bp of additional return over a 52-week UST bill. This level is well below the 10-year average real term premium of 57 bp and reflects the flattening real yield curve.

Risk-Free Real Term Premium

Source: arcpointadvisor.com

The estimated inflation risk premium is effectively zero for a 15-year bond. The inflation premium remains below 20 bp for the 28th consecutive month. We use break-even rates in the U.S. Treasury market to estimate inflation premia. Given the conundrum of no apparent inflation premia despite higher inflation expectations, we also are closing watching the CPI inflation swap market. There too, implied inflation premia are quite low (10bp for a 15-year bond five years forward).

Inflation Term Premium (15-Yr. Bond)

Source: arcpointadvisor.com

We estimate that investors in investment-grade corporate bonds are receiving 6 bp of return for every year to maturity as compensation for credit risk, similar to a month ago. The current credit risk premium is consistent with the 5-year average of 5 bp for every year to maturity.

Credit Risk Premium Per Year

Source: arcpointadvisor.com

Disclosure: None.

I think rather than short term rates going down, long term rates will rise to widen the spread even if the Federal reserve doesn't want them to. The recent rise in treasury yields came on buyers balking at existing rates, not the Federal Reserve raising them.

Interesting perspective Moon. @[Joe Arns](user:61421), what's your take?

Longer term real interest rates are dictated by global economic output and the marginal propensity of individuals to save vs. consume, and I agree that the Federal Reserve's ability to impact these rates is limited at best. However, I don't see a much steeper yield curve unless inflation concerns are such that a premium is demanded for holding longer term paper. And right now, the market is saying that although expected levels of inflation are a bit higher than a few months ago, there is little concern that inflation will accelerate to much higher levels.

Impressive work.